ACID – an acronym referring to Atomicity, Consistency, Isolation and Durabilityas applied to database transactions. ACID transactions guarantee that each read, write, or modification of a database table has the following properties:

Atomicity – each read, write, update or delete statement in a transaction is treated as a single unit and either the entire statement is executed, or none of it is. This prevents data loss and corruption from occurring if a transaction fails midway,

Consistency – transactions only make changes to tables in predefined, predictable ways so that data corruption or errors don’t create unintended consequences for the integrity of your table.

Isolation – when multiple users are reading and writing from the same table all at once, isolation of their transactions ensures that the concurrent transactions don’t interfere with or affect one another. Each request can occur as though they were occurring one by one, even though they’re actually occurring simultaneously.

Durability – ensures that changes to your data made by successfully executed transactions will be saved, even in the event of system failure.

In summary, an ACID-compliant database transaction is any operation that is treated as a single unit of work, which either completes fully or does not complete at all, and leaves the storage system in a consistent state. ACID properties ensure that a set of database operations (grouped together in a transaction) leave the database in a valid state even in the event of unexpected errors. A common example of a single transaction is the withdrawal of money from an ATM. Find out more here.

Analysis: As mainstream storage suppliers have adopted and acquired HCI, NVMeoF, and object storage technologies and others, a set of startups have found themselves in a well-funded and long-life state in which they appear to have no short-term need of an IPO or acquisition – contravening conventional financial mores.

They appear in no danger of failing and are examples of companies defying typical startup wisdom that you need to IPO or get acquired within six years or so after receiving the first venture capital investment.

According to Statista, in 2020, VC-backed companies went public approximately 5.3 years after securing their first VC investment.

Let’s look at three possible outcomes for a startup:

IPO or positive acquisition – for example Snowflake IPO and Cleversafe acquisition.

In-between state – for example Panasas and many others.

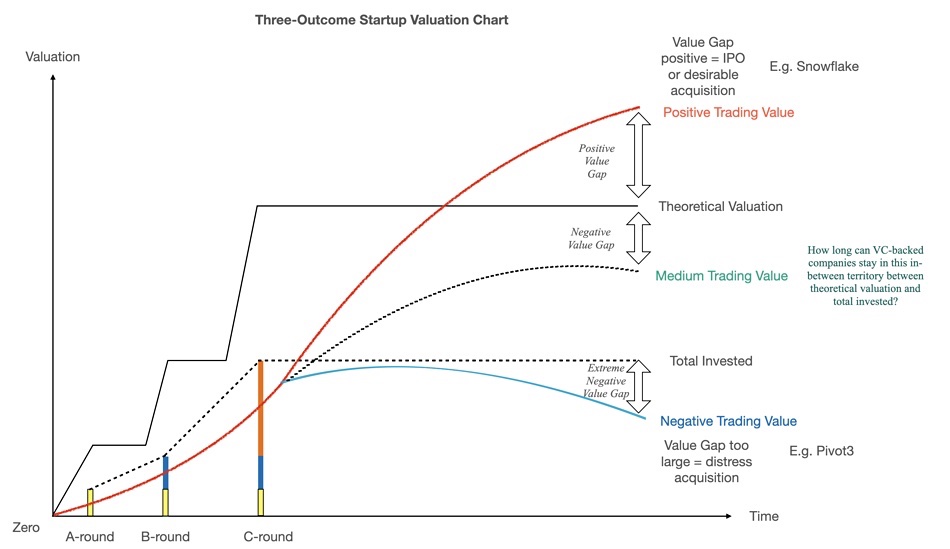

Blocks & Files chart

Above, we have devised a startup progress chart with these three possible outcomes plotted.

Chart explainer

The chart puts startups’ progress in a time versus valuation 2D space. The coloured bars are venture capital (VC) funding rounds and we show, as an example, A-, B- and C-rounds with the height of the bar representing total funding so far. The dashed line represents the total VC funds invested in the startup.

The solid line above this represents the company’s VC-calculated valuation at reach round. The red curve represents a theoretical startup’s progress as its trading value – what an acquirer would pay grows over time, surpasses the total invested amount and then rises further, past the theoretical valuation, putting the company in IPO territory as it approachers and passes that valuation. It has a positive trading value gap in our chart’s terminology.

At this point the VCs would get a good return on their investment if the company had an IPO or was acquired.

The blue line shows an under-performing startup whose trading value never rises above or drops below the total amount invested. There is an extreme negative value gap between the two and the VCs exit the company because it crashes – Coho Data and Tintri for example – or gets acquired as a distress purchase before bankruptcy, with Pivot3 as our cited example.

The middle, dotted, medium trading value line represents companies which don’t attain a trading value above their theoretical valuation but neither does their trading value drop below the total invested, giving the VCs hope that they will be able to achieve a good exit, eventually. We say these inbetweener companies have a negative value gap.

VC theoretical valuations

Niraj Tolia

How are VC valuations worked out? Kasten co-founder Niraj Tolia said “There is the theory that valuations should be based on discounted cash flows in the future but usually the reality is a lot more imprecise.”

Sometimes sane valuations for later stage companies will be based on “forward multiples” of, say, a multiple of the next 12 months projected revenue. Harder to do for an earlier stage company and that will then look at TAM and other market comps, founder histories, potential for exit and more.

“And, finally, there are some valuations that are simply hard to justify from the outside looking in. Might be a hot deal that got competitive and all metrics got thrown out of the window (like last year in a LOT of deals). Sometimes it’s what a founder can command based on a large vision.

“Basically, more art than science.”

Inbetweeners

Such companies can’t raise any additional funding and they either motor along in good medium trading value shape with adequate profitability, limp along with low profitability unless and until their VC backers want to exit with a closure or firesale or just cash burn themselves out of money. Perhaps a good example of this negative trading value state is Pivot3, a hyper-converged startup. It was started up in 2003 and took in a lot of money – $247 million across 12 funding events. Seventeen years after being founded it was bought by Quantum for $8.9 million, meaning a loss of $238 million for its backers.

What happened? The mainstream vendors built or acquired their HCI products and Pivot3 was not acquired. It then found that its effective addressable market shrank because the big beasts – Cisco (Springpath), Dell EMC (VxRAIL, vSAN), HPE (Nimble dHCI, Simplivity), NetApp (Elements HCI) and Nutanix – were roaming around and mopping up customers. Pivot3’s growth tailed off, faltered and stopped.

The COVID pandemic didn’t help and Pivot3’s board decided to get out of the HCI business.

Inbetweener status can be attained by any startup, whatever its funding amount. The tension between the aims of the VC backers (and most probably part-owners) meaning a good exit, and what the company’s executive leadership can deliver in terms of trading value is greatest in the well-funded in-betweeners. There is simply more VC money at risk.

Identifying inbetweeners

How might we identify long-life, well-funded inbetweener storage companies? Try this: we’ll look for VC-backed, $100 million-plus funded, post-startup suppliers, meaning more than five years since being funded, who have not significantly pivoted in the last few years. Here’s a starting list of $100 million-plus funded, “inbetweener” suppliers:

Databricks – $3.6 billion

Fivetran – $730 million

Cohesity – $600 million (IPO filed)

Rubrik – $552 million plus

OwnBackup – $507 million

Druva – $475 million

Dremio – $410 million

Qumulo – $351 million

Redis Labs – $347 million

Infinidat – $325 million

Silk – $313 million

Pensando – $313 million

Fungible – $311 million

Wasabi – $284 million

Firebolt – $269 million

SingleStore – $264 million

VAST Data – $263 million

Yellowbrick Data – $248 million

Clumio – $186 million

Cloudian – $173 million

Scality – $172 million

Nasuni – $167 million

Spin Memory – $166 million

Virtana – $165 million

Panasas – $155 Million

Liqid – $150 million

WEKA – $140 million

Egnyte – $138 million

MinIO – $126 million

Delphix – $124 million

Kyligence – $118 million

Datameer – $117 million

Pliops – $115 million

Pavilion Data Systems – $107 million

ExaGrid – $107 million

Scale Computing – $104 million

Elastic Search – $104 million

GoodData – $101 million

CTERA – $100 million

Now we’ll separate out those that are seven years old or older, classifying them as startups still:

Databricks – $3.6 billion and in 9th year

Fivetran – $730 million and in 10th year

Cohesity – $600 million and in 9th year (IPO filed)

Rubrik – $552 million+ and in 8th year

OwnBackup – $507 million and in 10th year

Druva – $475 million and in 14th year

Qumulo – $351 million and in 10th year

Redis Labs – $347 million and in 11th year

Infinidat – $325 million and in 12th year

Silk – $313 million and in 14th year (including Kaminario period)

SingleStore – $264 million and in 11th year

Yellowbrick Data – $248 million and in eighth year

Cloudian – $173 million and in 11th year

Scality – $172 million and in 13th year

Nasuni – $167 million and in 14th year

Spin Memory – $166 million and in 15th year

Virtana – $165 million and in 14th year (including Virtual Instruments period)

Panasas – $155 million and in 22nd year

WEKA – $140 million and in 9th year

Egnyte – $138 million and in 15th year

MinIO – $126 million and in 8th year

Delphix – $124 million and in 14th year

Nantero – $120 million and in 10th year

Datameer – $117 million and in 13th year

Pavilion Data Systems – $107 million and in 8th year

ExaGrid – $107 million and in 15th year

Scale Computing – $104 million and in 15th year

Elastic Search – $104 million and in 10th year

GoodData – $101 million and in 15th year

CTERA – $100 million and in 14th year

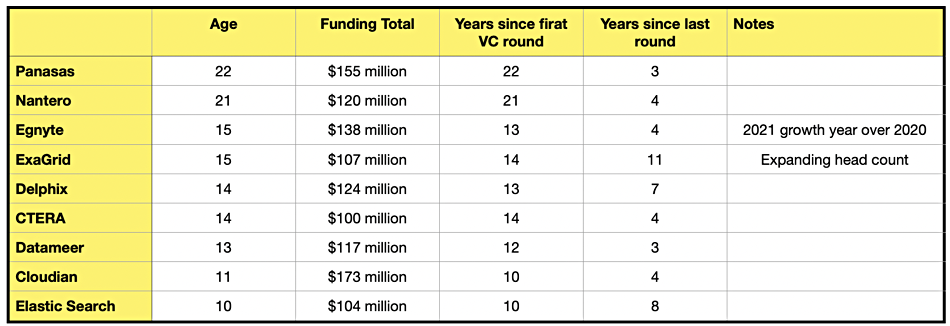

This gives 30 inbetweeener companies. Let’s find out the longest-lived and best-funded ones by putting them in age order, add in the time since the last funding event, and strike out companies less than ten years old, or with two years or less since their last round.

Extreme inbetweeners

We now have nine extreme “inbetweener” companies who are ten years or more old, have $100 million or more in funding, it is ten years or more since their first VC round, and their last funding round was three or more years ago. If asked, all would say they are growing and in good shape. None of them are closing offices or laying off staff. They exhibit no signs of financial stress as far as we can see. Indeed some are visibly and publicly growing, such as Egnyte and ExaGrid.

The current storage market supports – indeed seems to welcome – these players, as they continue to develop and grow their businesses. Long may it continue and let’s hope that their VC backers find some way to crystallise their investments without the company getting into dire straits. There needs to be, we might say, some way for the holdings of the relatively short-termist VC investors to be turned into the holdings of more, benevolent and long-term investors.

Perhaps a long-term view private equity acquisition, meaning not a slash-and-burn reorganising one, is one possible good outcome.

Wikipedia public domain image: https://commons.wikimedia.org/wiki/File:C_Merculiano_-_Cephalopoda_1.jpg

Big Blue’s big Red Hat open source business unit is adding Ceph-based persistent storage services to its OpenShift containerised app software services.

OpenShift Data Foundation offers cloud-native persistent storage, data management and data protection. It is based on Ceph, Noobaa and Rook software components. Ceph provides object, block and file storage. Noobaa, acquired by Red Hat in 2018, is an abstraction layer over a storage infrastructure and provides data storage service management across hybrid multi-cloud environments. Rook, which can be used to set up a Ceph cluster, orchestrates multiple storage services, each with a Kubernetes operator.

Joe Fernandes, Red Hat’s cloud platforms VP and GM, provided the standard announcement quote: “Red Hat OpenShift Platform Plus provides the innovation of Kubernetes tailored for enterprise needs, along with a broad set of additional capabilities like management, enhanced security features and now storage out of the box, answering common production requirements that basic Kubernetes services cannot address.”

Red Hat OpenShift is now a more complete Kubernetes app development, deployment and secure software stack. This comes from adding the OpenShift Data Foundation product to a Red Hat OpenShift Platform Plus bundle, now made up of:

OpenShift;

Advanced Cluster Management for Kubernetes;

Advanced Cluster Security for Kubernetes;

Quay (Central registry);

OpenShift Data Foundation (previously called Container Services).

The latest version of OpenShift Data Foundation, 4.9, includes multi-cloud object gateway namespace buckets. These enable data to reside in a single location while also being made available on alternative locations where applications need access, without having to copy data over to the alternative location.

It also has persistent volume encryption in which users can bring their own key, and manage and hold encryption keys separate from their cluster.

Red Hat OpenShift Platform Plus is available now and the Data Foundation offering is added it in two ways. Red Hat customers who have an active Red Hat OpenShift Platform Plus subscription receive OpenShift Data Foundation Essentials as part of their existing subscription at no extra cost.

A Red Hat OpenShift Platform Plus with Red Hat OpenShift Data Foundation Advanced bundle, adds security features, multi-cluster workload support, disaster recovery, and standalone and mixed use storage support to the Essentials offering.

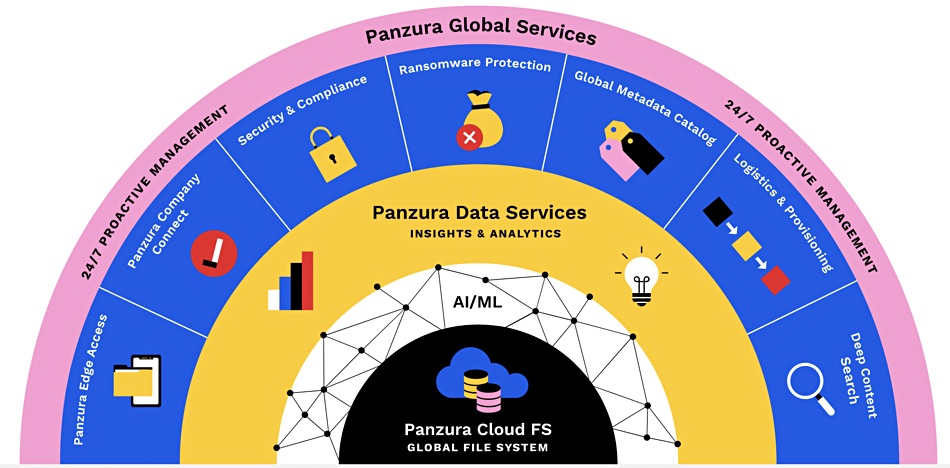

Cloud file sync-and-sharer Panzura has upped its game three ways: cloud outage failover, shared NFS and SMB access, and Hyper-V support.

This so-called Data Flex release means Panzura’s CloudFS customers need no longer suffer an outage when their cloud goes down, can have SMB and NFS users access the same files at the same time, and Hyper-V hypervisor users as well as VMware vSphere users get access to Panzura’s facilities.

The announcement quote came from Panzura’s chief innovation officer, Edward M.L. Peters: “Our customers operate in an environment that can span virtualizations and cloud providers. It only makes sense that they want a simplified way to access, share and collaborate on files no matter what multi-hypervisor or multi-cloud configuration they use.”

Cloud outage failover is provided through a cloud mirroring feature and it enables, Panzura says, enterprise-grade high availability, built-in multi-cloud orchestration, and automation. CloudFS simultaneously places the same set of data in two separate object stores in real time, providing multi-cloud redundancy. If there is a primary cloud outage or security issue with one cloud provider CloudFS can immediately failover data, applications and workloads to a secondary cloud provider, an organisation’s private cloud, or both.

Users can seamlessly continue work with no loss of data while the primary object store remains offline. Cloud FS re-syncs the impacted storage volumes when they come back online. Panzura customers get more uptime and can also remain in compliance with strict SLAs for regulatory and contractual uptime mandates.

Peters said “When you lose access to crucial data, financial losses mount with every minute that passes – and the reputational damage can be crippling. With the new failover capabilities of Panzura CloudFS, you will continue working as if an outage never happened.”

The mixed NFS-SMB mode allows users with file shares and storage via both NFS and SMB connections to access, share and update the same data, eliminating redundant workflows and data silos.

Panzura’s Hyper-V support enables IT departments to consolidate data and native applications for Microsoft SQL Server, Microsoft Exchange and Microsoft SharePoint that require low latency and high-performance access, backup and storage, onto Cloud FS. This, together with shared NFS-SMB access and cloud high availability, ups Panzura’s enterprise credentials considerably.

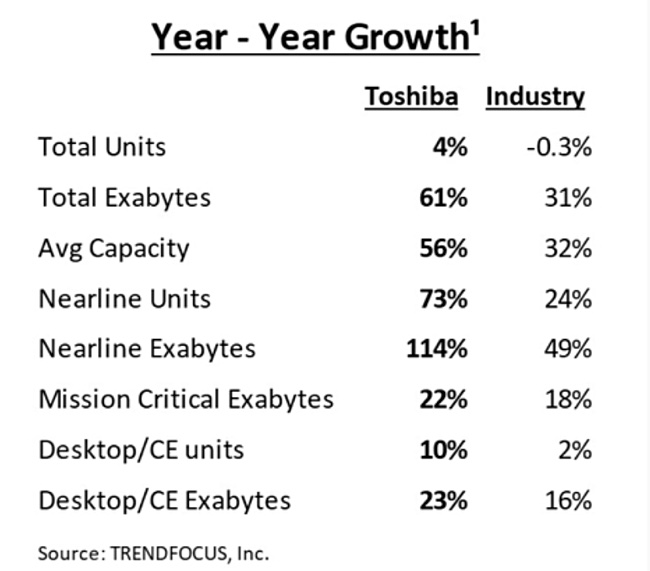

Toshiba was the only one of the big three disk drive manufacturers to increase its unit shipments in 2021, with exabytes shipped rising faster than the market average as well.

Disk unit shipments have been declining for several years as faster SSDs take over from slower, albeit cheaper, disk drives in notebook and desktop computers as well as performance-critical storage arrays. However, within the overall market, the 3.5-inch 7,200rpm (nearline) disk segment has been growing both unit numbers and exabytes shipped – so much so that overall disk capacity shipments have continued to rise while disk unit shipments decline.

US research house TrendFocus tracks the HDD market and its VP John Chen said “Toshiba’s leading year-over-year growth percentages in so many categories are the result of the company’s execution under challenging market conditions. … As some of the ongoing pandemic-related constraints begin to ease, Toshiba has positive momentum to post more milestones in 2022.”

Kyle Yamamoto, VP of Toshiba America Electronic Components’ (TAEC) HDD Business Unit, said “Our new technologies such as FC-MAMR (Flux-Controlled Microwave-Assisted Magnetic Recording) and MAS-MAMR (Microwave Assisted Switching Microwave-Assisted Magnetic Recording) are excellent examples of the effort that will propel the next generation of products forward.”

Toshiba shipped 54.68 million units equaling 187.24 exabytes for the year. It ships product into four products into four market sectors:

AL series – mission-critical enterprise performance segment;

MG series – nearline enterprise capacity and datacentre drives;

MQ series – mobile client HDDs;

DT series – surveillance and traditional desktop drives (3.5-inch).

TrendForce’s latest report shows that Toshiba grew unit and capacity shipments more than the market average in overall totals, nearline drives (MG series), mission-critical (2.5-inch and 10,000rpm) drives (AL series) and the desktop/consumer electronics (DT series) sectors.

That means competitors Seagate and Western Digital collectively lost share in these market sectors. We envisage that Toshiba was able to better manage its supply chain than the other two suppliers, who both alluded to supply chain issues in their results statements – here’s Western Digital and here’s Seagate.

Toshiba’s 2021 nearline exabytes shipped growth of 114 per cent more than in 2020 looks extraordinary against the industry average of, impressive as it is, 49 per cent.

In the final 2021 quarter Toshiba had a near-20 per cent unit ship share, Western Digital near-37 per cent and Seagate near-43-percent. Toshiba will have to keep growing its share for some time if it wants to get past Western Digital.

All-flash array vendor Pure Storage is partnering with IBM infrastructure services spin-off Kyndryl in a global alliance.

Kyndryl says it will become a key delivery partner for Pure and deliver jointly-optimised software and hardware to its enterprise customers, of which it has more than 4,000 – including 75 per cent of the Fortune 500. The company will increase its existing Pure skills and capabilities.

Stephen Leonard.

Stephen Leonard, Kyndryl’s global alliances & partnerships leader, provided a good formulaic announcement quote: “Our alliance with Pure Storage can help customers identify and take advantage of new ways to manage, secure, and analyse their mission-critical multi-cloud business data.”

Wendy Stusrud, VP, global partner sales at Pure Storage, matched it: “We’ve fostered a true collaboration with Kyndryl that will address our shared customers’ business challenges and drive the transformation and modernisation they are undertaking.”

Pure and Kyndryl say they will deliver systems related to application and infrastructure modernisation, automation, multi-cloud management, containerisation, and more. They will provide cyber resiliency elements natively at the storage layer to enable cloud-based applications coupled with data portability in the cloud or on-premises.

It’s good news for Pure, with Kyndryl recognising its enterprise credentials as a storage supplier.

Pure is joining august company. Kyndryl also partners with AWS, Cisco, Google Cloud, IBM, Lenovo, NetApp, Red Hat, SAP and VMware. And, in November 2021, Microsoft became Kyndryl’s only Premier Global Alliance Partner increasing Microsoft’s access to the $500 billion managed services market which Kyndryl leads and enhancing prospects for Azure’s use.

That means Dell Technologies and HPE are not in Kyndryl’s partner list. Yet.

Clearlake Capital Group has completed its previously announced acquisition of Quest Software, a global cybersecurity, data intelligence, and IT operations management software provider, from Francisco Partners. Quest CEO Patrick Nichols will continue to lead the Company supported by the existing executive management team. Terms of the transaction were not disclosed.

…

DDN and Shakti Software, a provider of ultra-high performance database analytics, announced record breaking STAC-M3 benchmark results with a system including Shakti’s data platform running on a single client server combined with DDN’s SFA200NVX storage appliance. Shakti’s data platform was created by world renowned computer scientist Arthur Whitney, who created the A+ programming language (used by Morgan Stanley) and founded the data analysis company KX. Results from the baseline (Antuco) suite of STAC-M3 benchmark tests run on Shakti 2.0 include:

The highest storage efficiency (least storage used for the same database size) of any publicly reported solution.

NBBO results 1.7x the speed of the best previously published results for a less-demanding version of the benchmark.

Faster results in several mean-response time benchmarks versus a solution involving kdb+, including:

3.7x the speed in the version of Year-High Bid that allows caching

3.3x the speed in NBBO vs the less-demanding version of the benchmark

…

Exasol, which claims it’s the developer of the world’s fastest in-memory database, announced its availability as a Software-as-a-Service (SaaS) model on Amazon Web Services. Exasol can also run on a customer’s chosen cloud of choice, on-premises or in hybrid mode. There are two versions: SaaS Standard Edition is best for organisations with smaller data volumes who don’t need advanced analytics and data integration features or extended support, and SaaS Enterprise Edition for enterprises with larger data volumes. It comes with extended support. This is good for organisations that require multi-departmental analytics environments, perform machine learning or AI in the database, or have complex requirements for data integration or virtualization.

…

Keepit, a cloud backup and recovery supplier with an independent vendor-neutral and blockchain-based cloud dedicated to SaaS data protection, announced its software now includes support for Microsoft Azure Active Directory (AD). Future updates, which will include support for additional Microsoft services including Microsoft Endpoint Manager, and Conditional Access Policies, will result in Keepit coverage for all essential MS cloud services.

…

SoftIron, which builds hardware and software Ceph-based appliances, has partnered with SUSE to provide integration support for SoftIron’s HyperDrive storage appliances using HyperDrive Storage Plugin for SUSE Rancher. Located in the SUSE Rancher Apps & Marketplace, developers using SUSE Rancher, the enterprise Kubernetes management system, can integrate and manage SoftIron HyperDrive capabilities through the SUSE Rancher container management platform, providing the flexibility of Ceph’s object, block, and file storage protocols in a single unified storage system.

…

Teradata announced a global partnership with Microsoft to integrate its Teradata Vantage data platform with Microsoft Azure. Teradata Vantage on Azure is already heavily integrated with the Azure ecosystem, including Power BI, Synapse Analytics, and more than 60 Azure data services. More information here.

…

Hybrid cloud data warehouser Yellowbrick Data announced a strategic partnership with Nippon Information and Communication Corporation (NI+C). The two say that enterprises like NI+C that serve the telecommunications, transportation, and banking industries in Japan rely on the Yellowbrick Data Warehouse to power critical business outcomes, facilitate data sharing and replication, and maximise the flexibility of multi-tenant billing. NI+C was founded by NTT and IBM Japan in 1985 and has developed as a systems integrator,

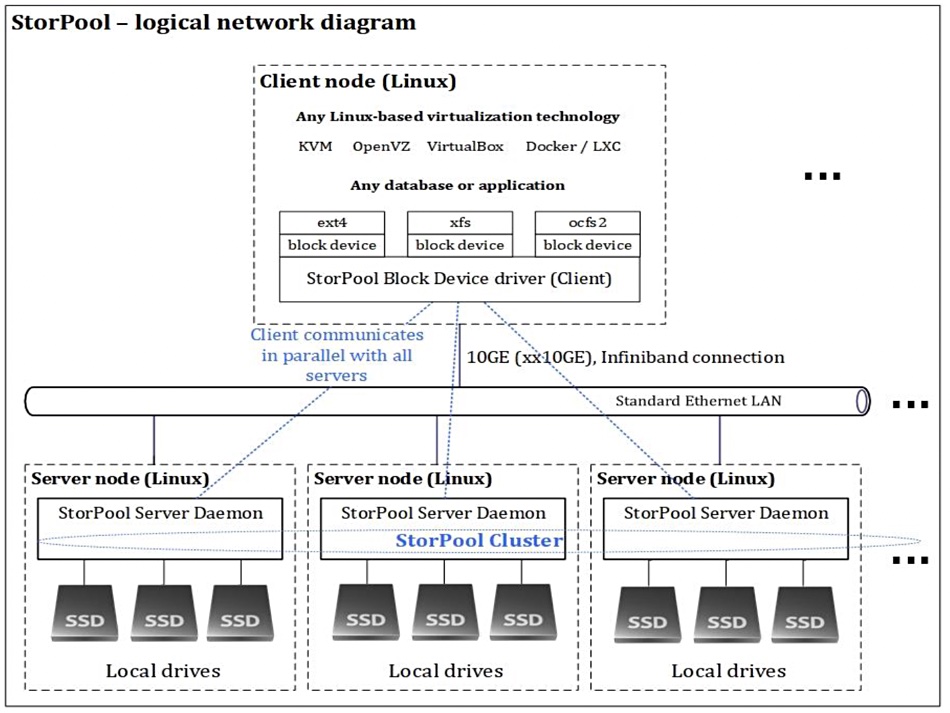

StorPool grew revenues by 30 per cent year-over-year in 2021 and has introduced a new version of its software with a mass of improvements.

Boyan Ivanov.

The product is scale-out, shared block storage software which runs on Linux and pools disk and SSD capacity resources across a cluster of commodity servers. Version 19.4, delivered six months after v19.3, has better speed, agility, reliability, updated hardware and software compatibility, management and monitoring changes, and improvements in the business continuity area. It includes support for up to 16 server Instances per node, an updated metadata structure, support for OpenNebula version 6.2 and much more – there’s a list here.

Boyan Ivanov, StorPool CEO & co-founder, issued a statement: “2021 was a successful year for StorPool with increased customer traction, numerous product improvements and valuable new team members joining the company.”

StorPool increased its headcount by an average of 25 per cent in 2020 and 2021. It says it is one of the few cash-flow-positive storage vendors in the world and is enjoying double- and triple-digit growth. It also has a 92 per cent Net Promoter Score.

Alex Ivanov, product lead at StorPool Storage, said “We keep advancing StorPool Storage to meet the product maturity expectations of current and potential customers, especially power users with large-scale clouds like IT services providers and SaaS/e-commerce leaders.”

Infinidat has appointed Troy Fortune as the president of Infinidat Federal, Inc. Previously he was VP and GM for immixGroup, the public sector business unit of Arrow Electronics. Infinidat CEO Phil Bullinger said “Adding Troy to our senior management team continues the strategic extension of our go-to-market abilities with strong industry leaders and broad investment in scaling our market reach. Infinidat Federal is extremely well positioned for 2022 as we build on our unprecedented growth in 2021.”

…

Park Place Technologies, a global datacentre and networking optimisation firm, has purchased Congruity360’s Storfirst software platform. Storfirst, it says, is the industry’s most secure, OEM- and platform-agnostic (cloud, hybrid cloud and on-premises) file system migration and information management software. It allows customers to manage data movement from production servers to disaster recovery servers, on-premises and to the cloud; controlling the movement of all file data. Chris Adams, Park Place Technologies president and CEO, said: “Storfirst’s ability to aggregate unstructured data and run analytics puts customers in the driver seat, empowering them to manage their data while reducing costs.”

…

Regatta is hiring. The three-year-old startup’s eponymous Regatta product is a mission-critical, extreme performance transactional and analytical database. It is is elastic and infinitely scalable – deployable from a single node to clusters of tens of thousands of nodes that may store hundreds of petabytes of data. Regatta was started up by founding ScaleIO executives – CEO Boaz Palgi, CTO Erez Webman and VP Engineering Eran Borovik – with offices in San Francisco and Haifa, Israel. ScaleIO was bought by EMC in June 2013 for $200 million.

…

Replicator WANdisco is growing and made reorganisation and cost-control moves in 2021. It saw strong trading in Q4, following significant contract wins both directly and with its key cloud channel partners including Azure, AWS and IBM, as well as its principal analytics partners Databricks and Snowflake. Q4 bookings increased 30 per cent to $8.4 million from $6.5 million in Q4 2020. For FY21, bookings increased 17 per cent to $11.9 million from $10.2 million in the prior period. Toward the end of FY21, the company carried out a sales reorganisation and effective cost management. WANdisco’s year-end cash position is expected to be approximately $27.8 million – a 32 per cent increase on the prior year, with $1.2 million in trade receivables. It sees significant market opportunities in IoT-driven deals and expansion into new verticals in the coming year.

All-flash storage supplier VAST Data has international expansion and development plans for Europe and Asia.

VAST has opened up operations in the UK, France, Germany, Israel, Turkey, Czech Republic, Middle East, Australia, New Zealand, Russia and Korea. These are being followed by further expansion across EMEA with Benelux, Switzerland, Italy, Spain and the Nordics, and in Asia with Japan.

Renen Hallak, founder and CEO of VAST Data, issued a statement: “In just a few short years we’ve become one of the fastest growing storage companies ever, disrupting a stagnant marketplace and challenging the status quo to solve old storage dilemmas for the new data-driven world.”

Stagnant indeed. Quite a few startups and incumbents would disagree with that sentiment.

Peter Gadd, international VP, said: “We have great technology, we have a great team and we have a great partner network. The market opportunity is huge and we are well primed to take advantage of the seismic shifts we see in data and storage over the next few years.”

VAST has also signed agreements with distribution partners across its international territories including Spinnaker in the UK, Arrow Electronics in Europe, Logicom in the Middle East and Africa, TechData in Australia, ASI in New Zealand and ASBISC Enterprises PLC in Russia, as well as Eastern and Central Europe.

All territories will be supported by in-region sales, technical support, marketing and customer services functions.

Hallak said “The plan now is to scale our Universal Storage platform into International markets, helping enterprises meet the challenges of exponential data growth, access complexity and speed. We believe it’s time for modern enterprises to rethink the whole data and storage landscape to take advantage and leverage the benefits of ‘clouds of flash’ for their AI, analytics and data protection strategies.”

There were some punchy customer comments accompanying VAST’s announcement.

Simon Blackler, CEO at Krystal, a UK based internet services company: “With VAST we can out-service and out-innovate the cloud giants, enabling us to deliver our customers shared services with higher performance at a lower price point.”

Tim Scheurenbrand, director of IT at Germany-based bioinformatics outfit CeGaT: “VAST’s all-flash storage … allowed us to reduce the time taken to process sample data from 24–48 hours to just two hours.”

Comment

VAST is taking full advantage of the price/performance window provided by its all-QLC flash, Optane-enhanced, single-tier scale-out Universal Storage product technology. It should be able to reproduce the success it has had in North America in the Europe, MiddleEast and Asia-Pacific regions. Latin America, it appears, will have to wait.

Assuming good progress then, in 12 months time, VAST’s revenues could be increased by 50 per cent or more. Such business expansion will surely result in an IPO or an acquisition.

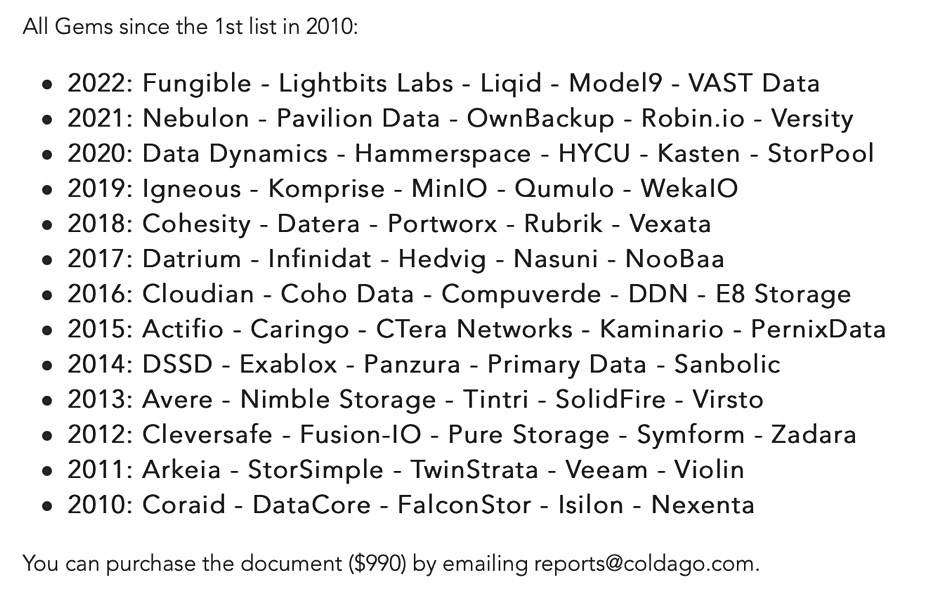

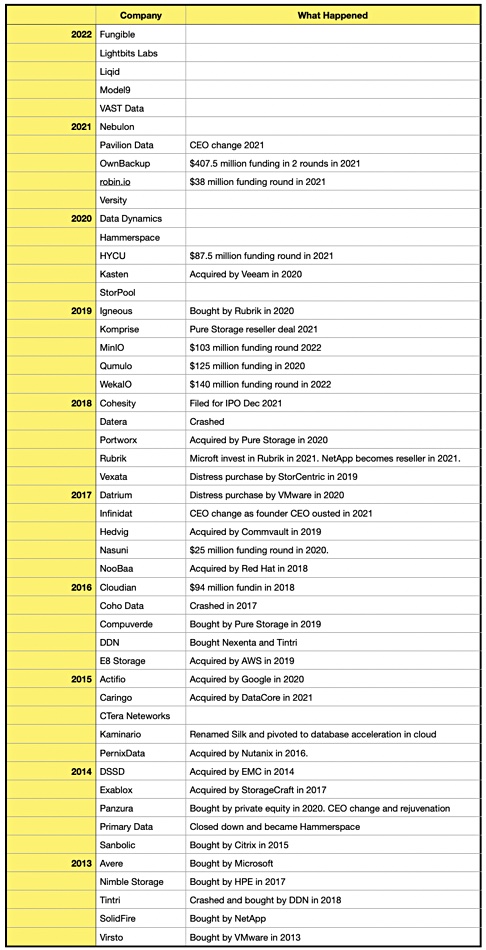

Storage industry research outfit Coldago has released a Gems report showing showing five players to watch in the coming months. The five nominees were named “as a result of a their vision, product development and execution with a serious aspect on the technology and product innovations.” They are Fungible, Lightbits, Liqid, Model9 and VAST Data. The complete list is:

We looked back at the past 12 years of Gems reports to see what’s happened to each year’s five nominees:

Twenty two out of the fifty have been bought. Two have crashed: Coho Data and Datera. Two have pivoted/rebranded/evolved: Kaminario became Silk and Primary Data became Hammerspace. Eight have had fresh funding rounds and one – Cohesity – has filed for an IPO.

Twenty five acquisitions (three in distress) versus two crashes. Looks like a decent hit rate for Coldago.

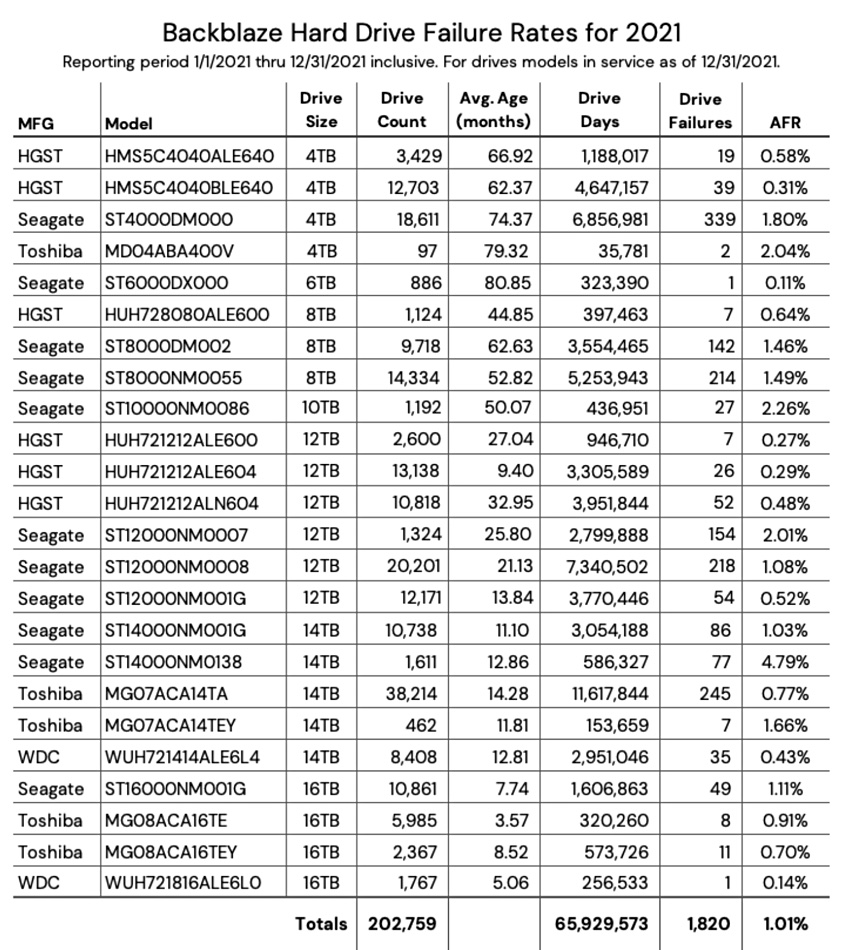

The 2021 disk drive stats from CSP Backblaze showed that the 6TB Seagate – model: ST6000DX000, the oldest in its fleet at an average adage of 80.4 months – had the lowest failure rate of any drive, with an annualised failure rate (AFR) of 0.11 per cent. Two recent drive purchases are doing well: the 16TB WDC drive (model: WUH721816ALE6L0) has an average age of 5.06 months and an AFR of 0.14 per cent and the 16TB Toshiba (model: MG08ACA16TE) has an average age of 3.57 months and an AFR of 0.91 pure cent. We reproduce Backblaze’s drive stats table here:

…

CDS, a provider of multi-vendor services (MVS) for datacentres worldwide, achieved its highest annual revenue ever on 21 per cent revenue growth compared with 2020, significantly improved profitability, expanded relationships with its OEM partners, and added more than 600 new enterprise customers during the year.

…

Data protector Cobalt Iron has been awarded patent number 11212304, which describes new capabilities for Cobalt Iron Compass, its enterprise SaaS backup platform, whereby Compass will automatically reconfigure IT infrastructure when it detects cyber threats, such as a ransomware attack. It will dynamically adjust access to backup infrastructure and data to reduce exposures to cyber attacks. It can also provide analytics-based insights into an attack and automatically perform various operations to further secure data.

…

Data protector Commvault has acquired Israel-based TrapX, a cyber deception firm, to enhance Commvault customers’ capability to proactively detect, defend, and recover from unknown threats. TrapX lures malware actors in with authentic traps that engage attackers, collect TTPs and trigger alerts. It’s massively scalable, flexible and fast, and TrapX can deploy >500 unique traps per appliance in less than five minutes. TrapX was founded in 2012, has raised $47.7 million in four rounds of funding, has more than 300 customers world-wide, and calls itself the world’s leading cyber deception platform. A Commvault blog claims “We believe this new acquisition will set Commvault apart as the only vendor in our industry to offer customers active data management capabilities that are integrated with their security investments.” TrapX technology will be integrated into Commvault’s Metallic SaaS offering.

…

File and object storage supplier and protector Quantum released ESG survey data that reveals the most common challenges organisations struggle with around effective data management, storage and analysis. It found respondents see unstructured data as under-leveraged and overly complex. Data quality and storage costs most often inhibit data management strategies. Data retention is top of mind and organisations struggle with when to delete or store data. Data sprawl and hybrid cloud models create vulnerable environments. Growing cyber security threats require new approaches. Organisations need a data management strategy to cope with these things.

…

Veritas has appointed Lawrence Wong as its first chief strategy officer. He’s also an SVP. Wong’s role is to partner with other Veritas leaders to develop and execute a comprehensive cloud strategy and he will lead the company’s corporate growth strategy and acquisition efforts. He will report to CEO Greg Hughes and be a part of the Veritas Leadership Team. Most recently he was at Accenture, acting as managing director and member of the Global Leadership Council (GLC). He has also held leadership roles at McKinsey & Company and HPE.

Veritas saw CMO Todd Forsythe depart to be an exec partner at Gartner in December last year. CTO Cameron Bahar left towards the end of 2020. Veritas currently lists no CTO or CMO on its leadership web page.

…

ReRAM startup Weebit Nano has appointed ReRAM and non-volatile memory (NVM) expert Gabriel Molas as chief scientist. It has recruited him from its research partner CEO-Leti where Molas researched NVM for the past 17 years, leading numerous ReRAM research projects including work with Weebit’s ReRAM. Molas said “I am excited to join Weebit as the Company moves to commercialisation. Over the past decade, ReRAM technology has continued to mature, and it is now poised to become a mainstream non-volatile memory alternative. Weebit’s ReRAM is particularly well positioned for success in both traditional memory and AI applications.” He is an IEEE Senior Member – an achievement that recognises his more than 150 international conference publications, 50 papers in peer-reviewed journals, and 25 patents.