All-singing, all-dancing TASS (Transcendent Abstracted Storage System) supplier 22dot6 has updated its Valence software — making it easier to set up and operate private, hybrid, and public cloud storage.

22dot6 is not your usual storage supplier. It was founded in 2015, has just five staff listed in LinkedIn, and no known external funding. Hammerspace-like Valence was first announced in May and, as of now, we don’t know how many customers 22dot 6 has for the software.

Diamond Lauffin.

But its founder, Diamond Lauffin, has a long-term storage industry track record — co-founding, for example, Nexsan and being an EVP sales at Qualstar from 1993 to 2000. In other words, take it seriously.

Valence VSR storage controller.

A Lauffin announcement statement said: “Most enterprise storage managers are getting pressure from upstairs to shift to the cloud, but often times it is difficult for executives not on the front line to understand what’s actually involved in this process, and how complicated it can be. A TASS architecture is the answer, and from sunrise to sunset the Valence Cloud Suite combines the features and optimal practices required for enterprise level data management in the cloud.”

This Valence Cloud Suite release adds:

Point-and-click private cloud setup;

Unifies private and public clouds into a single pool;

Cloud-to-cloud data migrations and reverse migrations with no pointers, links or stub files;

Transparent, multi-protocol, cross-platform support for all security and permissions with a single point-and-click;

Metadata-level analytics, lookups and data reports of public cloud data;

Individual, file-level data integrity audits that run transparently in the background and provide a red light/green light analysis of all data, protecting against file deletion, modification, corruption, or disappearance;

Geographic control over where data subject to regulation is located and file level data immutability.

Comment

We know of no independent analysis of the TASS software, and no evidence of 22dot6 engagement with analysts like Gartner, Forrester, ESG or the Evaluator Group. Contact 22dot6 to find out more.

This could be great storage software and have its use grow quickly, or it could be a storage curio — terrific in its own right but not a mass-market product. Keep your eyes on it just in case.

An Arcserve announcement appears to have had an embargo breakdown or similar event, as SecurityBrief Asia has put out a story — “Arcserve partners with Google Cloud to deliver cloud business continuity solution” — which is dated 11 November 2021. It describes the availability of Arcserve Cloud Services (DRaaS) on the Google Cloud Platform.

…

A DoKC (Data on Kubernetes Community) report entitled “Data on Kubernetes 2021” surveyed 500 Kubernetes-using respondents and found half of them are running half or more of their production workloads on it. Some 90 per cent believe it is ready for stateful workloads, and 70 per cent are running them in production. DoKC is a Kubernetes supplier trade group with levels of membership. Top level (platinum) members are DataStax, EDB, MayaData (bought by DataCore) and Pure-owned Portworx.

…

Taiwan-based contract semiconductor manufacturer United Microelectronics Corp. (UMC) is paying an undisclosed sum to Micron as the price of the legal action between the two being dropped. UMC pled guilty to Micron DRAM IP theft in October last year and was fined $60 million by the USA. The stolen IP was passed to China’s Fujian Jinhua which wanted it for DRAM manufacturing.

…

OWC Mercury Elite Pro mini.

OWC has updated its OWC Mercury Elite Pro mini portable flash drive with USB-C support, delivering up to 542MB/sec real-world performance. Drive capacities are 480GB, 1TB, 2TB and 4TB — or you can buy the product with flash drive and stick one in yourself. The 480GB model is priced at $94.

…

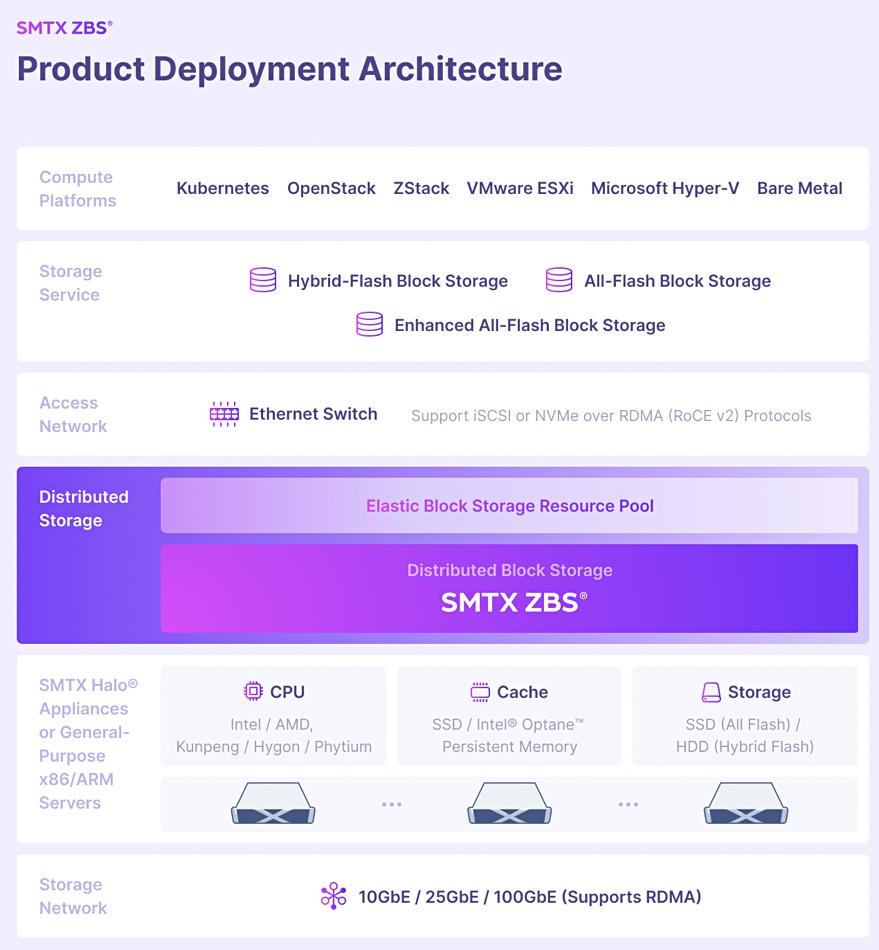

China-based SmartX has announced version 5.0 of its SMTX ZBS distributed block storage product which can deliver 770,000 4K random read IOPS from a 3-node cluster. V5.0 introduces support for RoCE v2, NVMe-oF (alongside existing iSCSI support) and Optane Persistent Memory. It can provide 8GB/sec bandwidth for 256K sequential reads, saying this is close to the physical limit with a 25GbitE network card.

…

Richard Henderson, technical director at TigerGraph, believes that, in 2022, “digital twins” will appear everywhere, and be based on real-time analytic graph databases. A digital twin is a real-time model of a business and its environment. It provides, he says, a complete and current view of the physical business situation, using the business events and data that are probably already available in individual operational silos and data marts. This, combined with graph analytics, can deliver a detailed and immediate digital scenario, showing the impact and risk associated with any delays or failures within that network. Graph analytics will combine these individual events and the map of the network to produce a “zoomable” big picture view of the entire operation.

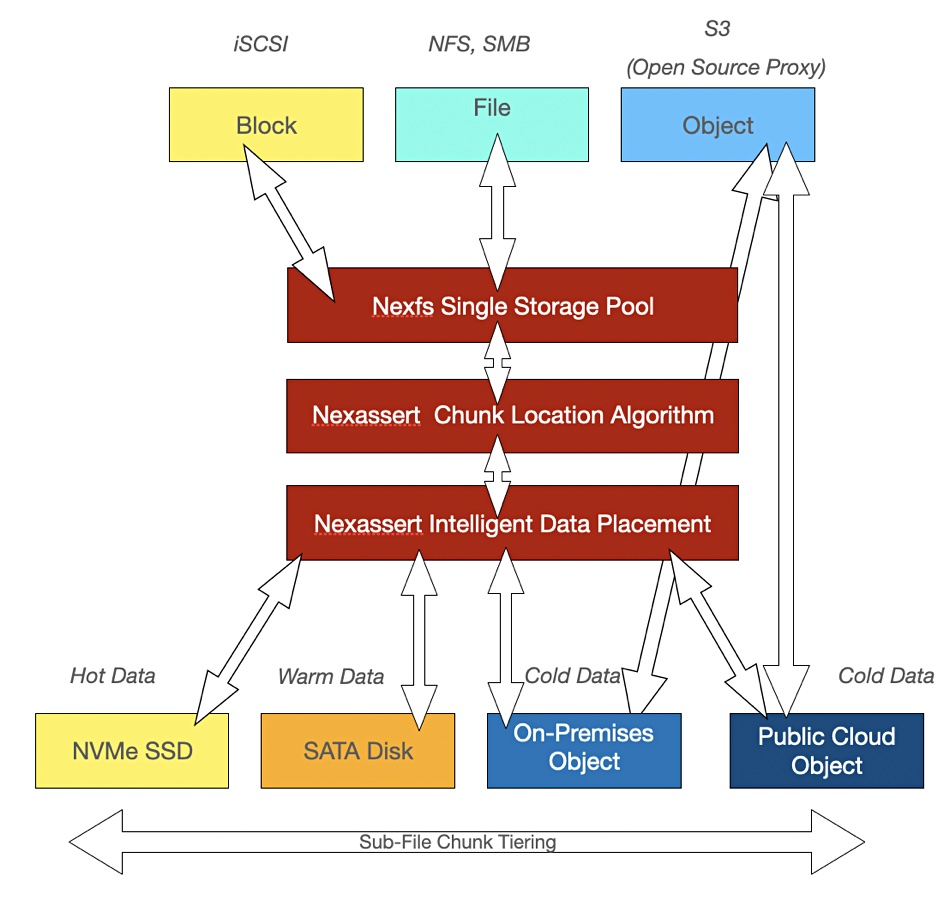

NexuStorage’s Nexfs software serves block and file data from an object-backing store using sub-file chunking to reduce data movement and help data tiering, and claims great tier-one storage cost savings and good performance.

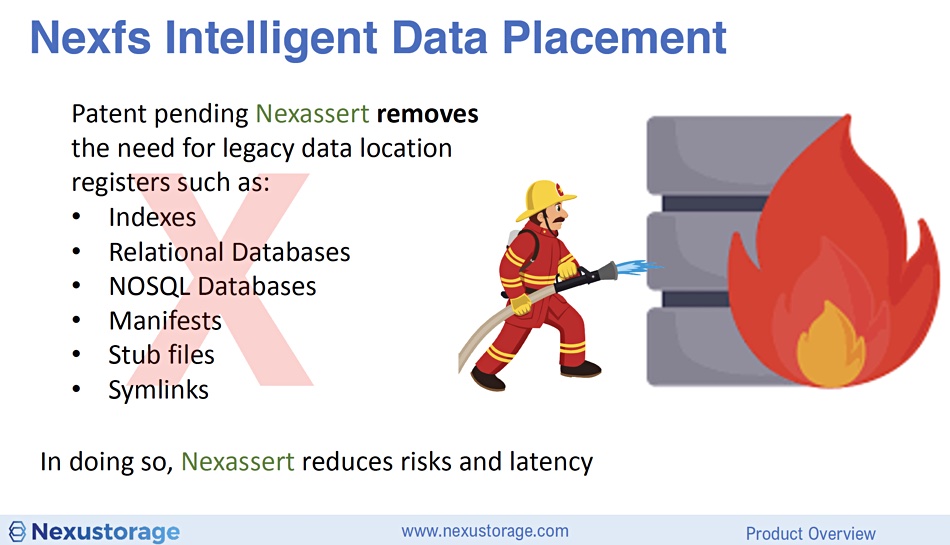

It has devised Nextassert software to do this without traditional data mapping indices, relational or NoSQL databases, manifests, stub files or symlinks. The company is a nine-month-old founder-funded startup based in New Zealand, and briefed a virtual IT Press Tour on its technology

Founder Glen Olsen, an ex-product manager at DataCore-acquired Caringo, said his Nexfs technology removes the gap between the worlds of file and block storage on the one hand and object storage on the other, with the object storage either on-premises or in the public cloud. Nexfs delivers, he said, a unified, intelligent, cost-effective, massively scalable, data-lifecycle-enabled, storage system that can provide an up to 95 per cent reduction in primary storage capacity.

The software runs on industry-standard servers and is available as a no-charge, downloadable Community Edition, with subscription-based, SLA-backed support coming soon.

Nexfs

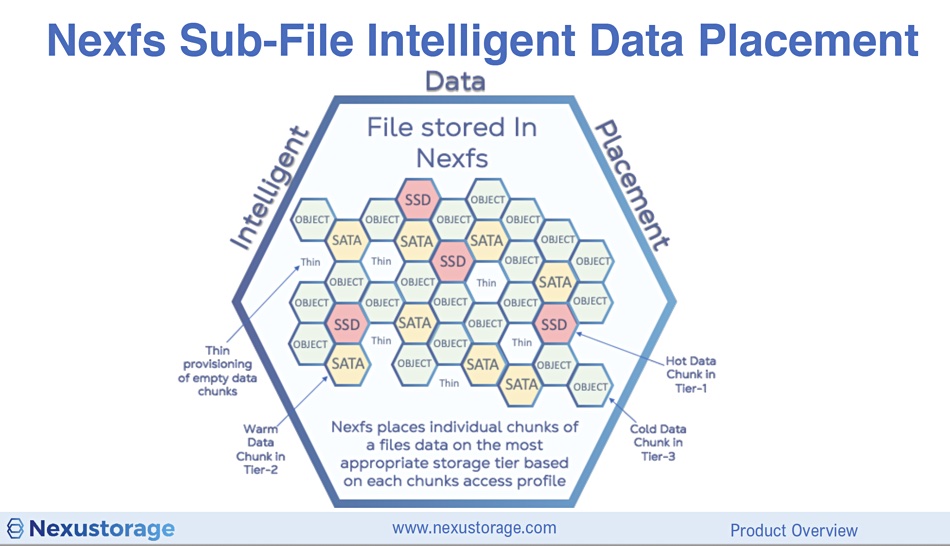

Nexfs is a file system. It splits files into chunks of between 1MB and 8MB in size and stores these chunks on three tiers of media: fast SSDs, slower SATA disk drives, and slower-still object storage. Nexfs presents data through either block or file interfaces, with iSCSI, NFS and SMB/CIFS interfaces supported. There is no direct access to the underlying object storage, although an open source web proxy providing S3 access is on the roadmap.

Blocks & Files diagram.

Chunks are placed on the hot, warm or cold tiers according to their access profile or personality and can be moved up or down a tier by a SmartTier function. This background process uses low and high tide so-called watermarks to decide if and when and how aggressively to move data between the tiers, with object storage regarded as the infinitely scalable back-end. Its migration of data between tiers can be triggered by file closure, a change in a file data chunk, and/or according to a set time schedule.

SmartProtect automatically copies data in the hot tier to the cold object tier and also copies POSIX file metadata to the hot tier and to the object tier. This means primary data is still available after a drive or system failure.

SmartClone puts cloned copies of files on an object storage tier for protection or distribution. If a single client changes part of the file, the changed chunks are unique to that client.

The actual storage hardware can be local drives on servers, a SAN, or on-premises object stores — for example, from MinIO, Cloudian and Scality, and AWS. The object access method is S3.

Because the underlying file data is chunked, its access time is lower than that needed for a full file access. Chunks from a file can reside on different tiers:

In effect a chunk is an object, and sets of chunks make up a file or, in the block case, a volume. There can be millions of chunks, and mapping their location on the storage drives and their relationship with their parent file is what the Nextassert software accomplishes.

Nextassert

NexuStorage claims its sub-file chunk technology with Nexassert allows massive multi-terabyte sized files to be stored in the cloud or object storage and treated as though they reside on traditional block storage.

Olsen said data mapping indices, databases or manifests are a performance bottleneck and can cause data loss if they are corrupted or destroyed. Nextassert sidesteps both problems.

He said: “This works because we don’t have a data location index and Nexfs can actually calculate where the data is.” Nexassert patent-pending software can (apparently) directly locate and access data belonging to a single file that resides on different storage classes without maintaining a separate index or manifest. How? We don’t know.

Olsen’s LinkedIn profile says he has filed a patent called “Addressing file data chunks over a REST interface without maintaining a file data chunk database, index or manifest.” We haven’t been able to find any more details than this.

It seems to us that the Nextassert technology will be crucial to the delivery of Nexfs’s performance and scalability.

NexuStorage company

Glen Olsen is the founder, funder and CEO of NexuStorage. Development has been done by up to 50 external contractors. This is the typical Silicon Valley startup business model, and it’s not unusual according to him. The entire time at Caringo, he said, “I was … a contractor. I was never actually a permanent employee. And to be honest, over time, 90 per cent of Caringo’s work force was the same — they were all contractors.They had very few permanent employees.”

He said NexuStorage is a pre-revenue company and, once it starts earning revenue, then it may have permanent employees.

Alternatives

Open source Ceph provides file, block and data access using an underlying object store.

Pavilion Data provides block, file, and object access from its all-flash hardware, claiming it’s the most performant, dense, scalable, and flexible storage platform in the universe.

StorONE provides file, block and object storage on the same drives, supporting all drive types — NVMe, SAS, SATA SSDs and HDDs — in the same server.

NexuStorage will need to have advantages not shared by these products to make headway in the market.

Comment

This is a courageously funded startup with unique software technology that effectively includes data lifecycle management and could provide an effective way of reducing primary storage usage. We’ll watch its progress with interest.

DDN is looking favourably at supporting ruler-format flash drives and a subscription business model, but doesn’t think storage-class memory is needed quite yet.

These points came across when we got the opportunity to send a few questions to Dr James Coomer, DDN’s VP for product management.

James Coomer.

Blocks & Files: Will DDN support the EDSFF ruler format drives?

James Coomer: Yes, we will switch to EDSFF form factor as soon as enough viable media in large capacity points is available, which is the main inhibitor today.

Which particular formats look to be the most appropriate for you?

We are primarily looking at E1.S and E1.L support.

Do you think there are too many EDSFF product formats, compared to the current M.2, AIC, U.2 and 3.5-inch storage drive formats?

Yes too many, and too many competing standards. The market conditions regarding supply are already a bit difficult, so the additional complexity of too many formats doesn’t help.

Will the EXAScaler base system hardware be used in the Tintri enterprise storage product line?

The EXAScaler base system hardware is already being used as the mainline platform for both VMStore and IntelliFlash. The VMStore T7000 series and the IntelliFlash N6000 and H6200 both use the same underlying hardware as the DDN EXAScaler appliances.

Will DDN move to a subscription business model?

Yes. With our upcoming software offerings we are adding subscription. Also we are seeing requests for customers for private cloud managed by DDN at their side or other datacentres, for which we have offerings.

How do you view the storage-class memory (SCM) product scene, with Optane SSDs and DIMMs, and the fast SLC-flash-based drives from Samsung and Kioxia? What is DDN’s view on using SCM technology?

SCM at this point are niche products as the cost is too high, capacity too low and the application-level performance improvements are not high enough for most customers to move in this direction aggressively. As prices will come down they will be used in our efficient hierarchical storage management stack when we see more customer demand, but nothing prevents us from using it today. We just don’t see enough demand yet.

Comment

Excellent answers – short, direct and clear. Thank you Dr James.

Data Processing Units (DPUs) help organisations build denser, faster, more efficient and cost-effective IT infrastructures, with the goal of providing an overall lower total cost of ownership.

This is the thrust of a GigaOm Sonar report, written by analyst Enrico Signoretti, looking at early-stage emerging technologies. DPUs are hardware accelerators, usually installed on commodity x86 servers, to offload specialised compute tasks such as security, storage and networking. They can be implemented as ASICs, FPGAs or proprietary Systems-on-Chip (SOCs) using Arm or specially-developed processors.

The Sonar report evaluates suppliers’ products looking at their performance, programmability, power efficiency, longevity and cost. It also checks key characteristics needed for enterprise adoption: architecture, drivers, APIs, ecosystem, management and support.

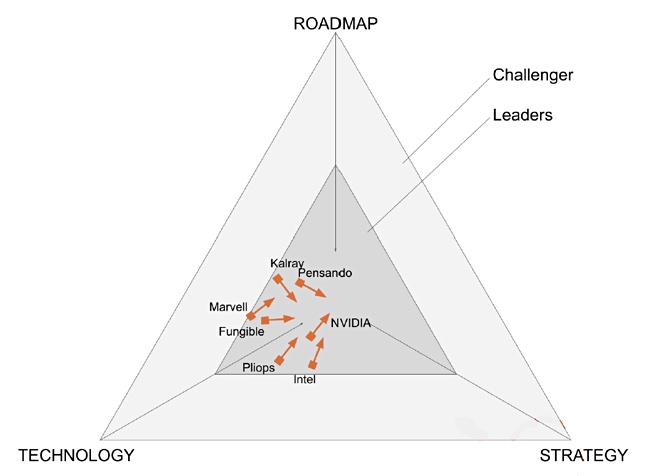

The included suppliers are Fungible, Intel, Kalray, Marvell, Nvidia, Pensando and Pliops. They are placed in a triangular 2D area to represent their relative positions as Challengers or Leaders. The three axes defining the space are technology, strategy and roadmap. The three axes start at the same central point (signifying a higher score) and then move outwards.

Here is the report’s Sonar diagram:

The orange squares are the suppliers’ starting positions, and the arrows show their direction of movement. At this early state of DPU development they are all Leaders – although Marvell is on the Leader/Challenger boundary – and all located in the technology-centric area of the diagram.

Nvidia and Pensando are the overall best-positioned, with Fungible, Intel and Pliops next, followed by Kalray and Marvell.

The report contains descriptive sections for each supplier, describing their product’s characteristics, its strengths and its challenges. It advises: “The DPU is a component of the server. Look to purchase it with the server so the vendor provides warranty and support for both as part of the server maintenance plan.” That seems too be an excellent point for all but hyperscaler customers.

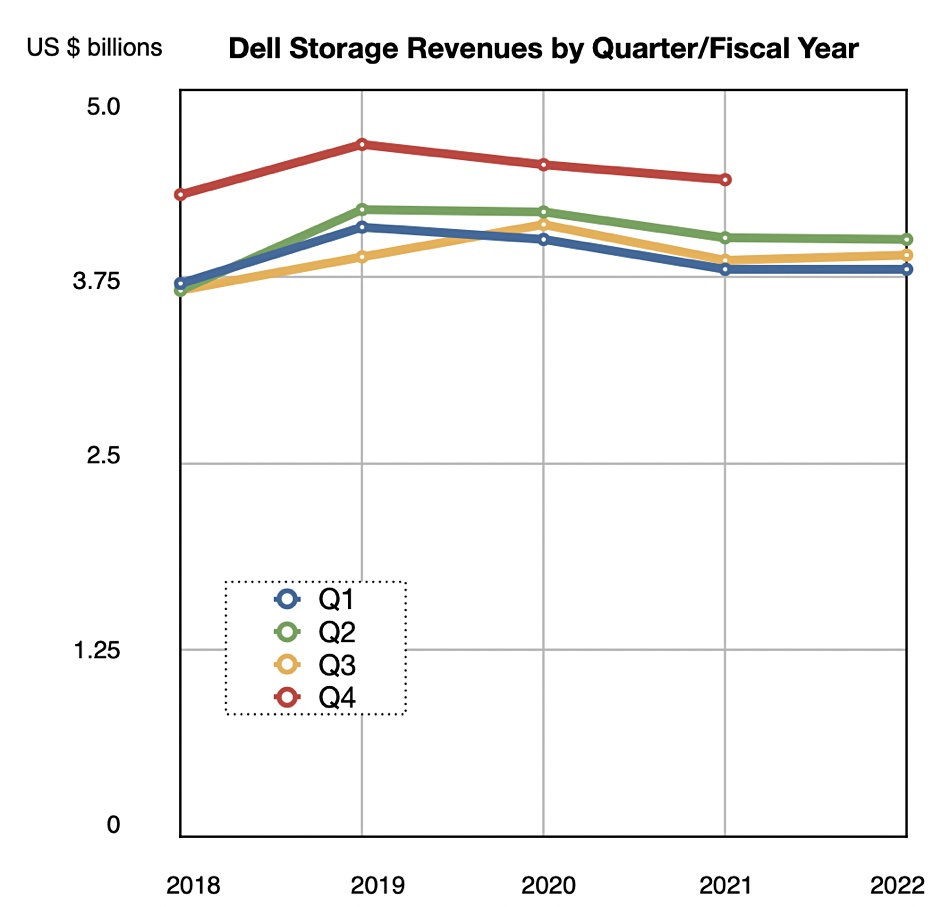

Dell’s quarterly revenues rose 21 per cent year-on-year to a record $28.4 billion, but storage revenues were anaemic with a mere 0.9 per cent rise to $3.89 billion.

This was the best third quarter in Dell Technologies history — helped, Dell said, by robust demand, durable competitive advantages, and strong execution. The company generated record revenue of $28.4 billion in the quarter ended October 29, up 21 per cent, with growth in all business units, customer segments and geographies, and strength across commercial PCs, servers and (much less so) storage. VMware revenue was $3.2 billion — up 10 per cent with general strength across its product portfolio. Dell has now separated itself from VMware.

Chuck Whitten, co-COO Dell Technologies, said in a statement: “We’re three quarters into what will prove to be a historic year for Dell, and we are just beginning to write the next chapter of the Dell Technologies story. We are uniquely positioned in the data era, with durable advantages and market-leading positions. Our strategy is focused on growing our core business and in adjacent multi-billion-dollar markets including multi-cloud, edge, telecom and as-a-Service.”

Jeff Clarke, vice chairman and co-COO Dell Technologies, said in his statement: “Our product, global operations and sales teams did an outstanding job this quarter as we shipped a record number of products and delivered record revenue.”

Yes, but storage rather let the side down. We’ll focus on that while acknowledging that Dell has done an outstanding job elsewhere in its results for the quarter.

Storage

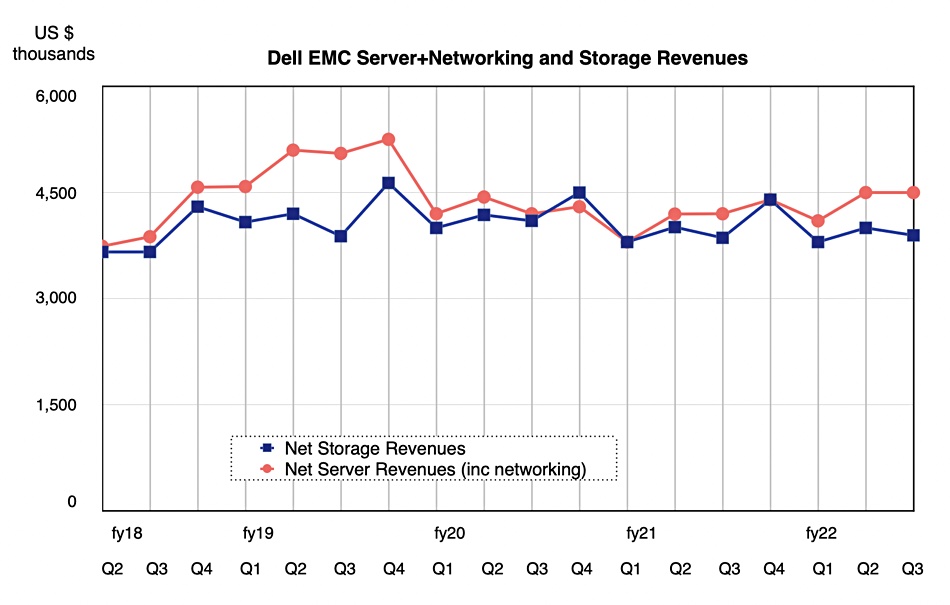

Storage revenues in the Infrastructure Solutions Group (revenues $8.4 billion; up 5 per cent) were almost flat while server-plus-networking revenues rose 9 per cent year-on-year to $4.5 billion.

A chart shows a widening gap between the two product categories over the past three quarters:

The seemingly stubborn resistance Dell’s storage shows to product sales growth is holding ISG revenues back. We should say that Dell is the leading storage product shipper, being number one in external enterprise storage, storage software, all-flash arrays, hyperconverged systems, converged systems, and purpose-built backup appliances. Yet it has barely grown storage revenues over the past three quarters while competitors — such as Pure Storage and NetApp — have grown their revenues.

What is the problem? A results presentation slide said there was “Strong storage demand, orders growth in Hyperconverged Infrastructure up 47 per cent, Data Protection up 26 per cent and Midrange up 18 per cent.” There must have been significant weakness elsewhere in the product range to have overall storage growth be just 0.9 per cent

This suggests disappointing high-end array sales could be a factor and possibly also low or no growth in Dell’s PowerScale file and ECS object storage products. There could be increased competition from suppliers such as Infinidat, Pure Storage, VAST Data, Qumulo and others to account for this.

Earnings call

We looked for any clues in Dell’s earnings call. Co-COO Jeff Clarke declared: “We are pleased with our storage performance in Q3, where we saw storage return to growth.”

He declared: “Momentum in our mid-range storage business continues to be led by PowerStore, where 23 per cent of PowerStore customers renewed to Dell storage and 28 per cent were repeat buyers. PowerStore is the fastest-ramping storage product in our history.”

That’s all very well but storage must have been a disappointment to Clarke with its lacklustre growth.

Answering a question, CFO Tom Sweet said: “Storage demand tends to be more back-end loaded in the quarter, and we clearly saw that again this quarter, perhaps a bit more than in prior quarters. And as a result of that, we were not able to convert that backlog to revenue … and we also deferred a fair amount of revenue to the balance sheet, just given the service attach rate as well as the software content within the storage.”

Whitten jumped in to strengthen Dell’s answer here: “We’re encouraged by storage orders growth because in the most strategic category, software defined storage, we grew 47 per cent, mid-range orders grew 18 per cent, which is now the fourth consecutive quarter our mid-range business has grown. … Data protection grew, unstructured data grew and our entry-level orders grew as well in the storage business, so … we remain encouraged by the orders growth.”

Will this backlog translate into growth next quarter? Possibly not, as Sweet said: “The reality is, as we highlighted in the talk track that we’re continuing to face supply chain challenges. And so how much of server demand gets converted or backlog gets converted into shippable revenue is something that the teams are working every day.”

He also said though: “that Q4 tends to be a higher storage quarter for us.”

It seems fair to assume that Dell is facing headwinds in the high-end array, filer and, possibly, object storage space. There must have been quite severe revenue declines in its storage portfolio outside the highlighted growth areas, such as the mid-range. This suggests that there are product weaknesses needing to be fixed and that could be a multi-quarter exercise.

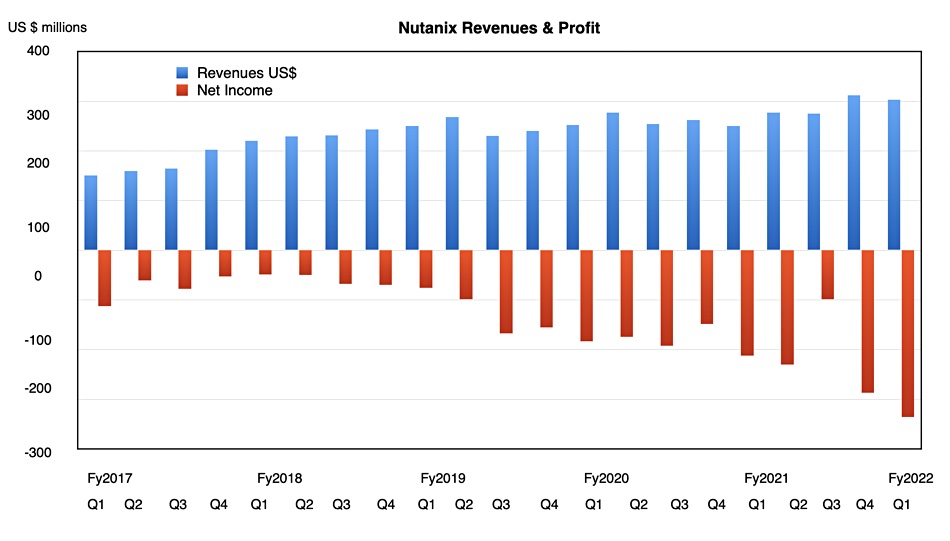

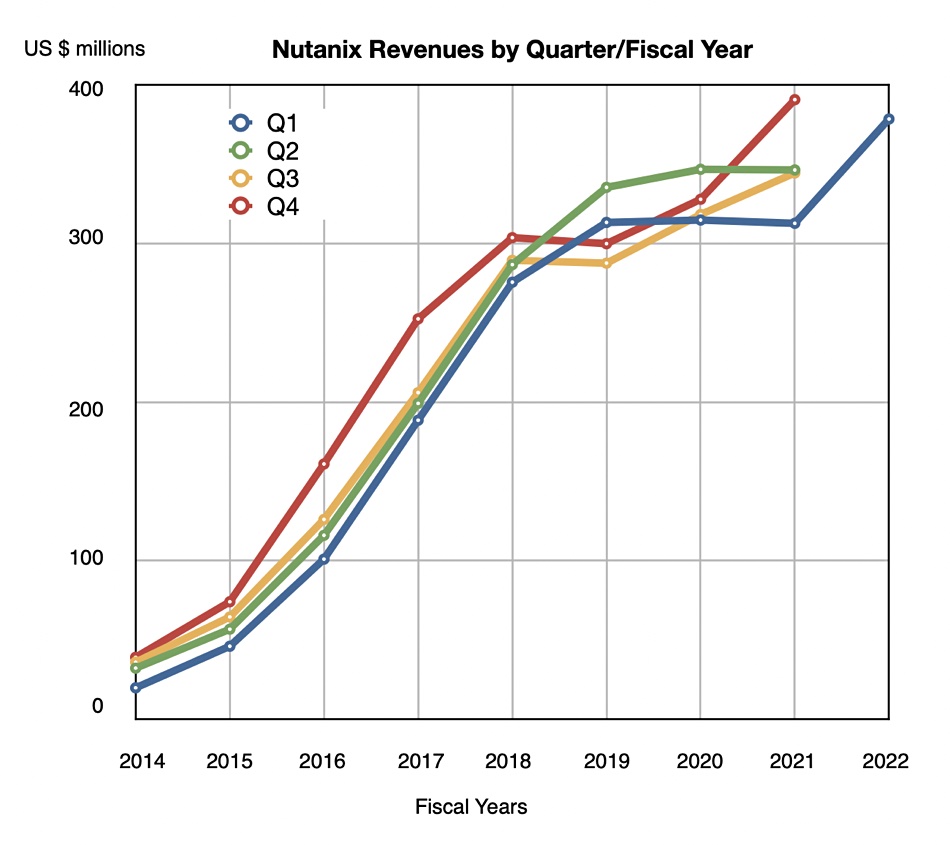

Nutanix reached a negative landmark, with losses exceeding revenues in its latest quarter, but financial analysts are happy with its progress.

Revenues were $378.52 million in its first fiscal 2022 quarter, which ended October 31, up 21 per cent annually, for a loss of $419.8 million. For every dollar it earned Nutanix spent $1.11 — it bought its growth. The year-ago quarter’s loss was $265 million. In the previous quarter it dropped 92 cents in costs for every dollar of revenue. Things have got worse.

President and CEO Rajiv Ramaswami’s results statement read: “Our first quarter was a good start to our fiscal year, demonstrating strong year-over-year top and bottom line improvement.” The “bottom line” term certainly did not refer to GAAP net income.

CFO Duston Williams said: “We achieved record ACV billings, which grew 33 per cent year-over-year, and saw 21 per cent year-over-year revenue growth, our highest growth in over three years.”

Financial summary

Free cash flow — improved to -$1.9M from -$16.3M a year ago;

Gross margin — 78.5 per cent compared to 78.3 per cent a year ago;

Annual Contract Value (ACV) — $183.3M vs last year’s $137.8M, up 33 per cent;

Annual Recurring Revenue (ARR) — $952.6M vs $569.5M a year ago;

Cash and cash equivalents at end of period — $350.99M compared to $504.5M last year.

The quarter was the third in a row showing annual growth and one with a steep rise:

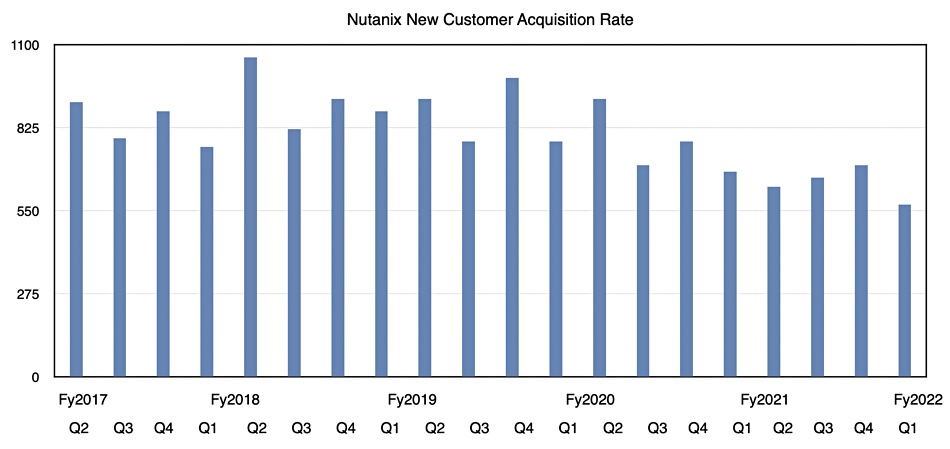

Nutanix grew its customer count by 570 in the quarter to a total of 20,700 but the increase was the lowest for five years or more. The customer acquisition rate trend is downwards. We might say Nutanix is spending more, as shown by deepening losses, to gain fewer new customers.

But customer spend increased and analysts were not concerned, as we shall see.

There was a minimal impact of Nutanix’s business from the COVID resurgence, as customer businesses have learnt how to do remote working. There was little to no supply chain impact as Nutanix has multiple hardware partners.

Nutanix saw more customers buying more products — 42 per cent of customer deals involved at least one so-called emerging product, which includes all add-ons beyond the basic HCI offering. This was up slightly, 7 points Nutanix said, year-on-year. A basis point is equal to 1/100th of one per cent, which is why we said it was up slightly.

Analyst views

Wells Fargo’s Aaron Rakers told subscribers: “[Nutanix] delivered positive F1Q22 results (and forward guide) driven by a seasonally strong federal business, significant upselling, and continued execution on subscription renewals.” He said Nutanix “provided investors with increased confidence in the company’s path to profitability,” and “Nutanix expects significant growth in emerging products and new ACV bookings in F2Q22.”

Rakers commented on the customer acquisition rate: “While new logo additions decelerated, Nutanix’s ASP per new logo was up year over year and quarter over quarter as it focuses on quality/efficiency of new logos. [Nutanix] now has 1,580 customers that have purchased >$1 million, up 68 quarter over quarter.”

Williams said in the earnings call: “We are generating more new logo ACV bookings with less new logos,” which explain’s Rakers’ view.

William Blair’s Jason Ader said: “Nutanix reported another solid beat-and-raise in its fiscal first-quarter print as the company benefited from improving hybrid cloud infrastructure demand, returns on its solution selling investments (including higher win rates, healthy renewals, and a strong attach rate for add-on products), and enhanced partner leverage.”

Ader also sees a “significant renewal opportunity ahead”. He pointed out that: “Management continues to view its rapidly approaching renewal opportunity as the key to unlocking operating leverage and achieving its target of free cash flow break-even in the next 12–18 months (as well as operating profit in calendar 2023).”

This means analysts were not concerned over the big loss, with Ader saying: “The company gained operating leverage from the higher revenue and spent less than expected.” But he did point out: “Risks to the Nutanix story include competition from Dell/VMware and cloud titans, a high cash burn and deep level of operating losses.”

Guidance

The guidance for the next quarter is for revenues between $400 million and $410 million — an annual increase of 16.9 per cent at the $405 million mid-point. Growth is slowing. Revenue guidance for the whole fiscal 2022 year is $1.615 to $1.630 billion — a 16.7 per cent increase on FY2021 at the mid-point.

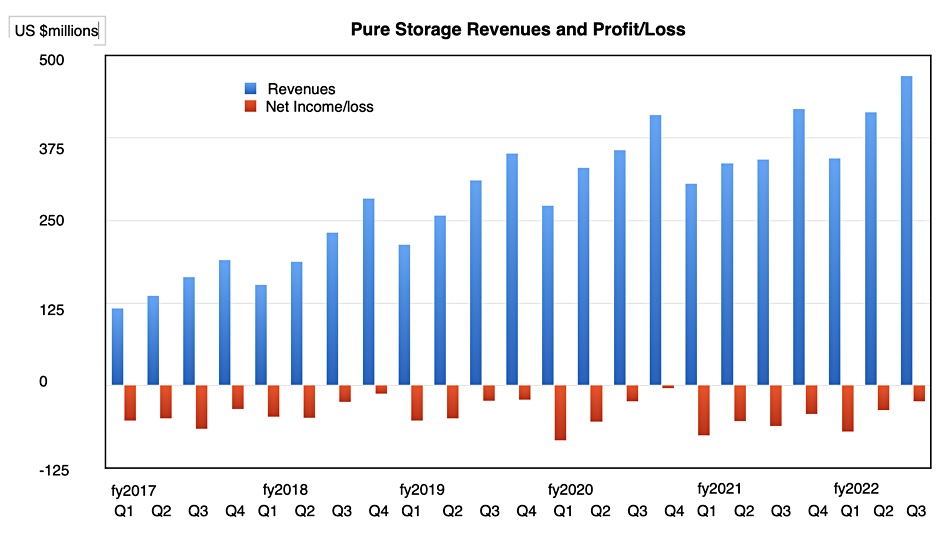

Pure has grown third quarter revenues a whopping 37 per cent year-on-year, surging back after last year’s third quarter 4 per cent revenue fall. That was its first negative growth quarter since we started reporting its results more than five years ago.

Revenues in the quarter ended October 31, 2021, were $562.7 million. They were $410.6 million a year ago, with a loss of $28.7 million — less than half the year-ago $74 million loss. But look at the quarterly trends so far this fiscal year. The chart below shows a declining loss trend throughout this fiscal year and if the fourth quarter comes in at the predicted $630 million then Pure could turn a profit — a GAAP profit — its first ever. That would be a landmark event in its history.

See the profit/loss trend in FY2022 at the right end of the chart.

Chairman and CEO Charlie Giancarlo said in his results statement: “With Q3 revenue up 37 per cent year-over-year and with increasing profitability, it’s clear that Pure continues to set the pace for the industry.”

CFO Kevan Krysler said: “Our strong Q3 performance was fueled by increased customer demand and execution across the entire business. We are in a great innovation cycle with our portfolio.”

Giancarlo’s prepared remarks reflected this, as he predicted: “Our next announcement, on December 8th, will … extend the breadth of our FlashArray platform.”

Financial summary:

Subscription services revenue — up 38 per cent year-on-year;

Subscription Annual Recurring Revenue (ARR) — $788.3M, up 30 per cent year-over-year;

Gross margin — 66.6 per cent;

Operating cash flow — $127.0M;

Free cash flow — $101.3M;

Total cash and investments — $1.4B.

Pure gained 345 new customers in the quarter — 12 per cent year-over-year growth — taking its total to, we calculate, just shy of 10,000 (actually 9,992 give or take).

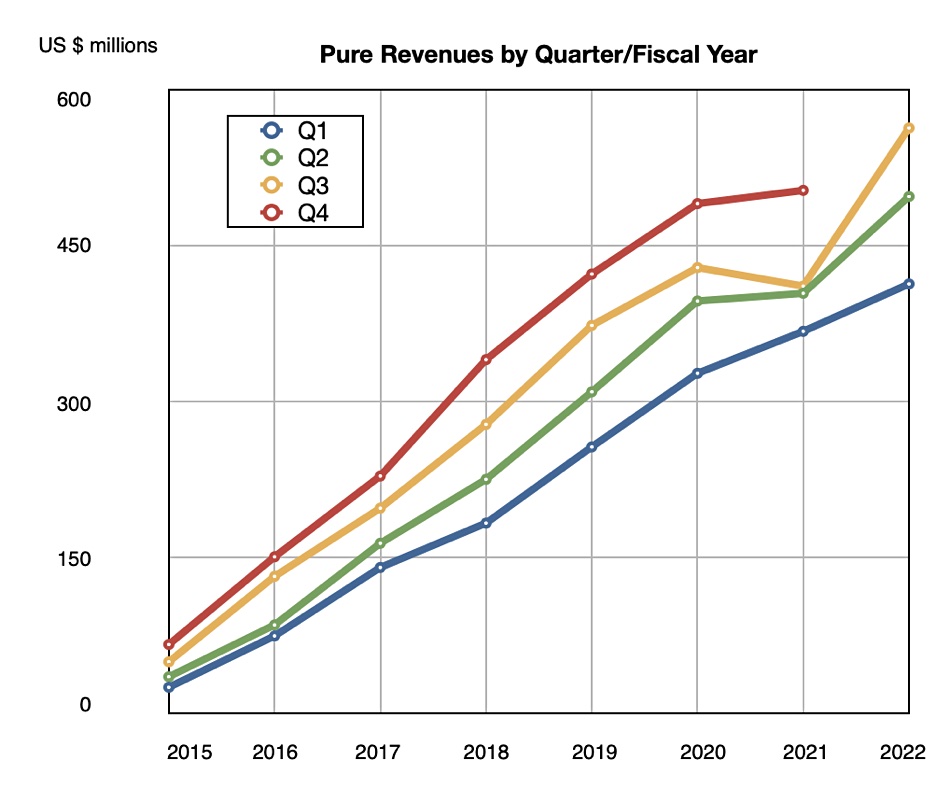

The Q3 revenue bounce back is seen clearly in a chart of revenues by quarter by fiscal year — see the yellow line’s dip and steep ascent.

The trends are good and Pure has uplifted its full year forecast to $2.1 billion — a 25 per cent increase on FY2021. This, with its Q4 $630 million contribution, rebuts any ideas that the Pure would be hit hard by the departure of sales chief Dominic Delfino earlier this month. He was replaced by Dan FitzSimons, who got a “special shout-out” from Giancarlo.

Earnings call

Giancarlo said in the earnings call that Pure had: “double-digit quarter-over-quarter growth across all product lines and across both US and the international markets” and “Pure continues to take share.”

He made a remark that strengthens our belief that Pure could make a profit in the next quarter: “We are also pleased with our strong profitability trend continuing through this fiscal year.” Krysler said he saw no sign of demand relaxing in his initial look at the next fiscal year.

Giancarlo acknowledged supply chain problems but said they had been largely overcome. “This past quarter, global semiconductor availability was more challenging than last quarter, and we expect this environment to continue into next year. However, our operations team and the strong partnerships we’ve built with our suppliers have continued to work well, minimising impacts to our customers and our business.”

Pure will publish its first environmental, social and governance report early next calendar year, with Giancarlo saying: “Pure’s products use dramatically less energy and create far less waste than competitive offerings.”

Hyperscaler FlashArray//C sale

Krysler dropped this gem about a product sale: “Our sales growth this quarter also includes sales of FlashArray//C to one of the top 10 hyperscalers.” A $10 million-plus FlashArray//C sale to a hyperscaler was predicted back in August. Without that sale the quarter’s growth “would more likely be in the high 20s,” rather than the reported 37 per cent. This particular sale could be repeatable with Krysler saying: “No reason for us not to believe that it’s repeatable and conversations continue.”

Giancarlo said that: “It’s also worth noting that the overall footprint savings was a key part of winning the initial deal,” referring to a disk-based alternative.

He talked about a disk-to-flash crossover, saying: “We believe very strongly that as flash continues to decline relatively to the declines in magnetic disk, that there’s inevitably going to be a crossover point where every player everywhere including the hyperscalers will start switching from disk to flash. And it’s just a matter of time and their particular use case or instance before that happens. … before flash is used in a more … mainstream way in the hyperscale environment.”

All the action is centred down on the bottom-left in Gartner’s latest hyperconverged infrastructure (HCI) software magic quadrant (MQ).

This annual MQ rates HCI suppliers on low-to-high “completeness of vision“ and “ability to execute” axes, defining a rectangular space divided into four squares: Niche Players with low vision and executive ability, Visionaries with more vision but low executive ability, Challengers with higher executive ability but low vision, and Leaders with high vision and high ability to execute. It’s a quick guide to supplier choices for Gartner clients, backed up by a separate and more thorough critical capabilities report.

This year’s HCI MQ has no change in the Challengers and Leaders quadrants, the former being empty and the latter the domain of just two players: Nutanix and VMware, and their respective positions are effectively unchanged. Nutanix is maybe closer to the ideal balanced execution ability/vision line.

Down in the bottom left, we wave goodbye to DataCore, which has been ejected this year. We see Quantum inheriting the acquired Pivot3 slot and moving to the left and downwards. StorMagic, with its vSAN product, moves into the Visionaries quadrant, which pleases it mightily. An announcement said: “This is the fourth consecutive year that StorMagic has been included in the report, and we are incredibly proud to be recognised, for the first time ever, as a ‘Visionary.’”

Andrew File System developer AuriStor updated attendees at an IT Press Tour briefing about its work on the file system with an HPC and large enterprise customer base dating back 16 or more years.

AuriStorFS (a modern, licensed version of AFS) is a networked file system providing local access to files in a global namespace that has claimed higher performance, security and data integrity than public cloud-based file-sharing offerings such as Nasuni and Panzura.

AuriStor is a small and distributed organisation dedicated to expanding the popularity and cross-platform use of AuriStorFS.

AFS background

The Andrew File System (AFS) began life as the Andrew Project by Carnegie Mellon University, which was founded in a merger of the Carnegie Institute of Technology and the Mellon Institute of Industrial Research in 1900. The founders of these two institutes were Andrew Carnegie (steel industry magnate) and Andrew Mellon (banking magnate) — hence the eponymous Andrew Project.

AFS is a scalable client-server distributed file system, like NFS and SMB, with a global namespace, location independence, client-side caching, callback notification to clients of file system content changes, and replicated access to read-only data. It looks like a local file system on an AFS client. An AFS cell entity is one or more AFS servers and their clients forming an administrative domain.

OpenAFS is an open source implementation of AFS based on code made available by Pittsburgh-based, IBM-owned Transarc in 2000. Transarc was started up in 1989 by several Andrew Project members and IBM was an initial investor.

AuriStor

Jeffrey Altman.

AuriStor was founded in 2007 as Your File System, Inc., by CEO Jeffrey Altman. It is a small — you might even say minute — company, with just five employees listed on LinkedIn. However it says it has a distributed team with members in its offices in New York City, Cambridge MA, Edinburgh, Scotland, and Nova Scotia, Canada.

A briefing presentation slide showed just eight contributing developers since January 2019.

AuriStor’s aim was to accelerate AFS development by selling a licensed version of AFS, and thus fund its own engineering and support effort. Its AuriStorFS is claimed to be a better cross-platform offering than Microsoft’s Windows DFS, more reliable than Gluster, as performant as GPFS, and more cost effective than Panasas for general storage needs. AuriStor wants to sell its AuriStoFS to large, medium and small enterprises, and even individuals with smartphone client software.

AuriStorFS is backwards compatible with AFS and OpenAFS. It has been certified for Red Hat Enterprise Linux 8.4, making it the only AFS-family software certified for use on any Enterprise Linux distribution. It is validated for Debian, Ubuntu, CentOS, and Oracle and AWS public cloud use. Client support includes Linux, macOS and Windows.

The AuriStorFS source code is available to licensed organisations wanting to participate in its development as part of a private community.

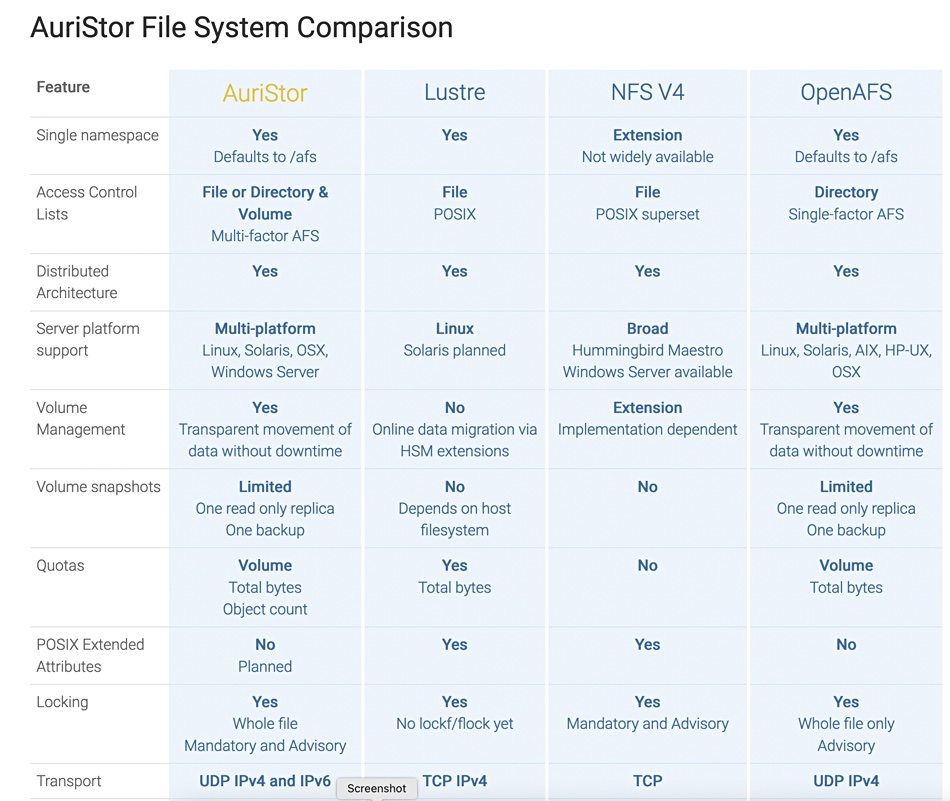

Competition

Here is a competitive matrix from the AuriStor website:

It appears to be somewhat dated. It does not include, for example, Panasas, Spectrum Scale, DAOS or WekaIO.

Scalability and performance

An AuriStor cell can store up to 2259 file streams of up to 16 exabytes — the maximum allowable distributed database size. OpenAFS tops out at 2GB — a tiny fraction of that.

The number of Volume IDs per cell is 264 — much more than the 231 limit of OpenAFS. There can be 290 objects (directories or files) per volume compared to OpenAFS’s 226.

Auristor’s timestamp granularity is 100ns which compares to OpenAFS’s 1 second.

There’s no need to go on. AuriStorFS is ridiculously more scalable than OpenAFS.

AuriStor says AuriStorFS is faster than OpenAFS and performance-competitive with Lustre, GPFS (Spectrum Scale), Panasas and NFS v4.

Customers

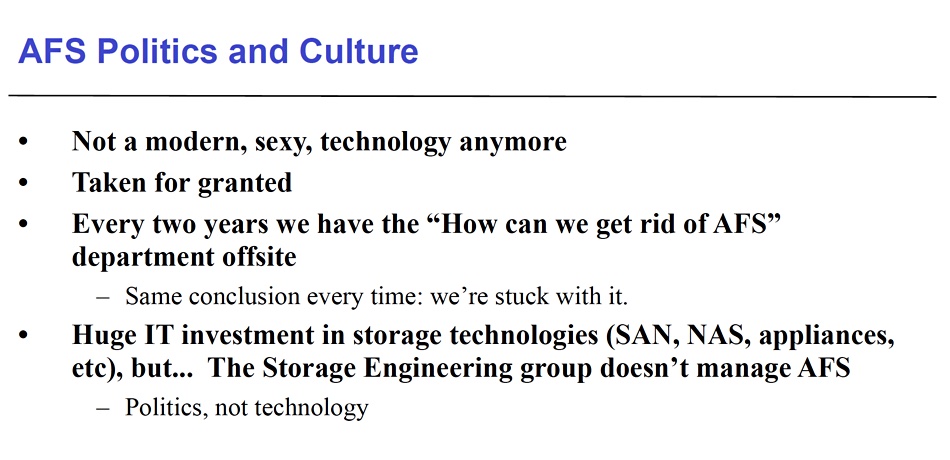

AFS, through IBM’s support, gained HPC and large enterprise users, such as Morgan Stanley, which in 2004 had more than 25,000 hosts in 50+ sites on six continents. Morgan Stanley said AFS could provide WAN file sharing better than NFS as it had a better client:server ratio of hundreds to one compared to NFS’s then 25:1.

At that time AFS was seen as dated, but Morgan Stanley’s investment in it made it impossible for the firm to migrate away.

Morgan Stanley view of AFS in 2004.

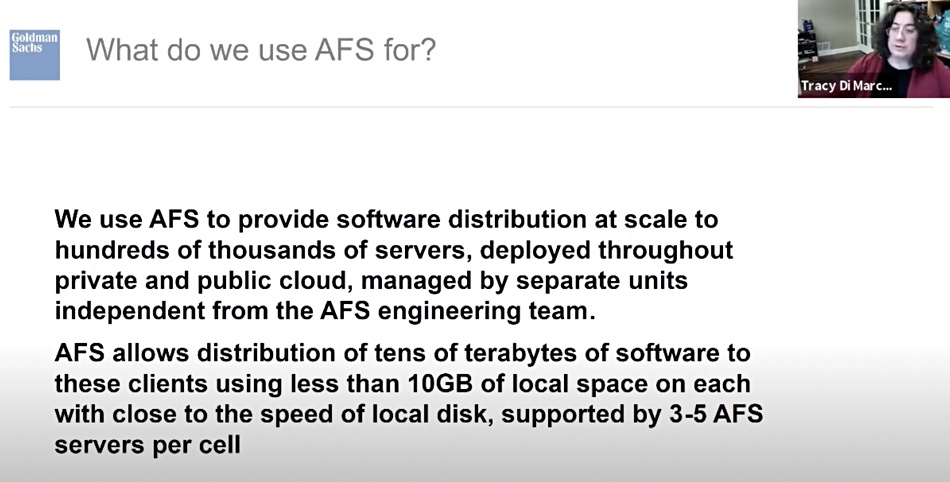

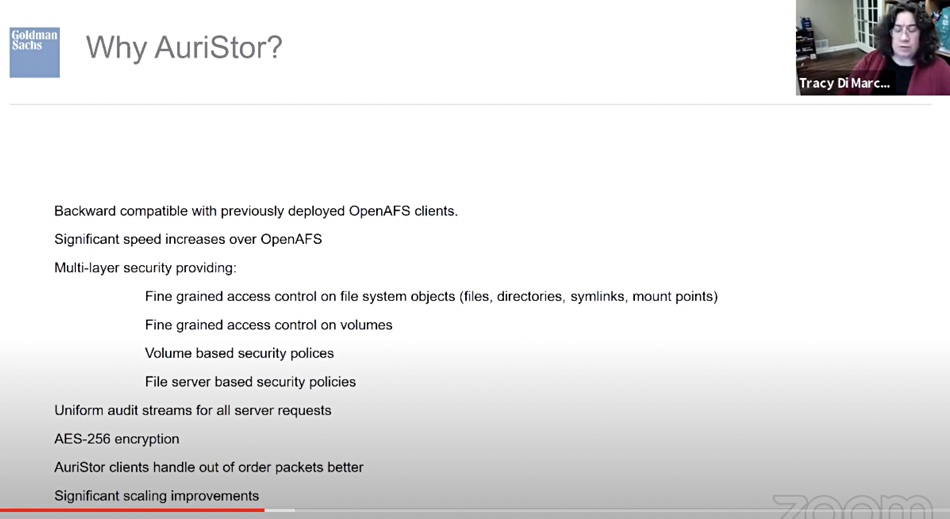

Goldman Sachs is another AFS user, and replaced its OpenAFS client with the AuriStorFS client in 2017, deploying it to 25,000 hosts — a number which has since grown. Its experience is discussed in a 2020 YouTube video by VP Core Engineering Tracy Di Marco.

Slide from Goldman Sachs’ VP Tracy Di Marco’s presentation.

Di Marco said AuriStorFS “allows us to provide hundreds of thousands of hosts that perform business functions to the firm, at close to local disk speed, without repeated, possibly expensive, unnecessary network usage, and with a standard small disk allocation, rather than more expensive larger disks.”

Slide from Goldman Sachs’s VP Tracy Di Marco’s presentation.

Other AuriStor customers include CERN, Intel, the IRS, Qualcomm, United and KLM airlines. We couldn’t find any HPC customers and think that the number of such is low. WekaIO, for example, has never encountered AFS, OpenAFS or AuriStor in the HPC market.

Comment

This is a niche business. AuriStor is a small business exclusively focussed on its own products and supporting a relatively small number of extremely large customers. It is funded by license sales and not by venture capitalists, making it markedly different from competing file system suppliers such as WekaIO.

The main competition facing AuriStor in our view comes from the public clouds — AWS, Azure and Google — and applications such as CTERA, Egnyte, Nasuni and Panzura. Hammerspace, with its global filesystem namespace, is another competitor.

A main focus of AuriStor marketing is to encourage its adoption by OpenAFS users. A secondary focus, in our view, is to prevent defection by its user base to the public cloud.

If it succeeds in moving down market from enterprise users with 20,000-plus servers then it will increasingly come into competition with CTERA, Egnyte, Nasuni and Panzura and may suffer from appearing more complex to install and manage than these suppliers’ products. At the same time it has more bells, whistles, levers and hooks for admin staff to use, secure and optimise it.

Pricing

The starting price for an AuriStor installation is $21,000/year for a perpetual use license with four database service and four file service instances. Additional file or database service instances within a cell start at $2,500 each and decrease to $1,000 each based upon quantity. Single server cells are licensed at a base price of $6,500.

Fact Sheet

Get a 24-page downloadable AuriStor fact sheet as a PDF from here.

See Tracy Di Marco’s “Leveraging AFS Storage Systems to Ease Global Software Deployment” presentation here and the slides here.

CDS, which supplies datacentre component monitoring services, announced its Raytrix MVS Insight offering with monitoring of a broad array of server, network, and storage environments and integration with leading ITSM providers. Raytrix MVS Insight supports thousands of devices and systems from all the major OEMs including HPE, Dell EMC, Hitachi, IBM, Fujitsu, Juniper, CISCO and Brocade. The product provides comprehensive monitoring at enterprise scale, from single devices to thousands of systems. It features a holistic overview of monitored environments across systems and locations, a broad array of notification methods from SNMP to Slack, alert correlation and predictive utilisation normalisation, and flexible alert filtering and scheduling to avoid network congestion.

…

Startup HighTouch, which is developing software to enable companies to get their data out of data warehouses and into an application — a reverse to the normal ETL process — has raised $40 million in a B-round of funding. HighTouch software copies data from the data warehouse tables into a SaaS application’s tables, such as Salesforce. Data analysis is done inside the SaaS app and not the data warehouse. HighTouch integrates with BigQuery, Snowflake, and Databricks, and enterprise applications such as Anaplan, HubSpot, Mixpanel, Salesforce, Stripe, and Jira. Policies can be set up to define sync frequencies to keep the destination app up to date with data changes in the source warehouses.

…

SaaS data protector HYCU introduced a Global PACE (Partners Accelerating Cloud Environments) Program. It eliminates tiers of engagement making it easier for partners to sell HYCU services. There are separate tracks for Managed Service Providers (MSPs), Cloud Service Providers (CSPs) and Managed Security Service Providers (MSSPs) plus enhancements for reseller and distributor partners. The program features a zero conflict promise, margin assurance, minimum advertised price, and seed and premier tiers.

…

JetStreamSoftware has announced general availability of JetStream disaster recovery for Azure VMware Solution (AVS), offered through the Microsoft Azure Marketplace and sold by Microsoft sales teams. Microsoft and Jetstream say it’s the first cloud-native, disaster recovery as a service (DRaaS) for VMware-based clouds and on-premises VMware environments. An integration with NetApp enables Azure NetApp Files (ANF) to support storage expansion of larger data sets independent of compute, enabling a much faster recovery time and near-zero RTO — at a lower cost. The offering combines Azure Blob Storage, JetStream DR (VMware-certified), Azure VMware Solution, and ANF storage expansion. Microsoft and JetStream say it will radically transform the economics of disaster recovery for enterprises.

…

Andy Langsam.

Cloud storage provider Wasabi has opened a London, UK, region to expand the availability and speed of services throughout the UK. It is located in an Equinix datacentre and is Wasabi’s second European region. The first opened in Amsterdam in 2019. The London centre has high-speed network access from multiple carriers, making it easy for UK customers to connect, plus power and space expansion capabilities. Wasabi has plans to open additional storage regions in 2022.

…

Veeam appointed Andy Langsam as GM Kasten Kubernetes Business Unit and SVP of Public Cloud for Veeam in August. He was Veeam’s SVP Public Cloud & Enterprise. He is an ex-SVP Sales at SolarWinds and COO of N2SW, acquired by Veeam in January 2018. As GM of the Kasten business unit he took over from prior GM, Niraj Tolia, the CEO and co-founder of Kasten, which was acquired by Veeam in September 2020. Tolia is now SVP for strategy at the Kasten Kubernetes BU.

Datto management believes it is currently the largest pure-play backup software supplier to the MSP market and growing faster than competitors ConnectWise, Kaseya, and N-able. (Thanks to Jason Ader of William Blair.) It think it is well positioned in the long term to capitalise on secular trends toward outsourced IT via the roughly $130 billion managed service provider (MSP) channel. Datto counts more than 18,200 MSP customers (out of an estimated 125,000 MSP providers worldwide), which creates abundant opportunity for deeper penetration. Management is looking to substantially expand its security capabilities over time to fulfil its stated mission of securing all digital assets for its MSP/SMB customers.

…

Quest Software announced GA of SharePlex v0.1.2 which can replicate Oracle databases in real time to MySQL and PostgreSQL. This can be useful when creating mobile or API-based applications, supported by PostgreSQL or MySQL databases, that require data from a legacy Oracle system. SharePlex for PostgreSQL and MySQL supports AWS (RDS and Aurora) and Azure (Azure Database for PostgreSQL and Azure Database for MySQL). It also supports replication to Oracle data warehouses, SQL Server data warehouses, PostgreSQL data warehouses, Kafka, which can then feed other systems, and Event Hubs, which can then feed other systems in the Azure ecosystem.

…

A new release of Raidix’s Era software RAID, version 3.4, provides improved automatic error correcting in case of write hole (inconsistent checksum or data), file drive error monitoring, and support for multi-path NVMe drives.

…

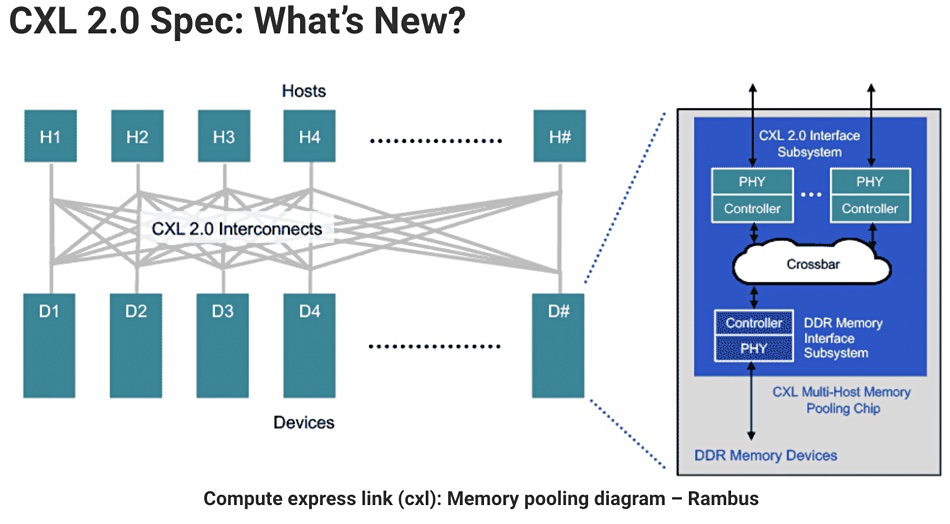

Semiconductor technology developer Rambus has posted a blog about CXL v2.0. It states:”Server architecture — which has remained largely unaltered for decades — is now taking a revolutionary step forward to address the yottabytes of data generated by AI/ML applications. Specifically, the datacentre is shifting from a model where each server has dedicated processing and memory — as well as networking devices and accelerators — to a disaggregated ‘pooling’ paradigm that intelligently matches resources and workloads.” CXL 2.0 supports memory pooling using persistent memory and internal-to-the-host DRAM.

“By moving to a CXL 2.0 direct-connect architecture, datacentres can achieve the performance benefits of main memory expansion — and the efficiency and total cost of ownership (TCO) benefits of pooled memory.”

…

SK hynix’s desire to upgrade its DRAM manufacturing operation in Wuxi, China, by using Extreme Ultraviolet (EUV) lithography equipment to draw finer lines on wafers and thus make denser chips, has had doubt raised over it, according to Reuters. The export of EUV gear to China could fall foul of US State Department rules preventing high tech exports to China.

…

The Taipei Times reports that China’s Alibaba group will lead a consortium offering ¥50 billion ($7.8 billion) to take over the bankrupt Tsinghua Unigroup which makes semiconductor products. There are several Chinese state-backed bids to take over Tsinghua Unigroup, which is seen as important to China’s desire to be self-sufficient in making semiconductor products. It owns, for example, Yangtze Memory Technology Corp.

…

Yangtze Memory Technology Corp. 128-layer 3D NAND Chips.

DigiTimesreported Chinese NAND fabber YMTC has improved the yield rate for its 128-layer 3D NAND. Output could reach 100,000 wafers per month in the first half of 2022. That could/would mean lower NAND chip sales in China for Kioxia, Micron, Samsung, SK hynix and Western Digital.