Data analytics startup Dremio has raised $135m in a D series, taking total funding to $250m, and achieving unicorn status ($1bn+ valuation). Competitor unicorn startup Starburst has pulled in $100m and Firebolt, another competitor, has taken in $37m.

The funding context is that cloud-based data warehouser Snowflake had a hugely successful IPO in September, 2020 and has a market cap of $80bn, at time of writing.

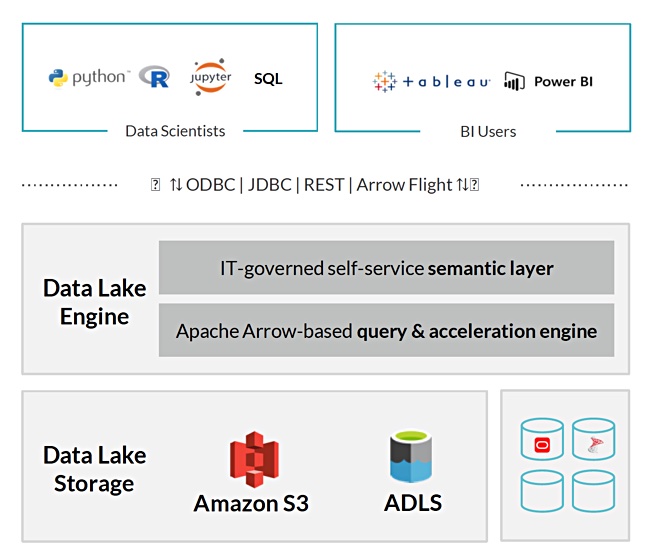

The shared dream here is to run fast data analytics on data from a variety of data sources. Dremio and Starburst say they do it simultaneously, without extracting the data you need and transforming it so it can be loaded into a single destination data warehouse. Instead you use software to combine different data sources into a single virtual data warehouse and analyse the data in that and in real time.

Firebolt says it performs extract, transform and load (ETL) much faster and more simply, and then runs faster analytics.

Dremio

California-based Dremio’s software technology enables data analytics to access source data lakes, thus avoiding existing extract, transform and load (ETL) procedures to build a data warehouse. Its cloud data lake engine software runs in the AWS and Azure public clouds, or on-premises via Kubernetes or Docker, and uses executor nodes with NVMe SSDs to cache data.

Dremio has a Hub software entity that provides connectors for Snowflake, Salesforce, Vertica, AWS Redshift, Oracle, various SQL databases, and others to integrate existing databases and data warehouses.

Its performance claims seem almost outlandish; 3,000 times faster ad hoc queries, 1,700 times faster BI (Business Intelligence) queries and 90 per cent less compute needed than other SQL engines.

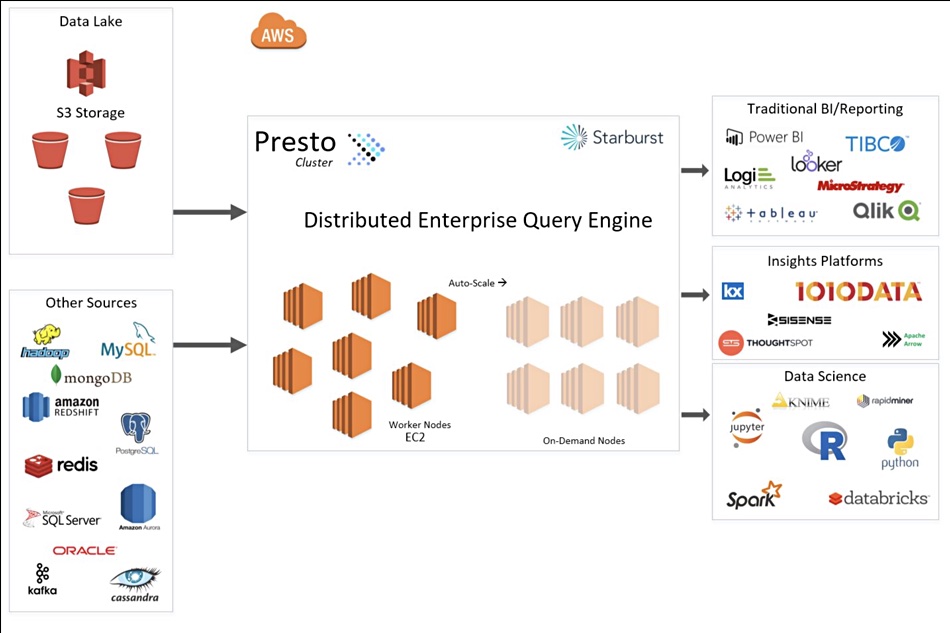

Starburst

Total funding for Boston-based Starburst stands at $164m, including $100m raised recently at a $1.2bn valuation.

The technology is based on Facebook’s open source Presto distributed query project. It applies SQL queries across disparate data lakes and warehouses, such as Teradata, Oracle, Snowflake and others.

Starburst’s software runs in AWS, Azure, and Google Cloud or on-premises via Kubernetes.

Firebolt

Israel-based Firebolt, the newest of the three startups here, says it delivers the ultimate cloud data warehouse running analytics with extreme speed and elasticity. The company set up in 2019 and bagged $37m in A-round funding in December 2020.

The software has native support for semi-structured data and querying with SQL. Firebolt claims “semi-structured data can be analysed quickly and easily, without the need for complicated ETL processes that flatten and blow up data set size and costs.”

In other words, it runs ETL processes to get data into its more scalable data warehouse, and then queries the data faster.

Firebolt says its serverless architecture separates compute from its S3 data lake storage and provides an order-of-magnitude leap in performance. Customers can analyse much more data at higher granularity with lightning fast queries.

More reading

Download a Dremio Architecture Guide to find out more about its software. Download a Starburst Presto guide to read about its technology, and inspect a Firebolt document comparing its technology to Snowflake’s.

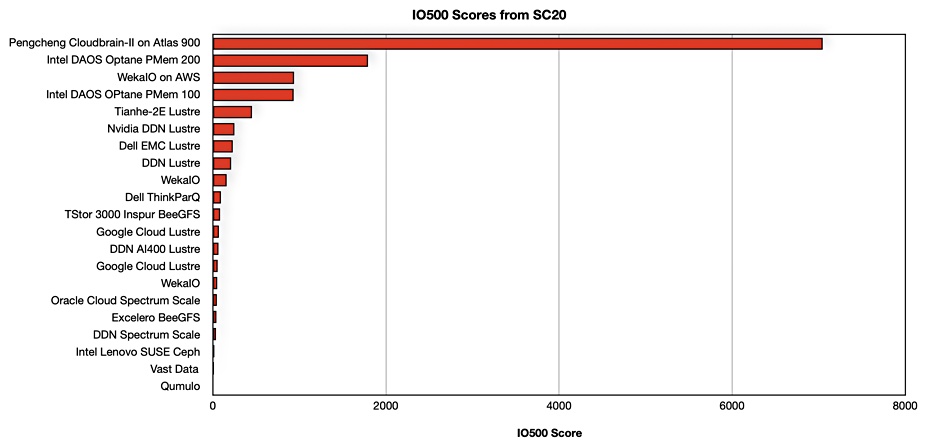

An Intel DAOS file system has leapfrogged WekaIO on the IO500 list, an annual league table of the fastest HPC file systems. This reverses Weka’s win over DAOS in 2019. However, a Huawei-based system is almost four times faster again.

This AI cluster is seriously big supercomputing iron, making Intel’s DAOS test rig of 30 servers and 52 clients look like a Raspberry PI in comparison. Having it on the same list as the DAOS and Weka systems makes the IO500 look unbalanced, like comparing a racing yacht with kayaks.

You’re playing with the big boys now

The Pengcheng Cloudbrain-II, jointly developed by Huawei Technologies and Pengcheng Laboratory in China, radically out-performs every other system, with its 255 client nodes scoring 7,043.99 on the IO500 test.

The hardware is a Huawei Atlas 900 AI cluster that uses Huawei’s Kunpeng and Ascend processors. Kunpeng 920 CPUs are 64-core, 64-bit ARM processors, designed by Huawei and built on a 7nm process. According to the partners, this is the world’s largest artificial intelligence computing platform.

Updated IO500 list.

Pencheng Lab aims to eventually reach exascale computing, with four Atlas 900 AI clusters deployed, delivering 1,000 petaflops.

This AI cluster is seriously big supercomputing iron, making Intel’s DAOS test rig of 30 servers and 52 clients look like a Raspberry PI in comparison. Having it on the same list as the DAOS and Weka systems makes the IO500 look unbalanced, like comparing a racing yacht with kayaks.

Huawei Atlas 900 AI Cluster

Intel vs WekaIO

DAOS – Distributed Application Object Storage – is Intel’s open-source and Optane-using parallel file system for high performance file system operations. All-flash servers are being used. DAOS puts metadata into Optane Persistent Memory and also stages small IO operations there, before writing full blocks to the SSDs.

Accessing filesystem metadata in the Optane memory is faster than accessing it in NVMe SSDs.

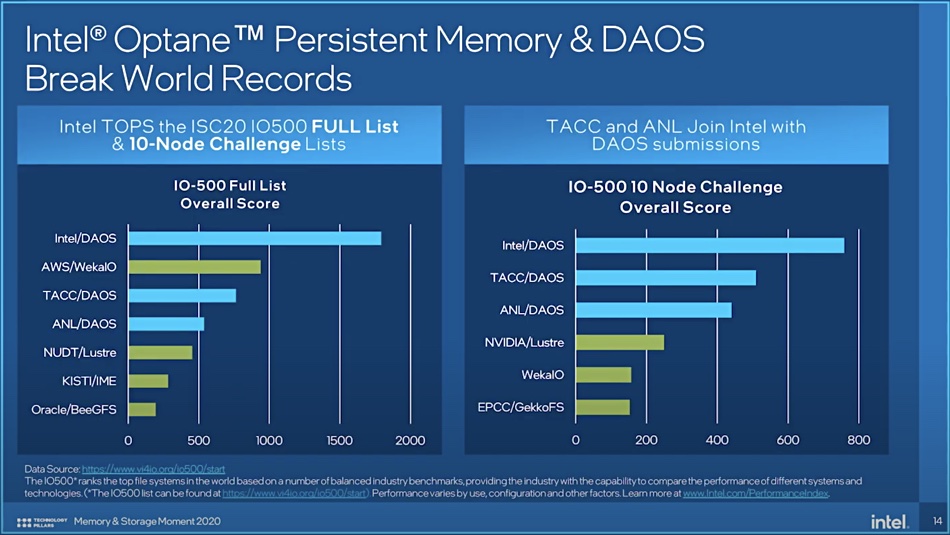

The relevant Intel DAOS and Weka IO500 scores are:

Intel DAOS + Optane PMem 200 Series – 1,792.98

WekaIO – 938.95

Intel DAOS + Optane PMem 100 Series – 933.64

Intel DAOS IO500 scores.

The extra performance of the gen 2 4-deck 3D XPoint-based PMem 200 Series DIMMs over the first generation PMem 100 Series almost doubled Intel’s DAOS score.

DAOS is obviously a fast file system, and also cheap – it’s open source. But users have to commit to using Optane PMem products to get the best use out of it. A trade-off calculation is required; is DAOS + Optane PMem as cost effective as WekaIO’s software?

Kelsey Prantis, a senior software engineer at Intel, discusses the DAOS system in a YouTube video.

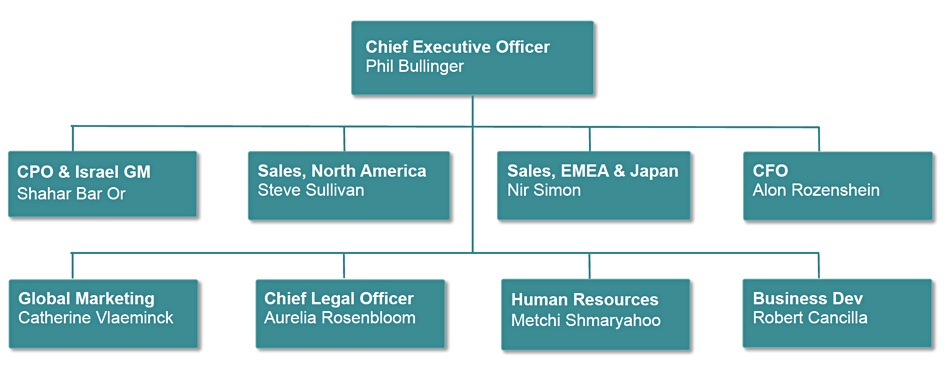

Infinidat, the enterprise large array supplier, has appointed a new CEO and CFO, replacing its co-CEO structure and completing the leadership transition from founder Moshe Yanai’s era.

The new CEO is Phil Bullinger, the ex-SVP and GM of Western Digital’s Data Centre Business Unit. This business unit was largely shelved by WD in September 2019, with the IntelliFlash product sold to DDN and the ActiveScale archival array to Quantum.

Phil Bullinger.

Scott Gilbertson, a member of the Infinidat Board of Directors, supplied a statement: ”Phil’s breadth of experience overseeing product development, strategy, and operations will enable him to lead Infinidat as it delivers the innovative and agile storage technologies its customers require for sustained competitive advantage.”

Bullinger joined WD in 2017 from EMC where he was the SVP and GM for its Isilon business unit.

Infinidat has hired Alon Rozenshein as its new CFO. Former co-CEO Nir Simon, becomes the sales head for the EMEA and Japan territories. The other co-CEO, Kariel Sadler, left the company last month. Rozenshein joins from Clarizen, a company that Infinidat executive chairman Boaz Chalamish also chairs. Chalamish’s role at Infinidat may change in the coming months, as he has finished “shepherding the company through its transition”.

Bullinger is based in Colorado and is not relocating to Infinidat’s Tel Aviv headquarters. Instead there will be lot of teleconferencing until the pandemic restraints ease, and then he will be well-positioned to meet face-to-face with Infinidat’s US customers, the company told us.

A Chalamish statement said: “As we focus on executing the company’s strategy, we can rest assured that the new leadership will continue to carry on our cohesive, globally-facing approach to the market – while working closely with the Israeli-based engineering and product operations teams”.

Bullinger confirmed that founder Moshe Yanai is an active Chief Technology Evangelist for Infinidat, is “a huge advocate for Infinidat” and remains a major investor. Bullinger also said that Rozenshein is a “very strategic CFO”.

He told Blocks & Files that Infinidat is profitable, cashflow positive, and growing. The company grew in each 2020 quarter, and posted significant Y/Y growth in the fourth quarter. There was 24 per cent growth in PB deployed Y/Y in 2020, and 10 new Fortune 500 customers came on board in the year, with an average deal size of more than $1.3m. The company also hired extra staff in the fourth quarter.

Infinidat executive management team.

Bullinger said the Infinidat management team is experienced and solid and hisf ocus is to ensure the company executes its strategy and continue its profitable growth. His priorities include growing go-to-market capability, and scaling sales and engineering. There will be product enhancements to increase Infinidat’s value to its customers, he added.

Infinidat has now completed its changeover from being led by its founding CEO, guiding engineering light and Israel-based Moshe Yanai, to be a possibly more global business led by Bullinger.

Bullinger said the Covid-19 pandemic had levelled the playing field in one way. Because sales teams could not visit or, indeed, dominate customers with face-to-face sales team attention, there was a reliance on Zoom-style meetings and documentation. This was favourable to Infinidat and the company was getting involved in more requests to tender.

Michael Tso, CEO of Cloudian, the object storage vendor, thinks I am wrong. For example, Outposts is severely limited when it comes to object storage, he says.

Tso told us: “Outposts is an enabler for Cloudian, similar to VMware, AzureStack and Anthos. Cloudian is very good at storing massive amounts of data, but users must stand up their own on-premises compute environments to work with the data.” Outposts can provide that on-premises compute environment.

Cloudian’s support of and partnerships with VMware, Azure Stack, Google Anthos and Outposts have helped it gain over 500 enterprise and government customers.

Michael Tso

I put it to Tso that “Outposts with S3 competes with on-premises Cloudian.”

Think again, he replied: “Our business has surged since Outposts was announced two years ago (plus AzureStack and Anthos), which I think is due to two reasons.”

“The first is that Outposts (as well as AzureStack and Anthos) unequivocally validated why we started Cloudian eight years ago: data gravity leads to cloud [data] needing to be distributed rather than centralised. Cloud compute will need to move closer to the data because moving data is very expensive and time consuming. The Outposts website states why someone would want to use the service and includes low latency, local data processing and data residency – all of which have been our consistent message for the last eight years.”

Hybrid cloud era

Tso acknowledges that on-premises storage vendors need to innovate to stay competitive with cloud storage service suppliers, and their on-premises systems. Cloudian “has invested heavily in the right differentiation areas and propelled our growth in this new hybrid-cloud era.”

Hardware players need to have “cloud-like elasticity in capacity and pricing, ” he says. “Software players need to provide more cloud-like features such as easy management, elastic capacities, cloud-native S3 APIs, and multi-tenancy and also differentiate in areas like security/air gap, IT policies/storage efficiencies, multi-cloud, etc.”

But surely, Outposts represents competition for Cloudian?

Tso replied: “In the two years since Outposts have been around, we have never seen them pop up as competition, rather only as an opportunity to collaborate.”

How come?

“Outposts S3 is quite different from AWS S3. Think of it as more of a cache – its control plane is in AWS, so it must always be ‘tethered’, and it runs on HCI (hyperconverged infrastructure) hardware, so it’s currently limited to 96TB per Outposts deployment with associated costs. In contrast, Cloudian scales to EBs, can operate in ‘air gap/dark site’ mode, and is frequently lower cost.”

“The model is entirely different, and so is the technology… Ultimately what Cloudian specialises in (distributed storage) is very, very hard at scale – both in terms of data volumes and number of deployments/configurations. While compute is elastic and portable, the technology for data persistence, resilience, security and sovereignty at scale in diverse enterprise network environments is very different from public cloud storage.“

According to TSO, AWS and Cloudian share the goal of using the S3 protocol for data on-premises instead of having it locked away in traditional silos. This S3-commonality makes that data friendly to cloud-native applications, such as AI, ML and analytics.

OK, So AWS Outposts is good for Cloudian today and presumably it is good for some other storage hardware vendors too. But tomorrow? Let us remind ourselves that Amazon is playing the long game, a game in which it sets the rules.

SoftIron, the startup storage supplier, use Arm processors instead of x86 CPUs for controllers in its Ceph-based HyperDrive. This provides scale-out storage nodes behind a storage router front-end box which processes the Ceph storage requests. It also has an Accepherator FPGA-based erasure coding speed-up card.

In this email interview SoftIron co-founder and CEO Phil Straw explains that Arm-powered storage is not the be all and end all. Indeed, FPGA acceleration can go further than Arm CPUs.

Phil Straw

Blocks & Files:What did you learn by using Arm?

Phil Straw: “What we learned with ARM is that the core itself is not magic in and of itself but it does have things you can lean on over and above x86. ARM is just a hardware executor of sequence, selection and repetition…and in many ways it is weaker than x86 (often). It is low power and has a different IO architecture.

“We took ARM and made it an IO engine that does compute (to serve storage); which makes an awesome storage product in one category. That is to say we did not take a computer and make it a storage product. That’s what we really discovered. ARM for us is low power and awesome at spinning (disk) and hybrid (flash+disk) media.

Blocks & Files: That’s the disk and disk-flash area. What do you use with all-flash storage?

Phil Straw: “We are also agnostic about technology and we are now servicing SSD/NVMe with x86 and doing the same things (not building computers but coming low level and leveraging AMD Epyc as a storage-from-birth architecture)…the results are also spectacular. More soon.

Blocks & Files: Tell us about host server CPU offload.

Phil Straw: “I think what is interesting here is not the ARM versus xxx debate or ARM being in any way a magic sauce. What is interesting is that storage and SDS in particular can have the potential to need processing. Adding extra tasks outside of the main processing does provide advantages.

“We at SoftIron have already demonstrated erasure coding inline with the network-attach. More to come there too because the advantages are there to be had. The extra processing can be useful either inline in the network or just as an adjunct to main processing. What is interesting is the idea of hand off, parallelism and avoiding dilution of input and output to storage and network.

Blocks & Files: Why are X86 server CPUs ill-suited to this kind of work?

Phil Straw: “Often when you take a computer the I/O paths are not optimised and by that I mean at all the levels in the stack. Firmware in the configuration of the processor, NUMA, UEFI/BIOS, kernel, drivers and the storage stack. Also in hardware as the chip is connected and used. As a result the storage throughput can be as much a half diluted by this phenomenon (SoftIron empirical test data, proven in x86 and ARM design) or, said another way, doubled by doing it custom for storage.

Blocks & Files:Is such optimisation all that’s needed?

Phil Straw: “For us the biggest yield has not been in extra compute once the bottom up design is for storage (and not a computer first) but the laws of compute and physics do always benefit from parallelism. They almost have to always. For this reason we use FPGA’s and have replicated hardware that sits inline with the network. This allows choke point compute that would be serialised in a processor to be handed to a highly parallel engine. The ARM processor network path is similar but different. We tried this path before we ended up using FPGAs for storage acceleration…for these reasons above.

SPU

Softiron is one of three startups that are using ARM processors for their storage controllers – the others are Nebulon and Pliops.

Nebulon is shipping a storage processing unit (SPU) to control aggregated storage in servers.

Pliops is developing an SPU that functions as a key-value (KV) based storage hardware accelerator, sitting in front of flash arrays, that speeds storage-related app processing and offloads the host server CPU. It works with block storage and key:value APIs and says its Pliops Storage Processor accelerates inefficient software functions to optimise management of data persistence and indexing tasks for transactional databases, real-time analytics, edge applications, and software-defined storage (SDS).

The idea of adding hardware-acceleration to storage related processing as a way of both speeding storage work and offloading host server CPUs emerged in 2020. It was part of the overall data processing unit (DPU) concept, with specific hardware used to accelerate storage, security, network and system composing workloads.

Blocks & Files thinks we will hear much more about DPUs and SPUs in 2021.

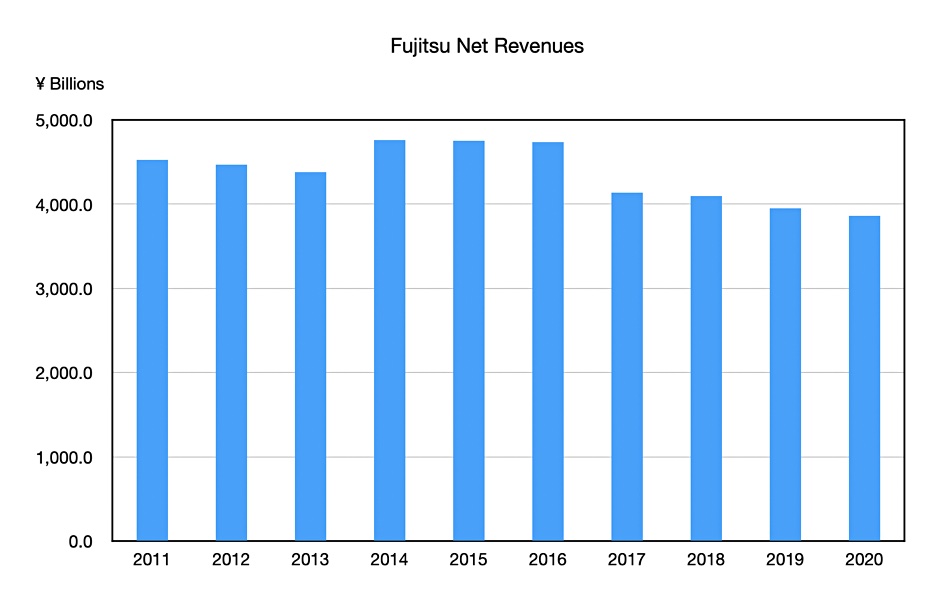

Fujitsu has embarked on an ambitious M&A programme to enable it to supply “transformational services [in a] very competitive” market. The Japanese tech giant has drawn up a list of 20 potential targets, according to the FT.

Nicholas Fraser, an acquisition consultant from McKinsey who joined the company in March 2020 to lead the investment programme, wrote in Fujitsu’s fiscal 2020 report: “To build the capability we need to deliver what our customers need, we must move fast to evolve what we do. Inorganic growth, encompassing both acquisitions and venture investments, is a powerful tool for accelerating this evolution. Inorganic growth is most effective when it is done programmatically. This means doing a number of deals each year and not just one or two every few years.”

He added: “DX (digital transformation) is about both digital (technologies) and transformation (capability). We are filling our investment pipeline with opportunities that help us on both of these fronts: gaining differentiation in digital technologies such as AI, advanced data/analytics, or cybersecurity, and gaining capability to engage customers in transformative discussions.”

Adoption of 5G phone services is also a focus area, with US sanctions on Huawei opening up more opportunities for Fujitsu. The coronavirus pandemic has also accelerated Fujitsu customers’ adoption of remote working and digital services.

The new acquisition programme is part of Fujitsu’s ¥600bn ($5.7bn) digital transformation drive.

Takahito Tokita.

Fujitsu president and CEO Takahito Tokita told a 2019 Fujitsu annual forum audience that the company needed to change to a global services focus because its current hardware-focus made it unbalanced.

In the fiscal 2020 annual report, he stated: “We have not yet turned the corner toward growth, and frankly, we recognise that rebuilding our global business is the most challenging of the four priority issues.”

Nine year revenue history shows stagnation and gentle decline.

He said: “We are also working to build an ecosystem that supports DX through M&As and investments in venture companies. For example, in light of the now widespread view that data will be the “new oil” of the global economy, we are collaborating with companies that have advanced software platforms for data analysis. By doing so, we are keen to create new markets that did not exist before and establish a competitive advantage in them.”

Background notes

Fujitsu had sales of about ¥3.8 trillion in fiscal 2020 – about $35.5bn – and employs 130,000 people worldwide. It has a comprehensive server and storage hardware product line featuring, for example, supercomputers, Primergy servers and ETERNUS storage arrays. But it also has legacy hardware products such as mainframes and SPARC servers. It divested its PC business to Lenovo in 2017 and sold off its Arrow smartphone business in 2018.

Recently it has taken up OEM and reselling partnerships in the storage area, and supplies NetApp arrays, Commvault appliances, Datera enterprise storage software, Quantum tape libraries, Qumulo filers, and Veritas data protection products.

We might expect changes are coming to Fujitsu’s server and storage businesses, such as subscription-based business models and cloud-based management.

A New York hedge fund spoiled Intel’s Christmas with calls for the company to get its act together. Dan Loeb, CEO of Third Point, said in a letter published Dec 29 that the semiconductor giant was going through a”rough patch”.

Third Point has amassed a near-billion dollar stake in Intel and you can read Loeb’s letter, addressed to Intel chairman Dr. Omar Ishrak, in full here, but here is the nub of his comments:

Intel has declined, market cap is down, staff morale is low and the board is neglecting its duty.

Intel must correct process lag with Asian competitors TSMC and Samsung.

Nvidia and ARM are using Asian competitors and eating Intel’s lunch

This has US national security implications – US needs access to leading edge semiconductor supply (presumably by retaining semiconductor manufacturing capacity in the US).

Loeb’s recommendations

Should Intel remain an integrated device manufacturer?

Intel needs to figure out how to serve its competitors as customers – e.g. making chips designed by Apple, Microsoft and Amazon that are currently built in East Asia.

Potential divestment of “certain failed acquisitions”.

For the sake of argument, let’s assume that Intel takes on board Third Point’s suggestions. It is unclear at time of writing if Loeb wants Intel to split itself into two separate corporate entities – a fabless chip designer and a US fab business – or if he wants the company to pursue the Amazon-AWS route. We suspect he has the the first option in mind, as an independent foundry could potentially open to its doors to AMD and Nvidia.

That said, it is highly unlikely that the maker arm of Intel could quickly retool its fabs to, say, make ARM chips for the likes of AWS and Apple. Any move into contract manufacturing would require substantial and sustained investment. We have no insight into which “failed” acquisitions Loeb is referring to, but note that Altera ($16.7bn) and MobileEye ($15.3bn) are the big recent acquisitions.

Optane stuff

But what about Intel’s Optane-branded 3D XPoint SSD and Persistent Memory business? The company is estimated to have “lost well over one billion dollars per year in 2017-2019 to bring 3D XPoint to the break-even point,” according to the tech analyst Jim Handy.

Today, it buys in chips from Micron and plans to manufacture gen 3 and gen 4 Optane chips. But why? The company is doubling down on its commitment to Optane -and may even have moved into operating breakeven point.

Intel is using Optane as a defensive moat for its x86 server chip business against AMD. This logic relies on customers agreeing it is worthwhile spending extra money on servers with Xeon CPUs and DRAM to buy Optane persistent memory. And Optane is building up steam in AI, machine learning and financial trading applications. But is this a big enough market?

The hyperscalers, who are the biggest purchasers of server chips, have displayed little interest. AWS, for example, one of Intel’s largest customers for its Xeon CPUs, has developed Graviton server instances that use its own Arm-based CPUs.

If AWS is adding Arm-powered server instances because they are better for microservices-based apps. We think it likely other public cloud and hyperscale cloud services suppliers will follow the same route.

Because of this and because of Loeb’s input, Blocks & Files thinks that it is possible we will see Intel rowing back on Optane persistent memory and SSDs in 2021, and possibly even sell the business to Micron. Intel is now selling its NAND memory business to SK hynix, which would make an Optane spin-off suggestion even more likely.

As Handy says: “The economies of scale have allowed Intel to finally reach the break-even point, and from now on Optane is likely to either continue to break even or to make a profit. This is enormously important if the company ever wants to spin off the Optane business. A spin-off seems very likely since Intel has exited nearly every memory business it has participated in since its founding: SRAM, DRAM, EPROM, EEPROM, NOR flash, Bubble Memories, and PCM. The only two left are NAND flash and 3D XPoint.”

Infinidat co-CEO Kariel Sadler left the company without fanfare last month. His departure may pave the way for the appointment of a sole CEO.

Eran Brown, Infinidat’s EMEA and APAC field CTO also left the firm in December, to work for AWS. Dan Shprung, EVP EMEA and APJ, left Infinidat in October to join Model9 as Chief Revenue Officer.

Sandler’s LinkedIn profile reveals he stopped working at the enterprise large array supplier in December, after nearly ten years with the company. He now describes himself as “Ex co-CEO at Infinidat.”

Kariel Sandler

Infinidat instituted the co-CEO scheme in May last year, following the sideways move of founder and CEO Moshe Yanai to become Chief Technology Evangelist.

Infinidat outsider Boaz Chalamish became executive chairman of the board. COO Kariel Sandler and CFO Nir Simon were appointed as Co-CEOs, nominally replacing Yanai.

The co-CEO function started looking shaky in November when Shahar Bar-Or was hired from Western Digital and appointed Chief Product Officer and General Manager of Infinidat’s Israel operations. He reports directly to executive chairman Boaz Chalamish. In our view, this makes Chalamish effectively the CEO of the company.

Sandler was a long-time associate of Yanai, working with him at IBM, which acquired XIV, and XIV before Infinidat was started up.

All storage media technologies saw increased density in 2020 – tape, disk, flash, persistent memory and even DNA. However QLC flash advances meant the nearline disk bastion is now under attack.

Overall there was no single major step forward that turned the storage world on its head last year. DNA storage developers amazed everybody with what they could do but this cuts no ice with storage professionals buying devices to store data now. They want data accessed in microseconds or milliseconds, not days.

Tape

Tape began the year with LTO-8 (12TB raw) and finished with a reduced capacity LTO-9 format – 18TB raw instead of original 24TB. The 2019 interruption in LTO-8 shipments due to the legal spat between manufacturers FujiFilm and Sony, while demand for tape capacity rose, means that LTO-8 capacity is no longer high-enough, so LTO-9 is being brought forward.

Showing tape capacity has a long runway ahead, Fujifilm and IBM demonstrated a 580TB capacity tape. This is 32 times more than current LTO-9 capacity and required a tape that was 1,255m long.

This provides a vivid insight into tape data access speed as streaming three quarters of a mile of tape through a drive will take several minutes. According to Quantum document, streaming time is increasing as tape’s physical speed through a drive is decreasing;

LTO-6 @ 6.83 m/sec when reading or writing

LTO-7 @ 5.01 m/sec

LTO-8 @ 4.731 m/sec.

We don’t have a LTO-9 tape speed number. Quantum said: “Slower tape speed is an enabler for future generations of LTO drives to offer higher data rates.” At 5m/sec it would take 251 seconds to move the full length of an LTO-9 tape through a drive.

Tape search speed is faster, 10m/sec with full height LTO-8 drives. That means it could take 125.5 seconds to stream the tape through the drive when looking for a piece of data – still slow compared to disk.

LTO-9 tape has 12 Gb/in2 areal density. An 18TB disk drive has 1022 Gb/in2. That means LTO-9 tape can achieve the same 18TB capacity with only 1/85th of the areal density than that of an 18TB disk. No wonder tape’s area density has such a large development head room.

Disk

Disk began 2020 with the standard 3.5-inch nearline drive storing 16TB, and ended it with 18TB and 20TB drives from Western Digital and Seagate. Both companies are developing next-generation technology to progress beyond current Perpendicular Magnetic Recording (PMR). This technology is reaching a dead end beyond which capacity can increase no further, due to the bit areas becoming too small to hold data values in a stable manner.

Western Digital intends to use microwaves to write data to a more stable recording medium called MAMR technology, while Seagate is overcoming its new medium’s resistance to change by using temporary bursts of heat (HAMR). Seagate has started shipping HAMR drives but Western Digital is only shipping partial MAMR tech drive drives using so-called ePMR technology.

We anticipate WD to ship MAMR drives this year, and Toshiba, the third disk drive manufacturer, to follow suit.

Dual or multi-actuator tech appeared in 2020, with Seagate adopting the technology. There are two read/write heads and they divide a disk drive into two logical halves that perform read/write operations concurrently to increase overall IO bandwidth.

But, even so, the time to access data on a disk depends mostly upon the seek time. This is the time needed to move a read/write head to the right track, and then for the track to spin under the head until the right data block is accessed. This can take between 5 and 10 milliseconds (5,000µs and 10,000µs). The data access latency for a QLC (4bits/cell) SSD is in the 100µs or less area – up to 1,000 times faster. That opened the door for QLC SSDs to go after the nearline capacity storage business.

Flash

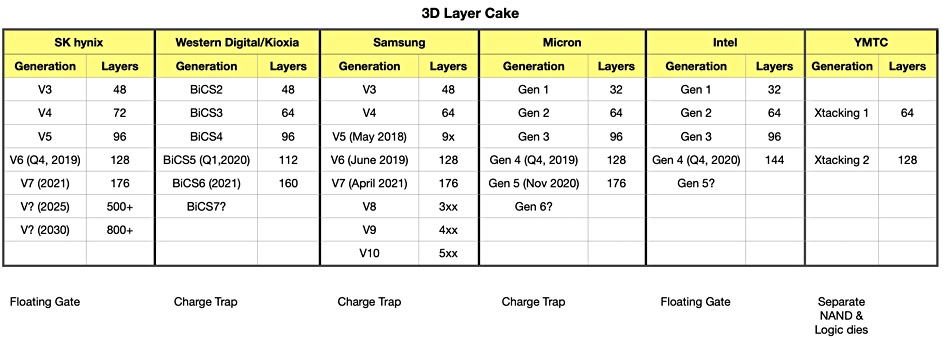

The big stories with flash and SSDs have been the increasing 3D NAND layer count and the rise of QLC (4bits/cell) NAND.

A table illustrates the layer count increase clearly.

Western Digital and Kioxia started 2020 with 96-layer 3D NAND in production and 112 layer in development. The pair now have 160-layers in development. Samsung and SK hynix are moving from 128-layer to 176-layer. Intel moved from 96 layer to 144 layer. (It also sold its NAND business to SK hynix late last year but that sale won’t complete until 2025.)

In general, adding 48 or so layers to a 3D NAND die increases manufacturing cost but assuming similar or better manufacturing yields, there is an overall decrease in cost/TB.

Adding a fourth bit to each cell increases capacity by a third. QLC flash doesn’t last as long as current TLC (3bits/cell) flash so extra over-provisioning cells are needed to compensate for worn-out cells. Even so, 150-layer-plus 3D NAND with QLC cell formatting, provides a flash SSD that is cheaper to make than a sub-100-layer TC flash SSD.

In April, Micron aimed its 5210 ION QLC NAND SSD at the nearline disk drive replacement market.

We now have many flash array suppliers adding QLC flash to their product lines; Pure Storage, NetApp, Nexsan, StorONE and VAST Data.

Tech developments suggest that the SSD threat to disk will intensify. Intel suggests that coming PLC (5bits/cell) NAND will enable the total cost of SSD ownership to drip below that of disk in 2022.

Persistent Memory

There is one main persistent memory game in town, and that’s Intel’s Optane. But let’s give a nod to Samsung’s Z-SSD.

The Z-SSD had a big win in 2020, with IBM adopting it for the FlashSystem arrays, with up to 12 x 1.6TB Z-SSDs supported.

Optane SSDs, which are not persistent memory products, but faster SSDs, were used by StorONE in its S1 Optane Flash Array, and also by VAST Data.

StorONE S1 Optane array.

Intel started shipping second generation 3D XPoint technology in 2020, meaning 4-layers, double that of the gen 1 products. The company announced three products using gen 2 XPoint: PMem 200 Optane Persistent Memory DIMMs, server-focused P5800X Optane SSDs, and an H20 client SSD combining a gen 2 Optane cache with 144-layer QLC 3D NAND.

Intel put in a sustained and concerted effort throughout 2020 to increase its support by applications. The hope is that, as customers take up these applications they will buy Optane persistent memory to send their performance to a higher level.

To date, adoption of Optane persistent memory – Optane DIMMs used as quasi-DRAM to expand a server’s memory pool – has been muted. But the adoption of the PCIe Gen 4 bus, twice the speed of PCIe 3.0, could deliver a bigger bangs-per-buck bump than Optane for less cash.

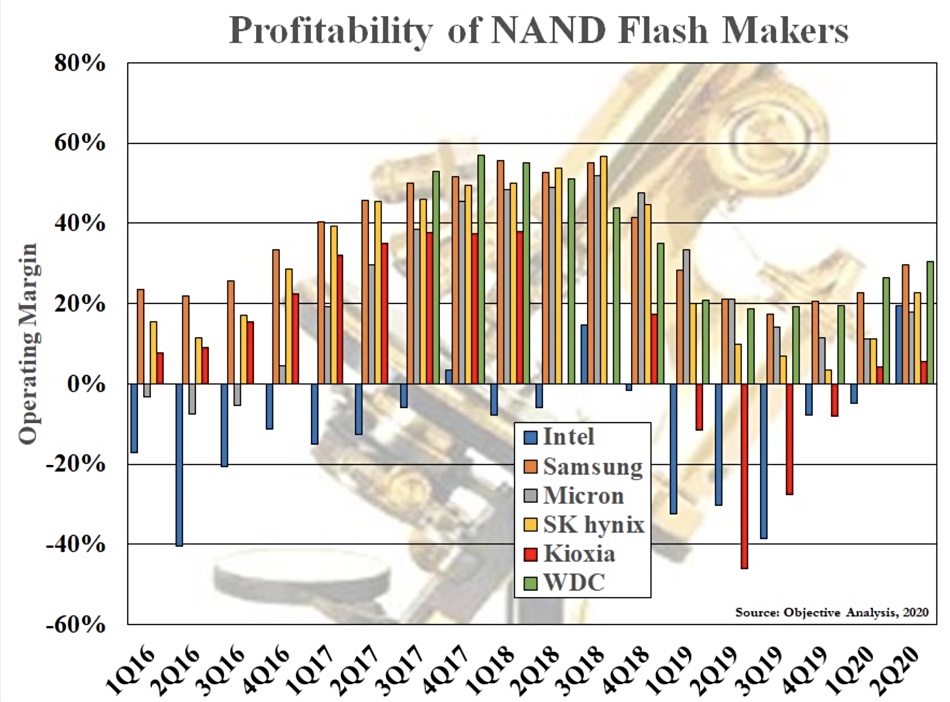

Intel in December outlined two coming Optane technology generations, with no performance details. All-in-all, Intel is making slow progress although it may have turned the corner on Optane profitability, according to tech analyst Jim Handy, in a blog in August. He included a chart in the blog;

This shows the operating margin of NAND manufacturers from 1Q 2016 to 2Q 2020, with Intel’s Non-volatile Solutions Group represented by a blue bar that’s mostly in negative territory. Handy thinks this is due to Optane losses. However, in 2020 the picture changes. NSG made a 19 per cent positive margin in 2020’s second quarter.

Handy comments: ”Intel has lost well over one billion dollars per year in 2017-2019 to bring 3D XPoint to the break-even point.”

He says: “The economies of scale have allowed Intel to finally reach the break-even point, and from now on Optane is likely to either continue to break even or to make a profit. This is enormously important if the company ever wants to spin off the Optane business. A spin-off seems very likely since Intel has exited nearly every memory business it has participated in since its founding: SRAM, DRAM, EPROM, EEPROM, NOR flash, Bubble Memories, and PCM. The only two left are NAND flash and 3D XPoint.”

Intel is now selling its NAND memory business to SK hynix, which would make Handy’s Optane spin-off suggestion even more likely.

DNA

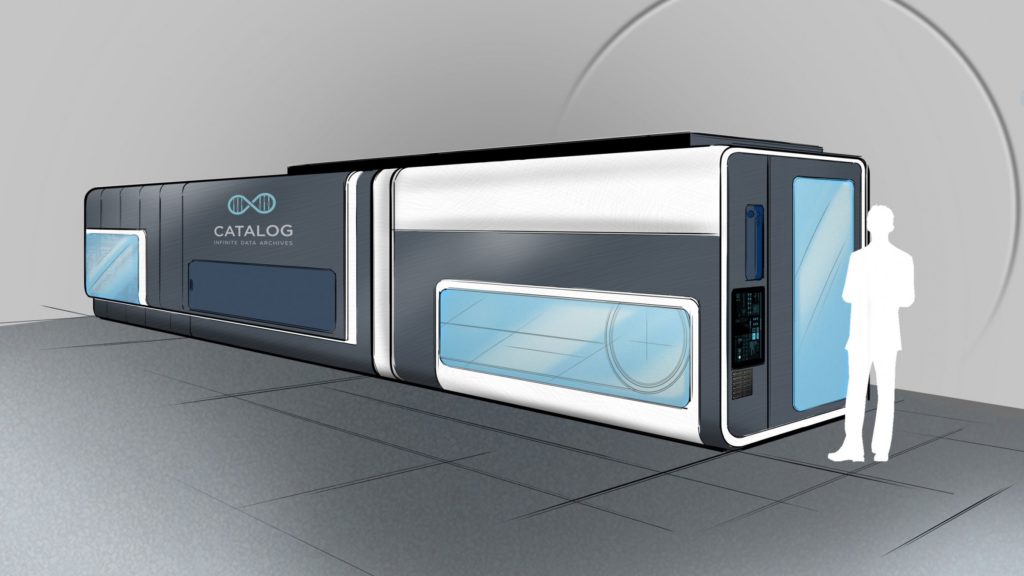

DNA storage came into prominence a couple of times last year, with its fantastic promise of extraordinary capacity in a small space. But that extraordinary capacity; one gram of DNA being able to store almost a zettabyte of digital data, one trillion gigabytes, comes at a cost.

Catalog DNA storage unit.

A lot of mechanical movement, chemical reactions, complicated lab machinery and time is needed. A Microsoft and University of Washington demo system had a write-to-read latency of approximately 21 hours for a 5-byte data payload.

But, again, scientist-led startups like Twist BioSciences and Catalog are pushing the DNA storage envelope forward and we might hear more about it in 2021. Indeed, Catalog now has a $10 million war chest to fund its development.

VMware is suing its former COO and now new Nutanix CEO Rajiv Ramaswami for contractual misdeeds.

The company’s complaint revolves around alleged secret talks between Ramaswami and Nutanix while he was working on “VMware’s key strategic vision and direction” with other VMware senior leaders.

In a statement, VMware said it has initiated legal proceedings in California, against Ramaswami “for material and ongoing breaches of his legal and contractual duties and obligations to VMware.”

Ramaswami joined Nutanix as CEO in December, two days after leaving VMware.

The VMware lawsuit alleges “Rajiv Ramaswami failed to honour his fiduciary and contractual obligations to VMware,” because he was “meeting with at least the CEO, CFO, and apparently the entire Board of Directors of Nutanix, Inc. to become Nutanix’s Chief Executive Officer.”

VMware declared it is not a litigious company by nature and has “tried to resolve this matter without litigation. But Mr. Ramaswami and Nutanix refused to engage with VMware in a satisfactory manner.”

Nutanix in a statement said: “VMware’s lawsuit seeks to make interviewing for a new job wrongful. We view VMware’s misguided action as a response to losing a deeply valued and respected member of its leadership team.”

Rajiv Ramaswami.

The company added: “Mr. Ramaswami and Nutanix have gone above and beyond to be proactive and cooperative with VMware throughout the transition. Nutanix and Mr. Ramaswami assured VMware that Mr. Ramaswami agreed with his obligation not to take or misuse confidential information, and VMware does not contend otherwise.”

This was apparently not enough as “VMware requested that Mr. Ramaswami agree to limit the ordinary performance of his job duties in a manner that would equate to an illegal non-compete covenant, and it requested that Nutanix agree not to hire candidates from VMware in a manner that Nutanix believes would be contrary to the federal antitrust laws.”

Nutanix believes “that VMware’s action is nothing more than an unfounded attempt to hurt a competitor and we intend to vigorously defend this matter in court.”

Comment

The two company statements represent what they want to say in public about their dispute and we don’t know what they said in private. It seems apparent that VMware feels threatened, even betrayed, by Ramaswami’s move to Nutanix and wants to limit the damage it perceives could result from the move.

A US employment contract may have a non-compete clause in it which forbids the employee from leaving and working with a competitor until a certain amount of time has passed after their resignation.

However such non-compete clauses are not enforceable in California law and VMware’s statement does not mention the “non-compete” phrase. Instead it alleges Ramaswami has breached his legal and contractual duties and obligations.

That said, the VMware lawsuit appears similar in nature to a non-compete dispute, particularly as its statement mentions Ramaswami having talks with Nutanix when he was working on “VMware’s key strategic vision and direction”. This implies Ramaswami could direct Nutanix activities from a standpoint of knowledge of VMware’s strategies; the kind of thing non-compete clauses are designed to prevent.

Nutanix’s claim that VMware “seeks to make interviewing for a new job wrongful” sets the scene for a court decision on how far legal and contractual duties and obligations extend into seeking new employment.

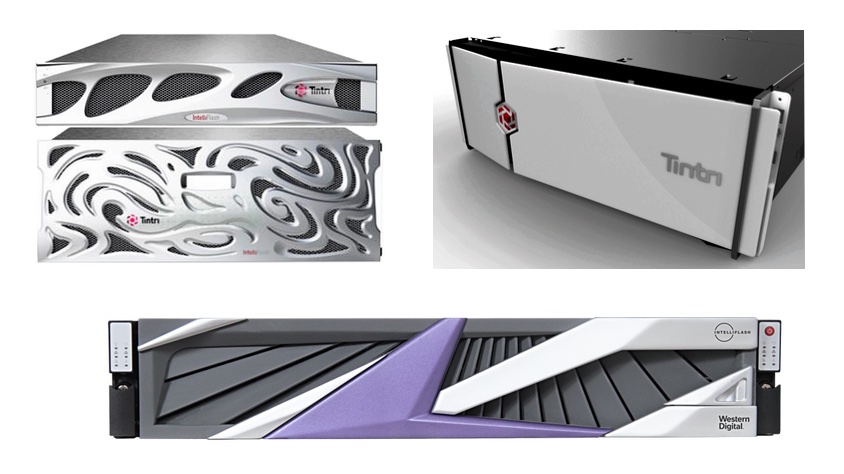

Bezels, like car radiator grilles, perform a function. They allow cooling air to enter a rack enclosure whilst protecting the delicate internal components from damage. That allows the bezel designer a lot of latitude in creating a bezel that’s pleasing to the eye while fulfilling its air ingest and protection roles.

These front panels should be icons of distinction, as finely crafted as car radiators, elegant badges bringing light, inspiration and imagination to dull rack walls in data centres. So let’s fight bezel boredom.

In the interests of good bezel design and improving the mental wellbeing of data centre admin staff, we’ll explore some examples of the good, the bad and the ugly in the bezel universe.

Embezeling, here we go

Let’s start at the bottom, with the ugly ones, grilles with logos:

What a utilitarian bunch. Why not add some colour?

Better, but we could do more, so much more:

That’s more like it. Top marks, Caringo! And well done, Backblaze with those red pods.

We could have lit-up logos:

A bit more adventurous with the shapes and colours?

Yes, well, okay DDN, perhaps not.

What about pretend-it’s-not-a-grille bezels;

What about collecting bezels, a nice addition to any wall?

Snapped this before the buildings were sold to Google. Signed by the hardware engineers that worked on the projects. pic.twitter.com/50zv1Jz524

You can see CEO Scott Dietzen’s signature, John Cosgrove’s, Max Kixmoeller’s and others. That is a bezel to treasure. You look at it and you think; “What a flash array!”

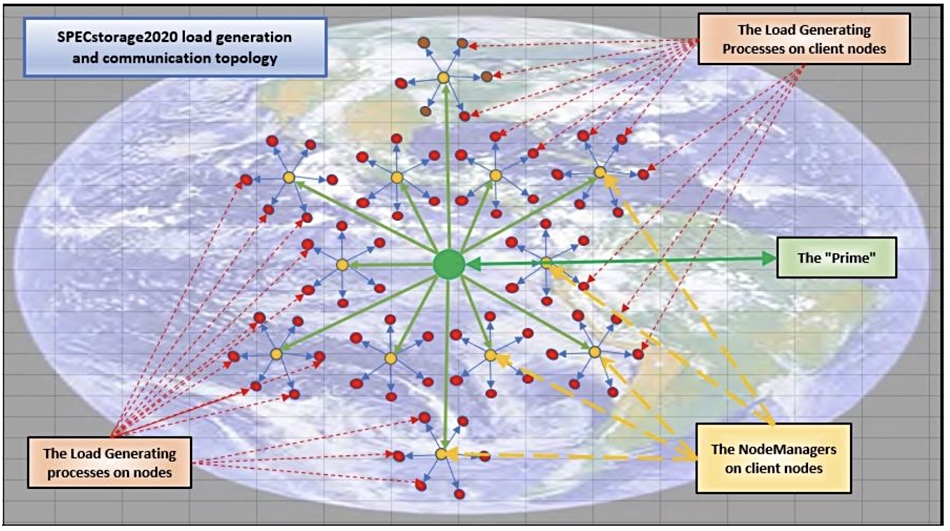

One of the more complicated file storage performance benchmarks is being replaced – by a successor that is even more complicated.

The SPECsfs 2014 SP2 benchmark determines file performance in five different workloads: software builds, video streaming (VDA), electronic design automation (EDA), virtual desktop infrastructure (VDI) and database. Each category test gets a numerical score and overall response time (ORT).

The new SPEC Solutions 2020 benchmark modifies the SFS 2104 SP2 test by adding two new workloads, dropping two existing ones, and tweaking the test methodology. This means that the new benchmark results cannot be compared to the old ones.

There is a new AI_IMAGE (AI image processing) workload, representative of AI Tensorflow image processing environments, and a new Genomics one. The existing SPECsfs 2014 software build, EDA and VDA workloads are retained but the VDI and Database workloads are being scrapped.

That’s because the technology of these has changed and is continuing to evolve. These workloads could be re-introduced later, after the collection of new base trace data has been completed.

SPEC Solutions 2020 benchmark scaling diagram.

The test scale has substantially increased. SPECsfs2014_SP2 scaling was up to 60,000 load-generating processes globally. This is expected to increase to around 4 million load-generating processes distributed globally in SPEC Solution 2020. All of the geographically distributed load generating processes will be kept in sync, at a sub millisecond resolution.

The updated benchmark has a new statistical collection mechanism that enables users to extract runtime counter information and load it into a database for graphical representation by, for example, Graphite, Carbon, and Grafana.

SPEC Solution 2020 graphical output.

SPEC Solution 2020 can support a non-POSIX storage system with a plugin shared library for accessing an AFS storage service. Others may be added in the future, such as an object store, S3, Ceph, and more. The new test supports custom workloads for private, no-publishable testing. It’s also possible to combines Unix and Windows load generators in a workload definition.