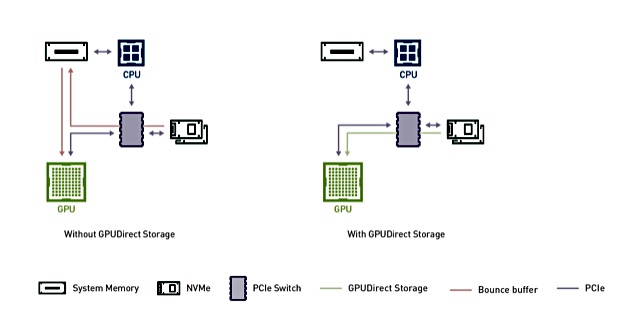

Nvidia has crafted a direct link between its GPUs and NVMe-connected storage to speed data transfer and processing.

Until now a GPU was fed with data by the host server’s CPU, which fetched it from its local or remote storage devices. But GPUs are powerful and can be kept waiting for data; overwhelmed server hosts simply can’t deliver data fast enough.

GPUDirect Storage cuts out the host server CPU and its memory, calling it a bounce buffer, and sets up a direct link between the GPU, a DGX-2 for example, and NVMe-connected storage, including NVMe-over-Fabrics devices.

GPUDirect Storage uses direct memory access to move the data into and out of the GPU, which has a direct memory access engine.

The results are promising. For instance, in a blog the company noted: “NVIDIA RAPIDS, a suite of open-source software libraries, on GPUDirect and NVIDIA DGX-2 delivers a direct data path between storage and GPU memory that’s 8x faster than an unoptimised version that doesn’t use GPUDirect Storage.”

And in a developer blog Nvidia said: “Whereas the bandwidth from CPU system memory (SysMem) to GPUs in an NVIDIA DGX-2 is limited to 50 GB/sec, the bandwidth from many drives and many NICs can be combined to achieve maximal bandwidth, e.g. over 200 GB/sec in a DGX-2. “

Xilinx has launched a FPGA that supports PCIe v4 and uses high-bandwidth memory to munch data manipulations faster and firehose the results.

Field-programable Gate Arrays (FPGAs) are reprogrammable hardware products used as CPU accelerators. Xilinx, founded in 1984, invented FPGA devices, also known as programmable logic devices.

The Alveo U50 follows on from existing U200 and U250 accelerators, which connect to host systems across PCIe v3 and use DRAM memory.

The half-height, half length device delivers a claimed 10-20x improvement in throughput, latency and power efficiency, with a 75-Watt power envelope.

It has 8GB of high-bandwidth memory (HBM2) with greater than 400 Gbit/s data transfer speed, and 100Gbit/s external connectivity. That helps support for NVMe-over-Fabrics and disaggregated computational storage – a hint about composable systems.

Target application areas are deep learning inference, data analytics, computational storage, network acceleration and financial modelling.

For data analytics, Xilinx claims the U50 provides 4x higher throughput per hour and reduced operational costs by 3x compared to in-memory Xeon Platinum 8260 CPU, with a 24ms query time compared to the Xeon’s 210ms.

Xilinx is showcasing the Alveo U50 at the Flash Memory Summit 2019, August 6-8 at Santa Clara.

The Alveo U50 is sampling now with OEM system qualifications in process. General availability is slated for Fall 2019.

Excelero, the NVMe-over-Fabrics flash array software startup, has announced a scale-up NVEdge product to complement its scale-out NVMESH offering.

NVMe-over-Fabrics (NVMe-oF) extends the PCIe/NVMe protocol across network links so a server application can access remote flash drives for block data as if they were local. This is much faster than accessing the drives across iCSCI or Fibre Channel protocol links.

Excelero’s scale-out software adds NVMESH storage nodes to an existing set of nodes to manage data growth potentially requiring tens of thousands of nodes. A scale-up offering adds NVMe drives to an existing system, at rack or sub-rack level. Scalability lis imited by the number of drive bays available in the system’s enclosures.

The Edge for Excelero ranges from a smart device through remote and branch offices to a small data centre; – think five to 1,000 servers accessing an array.

NVEdge needs to run on dual X86 controller-based commodity storage arrays with high availability. The software is based in part on open SPDK, and supports SmartNICs such as Mellanox’ BlueField and Broadcom’ Stingray.

It provides:

Thin provisioning up to 1,000x

Support for RDMA and NVMe over TCP/IP networking

Data protection – RAID 10

Checksums

Excelero said OEMs and system integrators will build the systems using Intel and AMD processors. Current partners include Dell, HPE, Lenovo, Quanta, SuperMicro and Western Digital.

An NVEdge array can deliver up to 2.7m IOPS across a 100Gbit/s link using 4K blocks.

Scale-up

According to Excelero co-founder and CEO Lior Gal, the scale-up NVEdge system is comparable to scale-up NVMe-oF systems from AWS-acquired E8,StorCentre’s Vexata, and Pavilion Data Systems. They are all appliances, he says, and Excelero’s advantages include easier deployment and use of standard hardware.

Excelero co-founder and CEO Lior Gal

Appliance vendors with new technology find it difficult to scale their businesses and Excelero, with its scale-out technology is already past that barrier, Gal argued.

He hinted that we might expect NVMESH systems to include NVEdge units in some way.

EXTEN Technologies, the revived Mangstor, has announced its HyperDynamic NVMe-oF array software for use by OEMs and that will compete with NVEdge.

NVEdge is available to select partners immediately and is on show at this week’s 2019 Flash Memory Summit in Santa Clara.

Toshiba has come out with three flash news announcements detailing a range of smaller, denser and speedier drives.

96-layer TLC (3bits/cell) NAND RD500 and RC500 gumstick card SSDs,

Low-latency XL-FLASH media,

XFMEXPRESS fingernail-sized flash card for mobile and embedded device use.

RD500 and RC500

These SSDs use 96-layer 3D NAND, like Western Digital’s SN640 and SN340 announced yesterday. However they are M.2 format drives for gamers (RD500) and mainstream POC (RC500) use.

Both use Toshiba’s 96-layer 3D NAND organised as TLC (3bits/cell) with a faster SLC (1bit/cell) cache. They are connected via the PCIe 3.0/NVMe v1.3c protocol.

The RD500 has 512GB, 1TB and 2TB capacity options while the RC500 has 256BB, 512GB and 1TB capacities. These match Toshiba’s XG6-P (2TB) and XG6 (2576GB, 512GB, 1TB) which are also made with 96-layer TLC flash. The RD500 is faster than the XG6-P.

The performance numbers are:

The XG6-P drives are sold to OEMs for mainstream use while the RC 500 and RD500 are for retail sale; RD500 being targeted at gamers.

The RC500 appears to overlap Toshiba’s XG6 drive, being about the same speed on random IO but much slower on sequential IO, as the XG6 does up to 3.18/2.96 GB/sec for read and write respectively.

Toshiba warrants the RD500 for five years and the RC500 for three, but does not provide total-petabytes-written or drive writes/day numbers. Nor does it provide any prices. They’ll hit the shops in the fourth quarter.

XL-FLASH

Toshiba XL-FLASH is fast, low-latency SLC 3D NAND, like Samsung’s Z-NAND, positioned between ordinary and slower NAND and faster DRAM, equivalent to storage-class memory (SCM) such as Optane (3D XPoint) and Samsung’s Z-NAND.

It was first announced by Toshiba at FMS 2018 and Tosh is now telling us it will be producing 128Gbit dies in a 2-die, 4-die, 8-die package. A die will be sectioned into 16 planes for parallelism, with 4Kbit pages. They will be manufactured using the latest BiCS processes, Toshiba’s 3D NAND technology; that implies 96-layers.

The die will be formatted as SLC (1 bit/cell) and the read latency will be down to 5µs, with Tosh saying this is ten times faster than today’s NAND. An Optane DIMM’s read latency is as low as 0.35 µs.

Scott Nelson, GM of Toshiba Memory America, Inc., issued a quote: “SCM is the next frontier for enterprise storage, and our role as one of the world’s largest flash memory suppliers gives XL-FLASH a cost/performance edge over competing SCM solutions,” such as Optane.

Toshiba will sample its XL-FLASH from September onwards with OEMs likely to ship SSD product in 2020. It suggests XL-FLASH could be designed into industry-standard DIMMs connected to a server’s memory channel.

Target applications are high-speed storage and memory extension, just like Optane. We can expect Optane, XL-FLASH and Z-NAND devices competing in the SCM market in 2020.

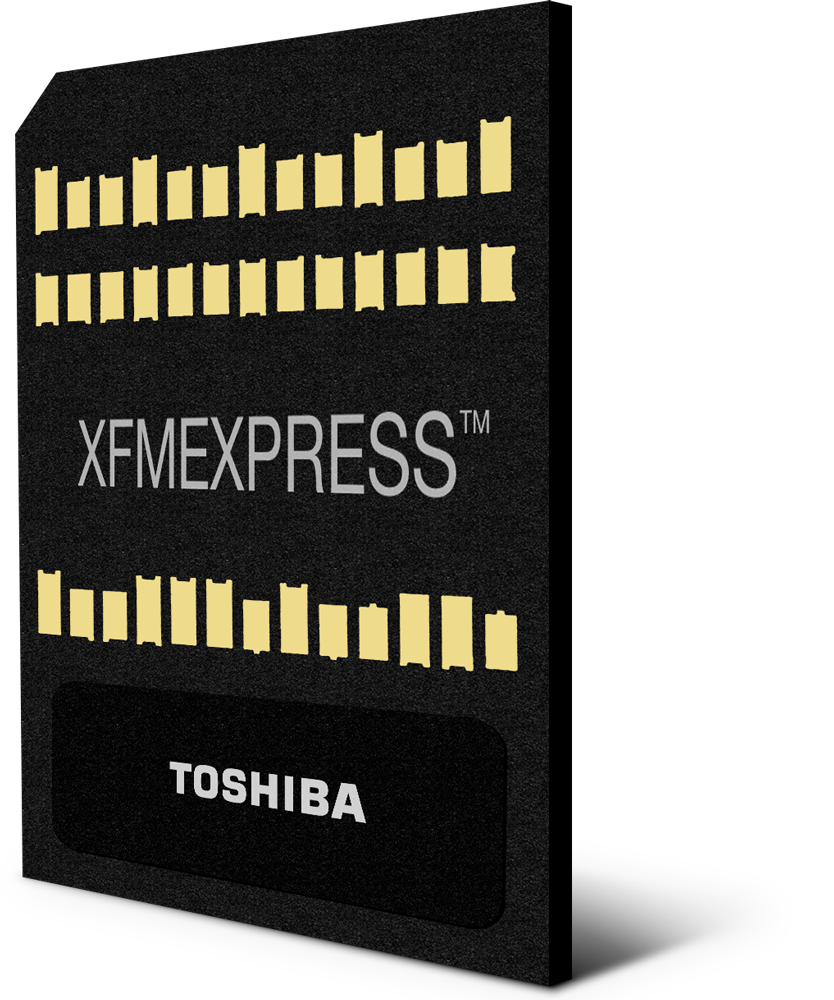

XFMEXPRESS

Toshiba has devised a new format for fingernail-size flash cards and used it to build a NVMe-connected device; the XFMEXPRESS.

The existing microSD format is sized at 15mm x 11mm x 1mm and a WD Purple QD312 device holds between 32GB and 256GB of data, which can be transferred at up to 30MB/sec.

The XFMEXPRESS card is larger at 18mm x 14mm, and it fits in a 1.44mm deep connector slot. It has a proprietary format and uses a fastened hinged connector. That is less removable than a USB stick.

It can transfer data at up to 4GB/sec, across 2 to 4 PCIe 2.0, 3.0 or 4.0 lanes. with a second generation device doubling that to 8GB/sec.

Details of the XFMEXPRESS card’s capacity are non-existent but Toshiba said it can use the latest and future 3D NAND. That means 64-layer, 96-layer and 128-layer technology. We can envisage 512GB-class capacities or possibly greater.

Toshiba said it is for thin and embedded devices like skinny PCs, notebooks, tablets and the like.

Whether Tosh will try and get the format standardised is unsaid. A difficulty is that the SD Association has already proposed a microSD Express standard.

It is slower than Toshiba’s XFMEXPRESS, using a single PCIe 3.1 lane and NVMe v1.3 to enable transfers at up to 985MB/sec; 0.985GB/sec compared to XFMEXPRESS’ 4GB/sec. Adding multi-lane support to microSD Express would nullify Toshiba’s speed advantage.

Fujifilm and Sony have buried the hatchet over a patent dispute that crippled the global supply of LTO-8 tape media.

The two tape media makers have agreed a global patent cross-licensing deal and the US Court of Appeals for the Federal Circuit subsequently dismissed their patent dispute case.

Although neither side are talking in public, the LTO Program Technology Provider Companies (TPCs), – HPE, IBM and Quantum – have announced that Fujifilm and Sony both plan to produce LTO-8 media.

The TPCs are licensees of LTO-8 technology, and they will officially certify media made by Sony and Fujifilm. Global LTO-8 tape media availability is anticipated in the fourth 2019 quarter.

That means customers will get full access to LTO-8 media and its 12TB raw capacity (up to 30TB compressed). Until now they have had to make do with 6TB LTO-7 technology tape, possibly formatted to 9TB via an M8 formatting step in an LTO-8 drive.

Neither Fujifilm nor Sony said anything about their dispute being over. The two tape media manufacturers had been at each other’s legal throats with a flurry of IP lawsuits and US LTO-8 media import bans. This stopped the supply of LTO-8 tape media, rendering LTO-8 tape technology useless.

An anodyne statement of approval was issued by a Quantum senior director, Eric Bassier: “We are pleased to have two licensees for tape solutions allowing us to deliver more product to market, and enabling us to once again provide tape technology solutions, including LTO generation 8, to our partners and end-users.”

Nathan Thompson, founder and CEO of tape systems vendor Spectra Logic, told us by mail: “The IP lawsuits between Sony and Fujifilm have been entirely resolved, globally. Since neither company was producing LTO-8 recently, the TPC will carefully validate both companies products before enabling sales.”

He added: “I don’t know all of the details, but know that both companies were under a lot of pressure from the TPC, end users and market participants like Spectra to resolve the lawsuits. It is my understanding that there is cross licensing on LTO-7, 8 and 9 technologies.”

And, “Spectra is very pleased with the outcome.”

It will take months to fulfil backlogged LTO-8 tape media orders so customers could wait until some time next year to get their cartridges. The succeeding LTO-9 format, with doubled LTO-8 capacity at 24TB raw, is due to arrive in 2020.

Frustrated customers may decide to jump the LTO-8 generation and go straight to LTO-9.

LTO-7 media formatted as type M in LTO-8 drives, will not be readable by LTO-9 drives, adding to the complexity.

Blocks & Files has asked Fujifilm, Sony, and the LTO-8 consortium for comment.

Take a quick dip into our weekly collection of enterprise storage news briefs

Toshiba on the Rocks

Toshiba Memory America has worked on the open source RocksDB to produce its TRocksDB that uses key values more efficiently with SSDs to enable improvements in storage and DRAM usage.

RocksDB takes a log-structured merge-tree (LSM tree) approach to storing data, and rewrites data at least one time for every level of the database, and in many cases, multiple times per level.

The total write amplification for RocksDB will often be greater than 21x, which leads to application-level performance delays and early SSD wear-out.

Toshiba MA has remedied this by storing values and keys in separately managed files. This enables more efficient database lookups, minimises write amplification, and optimises SSD utilisation.

TRocksDB runs on any Linux hardware supported by RocksDB and the server software will soon be available under the terms of Apache2 open-sourced licensing.

EXTEN speeds up NVMe over TCP

EXTEN Technologies has announced the availability of the third generation of its HyperDynamic storage software. It improves TCP performance with Solarflare TCP acceleration that provides TCP performance near RDMA.

V3 adds;

Node level resiliency with synchronous replicas

Shared volumes with replicas for supporting parallel file systems

Dual parity (RAID 6) resiliency

Integrated drive management and hot swap

There is declustered RAID, which provides the ability to simply configure resilient volumes that use standard, Linux multi-path IO software to provide redundancy in networking and storage. Different RAID levels per volume allow flexible, optimised provisioning for separate use cases

The web user interface provides node and cluster level telemetry and the ability to set QoS limits to manage performance during drive or node rebuilds.

2019 Flash Memory Summit

The storage industry’s pre-eminent solid state storage show kicks off in Santa Clara this week and there will be a plethora of announcements and exhibitors. Among them;

Burleywood will talk about its SSD TrueInsight SSD workload profiling analysis software,

DCIG will provide an update on all-flash array developments,

Everspin will display its MRAM products,

Cadence Design Systems is providing DDR4 Design IP (DIP) and Verification IP (VIP) support for Everspin’s 1 Gbit STT-MRAM memory,

Lightbits Labs execs will discuss the state of NVMe/TCP,

Phison Electronics showcases its lineup of PCIe Gen4 SSD controllers,

Dr. Rado Danilak, CEO of Tachyum Inc., will speak about the need for new approaches, and capabilities of data centrer architectures, interconnects, storage and memory types to help artiificial intelligence,

Virtium’s Scott Lawrence, director of business and technology development, will discuss embedded-system designers’ data-security demands and industrial SSDs.

Short items

An Active Archive Alliance report: “Active Archive and the State of the Industry 2019,” highlights data growth challenges facing the storage industry and the expanding role of active archives in the data management lifecycle. Download it with minimal registration here.

Aderas, a systems integrator for US government and commercial customers, is developing an IT platform-as-a-service for its customers, using Private MultiCloud Storage from Madison Cloud powered by StorONE SDS and direct connections to cloud providers at Equinix data centres.

Apple has joined the open source Data Transfer Project to help transfer data to and from its iCloud. Members include Google, Microsoft, Facebook, and Twitter.

IDC has profiled Storage Made Easy, Panzura, and Igneous in an Innovators report on unstructured file and object data content management – IDC Innovators: Unstructured (File and Object) Content Management, 2019 ($2,500(.

FalconStor, a storage software company, has hired David Morris as VP of global product strategy and marketing. He’s a 25-year IT vet with career history at EMC, VMware, Pillar Data, and Huawei .

Intel has canned the gen 2 OmniPath connect project (OPA200) leaving the low-latency 200Gbit/s interface field to Nvidia’s Mellanox. The 100Gbit/s OPA100 Intel product remains.

Kalray’s target controller PCIe cards can be seamlessly configured to support NVMe-over Fabric either over RDMA (“RDMA over Converged Ethernet” or RoCE) or over TCP protocols. The cards can support JBOF/JBOD NVMe-oF target controller functionality.

Kingston is shipping its A2000 NVMePCIe SSD; a single-sided M.2, next-gen entry-level, consumer NVMe PCIe SSD utilising 3D NAND.

Marvell has introduced PCIe Gen 4 4-channel NVMe controllers. The 88SS1321, 88SS1322 and 88SS1323, represent the industry’s first PCIe Gen4 DRAM and DRAM-less SSD controllers to be fabricated on a 12nm process. They support M.2 (22110 to 2230), BGA, EDSFF and U.2 SSD form factors.

Special effects company Whiskytree is buying Panasas ActiveStor parallel access filers to to store and manage its creative computer graphics and visual effects workflows.

The SNIA EMEA Storage Developer Conference (SDC) will return to Tel Aviv in early February 2020.

Tape systems and data protection vendor Spectra Logic is celebrating its 40th anniversary. It announced that TransMedia Dynamics (TMD) has completed client certification of its Mediaflex-UMS Content Supply Chain platform with Spectra’s BlackPearl Converged Storage System.

Storage Made Easy’s new Enterprise File Fabric v1906 release is now available through the Early Access upgrade channel. Features include, faster synchronisation and indexing, a Microsoft OneDrive connector, team folder permission reporting and more.

Toshiba’s KumoScale NVM Express over Fabrics (NVMe-oF) storage software has received an Interop ‘Best of Show’ award in the Server & Storage category.

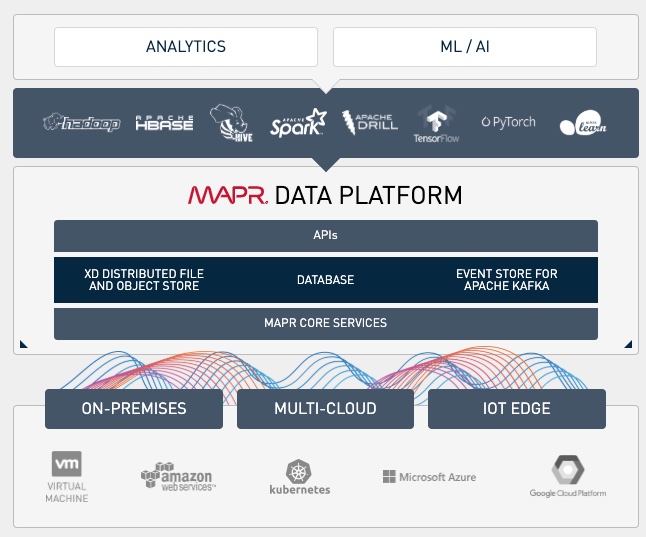

HPE has scooped up the assets of MapR, the doomed Hadoop vendor, for an undisclosed sum.

MapR ran into severe business problems in its first fiscal 2020 quarter, with customer purchases collapsing, and a potential investment round terminated. At the end of May 2019, MapR announced it had two weeks to find an investor or close down. That deadline was extended to July 3.

Since then, radio silence. Until today.

The HPE transaction includes MapR’s technology, intellectual property, and domain expertise in artificial intelligence and machine learning and analytics and data management.The announcement does not mention MapR staff joining HPE.

HPE issued this quote from CEO Antonio Neri: “MapR’s file system technology enables HPE to offer a complete portfolio of products to drive artificial intelligence and analytics applications and strengthens our ability to help customers manage their data assets end to end, from edge to cloud.”

HPE will extend BlueData capabilities for stateful container-based applications with MapR. BlueData was bought by HPE in November last year. Its EPIC Big Data-as-a-service software runs large-scale distributed analytics and machine learning workloads in Docker containers.

By adding MapR technology to BlueData, data scientists and data analysts will be able to stitch together AI/ML and analytics data pipelines in minutes across on-premises, hybrid cloud, and multi-cloud environments.

HPE will add ‘appropriate ‘MapR partners, meaning resellers, ISVs and system integrators, to its partner program.

The good old days

MapR was founded in 2009 by CEO John Schroeder to build a big data analytics business based on Hadoop technology. At its peak the company was valued more than $1bn. Total funding was $280m, collected in seven rounds, with the last raising $56m in September 2017.

The company developed a data platform for artificial intelligence and analytics applications powered by scale-out, multi-cloud and multi-protocol file system technology. The XD Distributed File and Object Store manages both structured and unstructured data.

MapR broadened its software technology to include artificial intelligence and machine learning and added Blockchain and Kubernetes container support. The software runs on-premises or in the AWS and Azure public clouds.

MapR Technologies allows for multiple workloads in the same environment and offers expansive APIs for easy access. It handles a variety of data types from files and streams to documents and multi-cloud and container support.

Comment

With fellow Hadoop analytics big data developer Cloudera also running into problems it is clear that the Hadoop era has run out of growth.

MapR Technologies is a unicorn that crashed to earth. The month-long pause since the July 3 deadline suggests that purchase negotiations for MapR’s business were involved and tortuous.

The lack of comment from MapR executives in HPE’s announcement is telling, and what it’s telling Blocks & Files is that relatively few MapR staff are joining HPE.

The development roadmap for MapR’s Data Platform will now be examined by HPE and, no doubt, re-evaluated.

Western Digital has refreshed its NVMe SSD, composability and storage server products.

The company has added 96-layer 3D NAND data centre drives, almost quadrupling maximum capacity compared to a prior generation with a new ruler format. It has replaced the composable systems F3000 flash drive (aka proprietary SSD) offerings with a similarly specced F3100 drive.

And it has set up a compatibility lab for composable systems and their multi-sourced components. Finally it has added new storage server boxes to the Ultrastar Serv line for OEMs and resellers.

Ultrastar SN640 and SN340

WS has upgraded the Ultrastar DC SN630 drive, a 64-layer 3D NAND TLC (3 bits/cell) product, to the mixed-use SN640 with added M.2 and ruler formats, and the SN340 read-intensive drive. Both use denser 96-layer 3D NAND organised as TLC flash.

The SN640 comes in three formats:

M.2 with 960GB, 1.92TB and 3.84TB capacities,

U.2 with 960GB, 1.92TB, 3.84TB and 7.68TB capacities,

EDSFF E1.L with 7.68TB, 15.36TB and 30.72TB capacity levels.

Western Digital Ultrastar DC SN640 and SN340 drives.

The SN630 topped out at 7.68TB in its U.2-only format.

According to a product brief the performance data for these three drives is up to 3.0/2.0 Gib/sec for sequential reads and writes. The Random read/write IOPS numbers are up to 480,000/2120,000. WD has not revealed the performance numbers for each format type.

It does say in its release that the EDSFF format drive is designed to provide speeds up to 720,000 random read IOPS.

SN640 capacity can be tuned to increase endurance from 0.8 drive writes/day to 2 DWPD. So a 1.92 drive with an 0.8DWPD rating can be increased to 2DWPD by setting the capacity down to 1.6TB.

The SN640 controller features NVMe multi-namespace support, up to 128 of them, and management for zoned drive support.

The drives have Instant secure erase and AES-256-bit encryption. They are sample shipping to potential customers.

SN340

This is a read-optimised drive with 3.84TB or 7.68TB of capacity. Performance is skewed heavily to read work, achieving random read and write IOPS up to 420,000 and just 7,000. Sequential read and write bandwidth is similarly skewed; up to 3.1GiB/s and 1.4GiB/s.

The drive supports just 0.3 DWPD for random writes but up to to 1.2DWPD if all the writes are 32KB-aligned. The SN340 draws 6.5W when operating -better then the prior SN630 read-intensive drive which drew 10.75W.

OpenFlex F3100

Western Digital has refreshed OpenFlex with an F3100 flash drive replacing last year’s F3000. Both are NVMe-over-Fabrics-connected ruler-like format drives, like a longer version of a 3.5-inch drive as an illustration of the device on an E3000 chassis makes clear:

E3000 chassis. The E3000 can hold 10 x F31000 drives.

OpenFlex products are part of WD’s composable systems infrastructure, whereby compute, storage and networking are disaggregated from fixed configuration servers and placed in resource pools. From there, portions can be dynamically composed or configured into server systems for particular workloads.

WD is competing with vendors such as Dell EMC, DriveScale, HPE and Liqid in the composable systems market.

The OpenFlex F3100 holds 61TB, like the F3000 and does up to 11.7GB/sec. The F3000 was rated by WD at 12GB/sec; the same within decimal rounding limits. The F3100 is said to deliver up to 2.1m IOPS with a latency of less than 48μs, making it the fastest NVMe-oF open composable storage platform, WD claims.

Our working assumption is that WD’s F3100 is a sped-up F3000 – we have no IOPS and latency numbers for the prior F3000. We don’t have any information about the type of flash in the F3100 or how it is organised to make a 61TB device.

Blocks & Files notes the SN640 EDSFF ruler drive holds up to 30.7TB and it is tempting to think of the F3100, with its 61TB capacity, as a pair of SN640 rulers in a single case.

Composable Compliance Lab

WD has also set up a compliance lab, along with partners, for its composable system. It calls this an open composable ecosystem, as away of contrasting the competition – which includes Dell EMC, HPE and Liqid.

The lab will test and validate end-to-end interoperability between OpenFlex components, using the Open Composability API for example, from different suppliers, such as Broadcom, DriveScale, Edeticom. Kaminario, Mellanox and Xilinx.

Storage servers

WD has added new Serv24 storage servers, intended as building blocks for software-defined storage (SDS), hyperconverged infrastructure (HCI) and edge environments. Edge encompasses remote and branch offices, video surveillance, and IoT edge environments.

The Serv24-4N is a 4-node, all-flash, NVMe drive system for HCI use with a 2U chassis. Each node has two Xeon SP CPUs, 24 PCIe lanes to six SSDs, and 3 x 16 lane PCIe slots. The maximum raw capacity is 184TB.

The Serv24+6 is a hybrid flash and disk system inside a 2U chassis, slated for SDS and edge use. It has 24 front-mounted drive bays and 4 disk drive bays in the rear. Disks can use SAS or SATA interfaces. The maximum capacity is 420TB.

Western Digital’s release says the Serv24+6 also has “up to six NVMe SSDs in the rear bays for a data-acceleration tier to improve application performance.”

These two join the Serve24 24-slot NVMe drive system, a Serve24 high-availability system and a Serv60+8 hybrid flash and disk server in a 4U cabinet.

More information and availability

Get an F3100 datasheet here. You can download an SN340 and SN640 product briefs. The DC SN640 and 340 are sample shipping to prospective customers.

The Ultrastar Serv24-4N will be available this quarter. The Ultrastar Serv24+6 is sampling now and will be available in volume by September. There is no product brief or datasheet information available for either one of these systems.

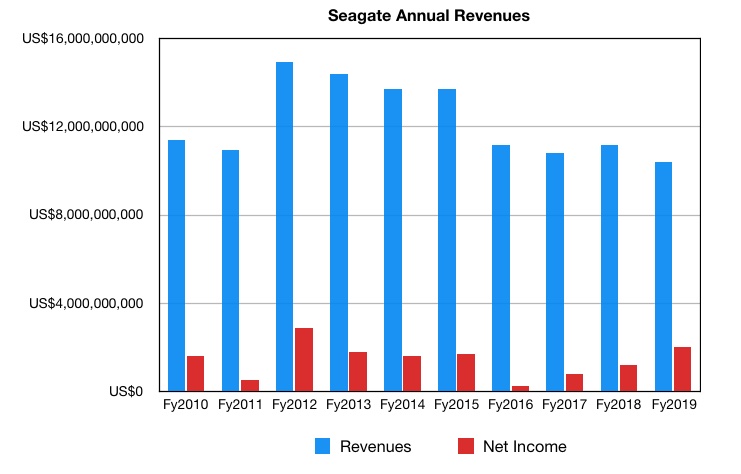

Seagate successfully squeezed out cash from its disk drive business in its latest quarter despite long-term revenue decline, and with little or no help from enterprise arrays and SSDs.

Seagate’s fourth fy2019 quarter revenues were 5.4 per cent down annually at $2.37bn, but above the mid-point of its guidance, keeping the analysts happy. Net income was up a humungous 113 per cent to $983m, largely due to a one-time $702m tax benefit. Taking that away profits would have been $281m, 39 per cent lower than a year ago.

Full fy2019 revenues for Seagate were $10.4bn, 6.3 per cent less than a year ago. Net income for the year was $2bn ($1.8bn) recorded last year. If we take away the Q4 one-time tax benefit again, then full year profits were $1.31bn.

Cashflow from operations in the quarter was $448m and free cashflow was $297m. For the full year cashflow from operations was $1.8bn and free cash flow was $1.2bn.

CEO Dave Mosley said in as statement: “We continued to execute well in the June quarter in the midst of an uncertain global environment. We once again delivered on all of our financial expectations, while driving higher operating profit and earnings per share quarter-over-quarter, and demonstrating our ongoing focus on optimizing free cash flow,”

He said global industry conditions were starting to improve, particularly among cloud and hyperscale customers. Seagate expects to make revenues of $2.55bn plus or minus 5 per cent in the next quarter, 14.7 per cent down on $2.99bn last year.

The long view

Looking at the past seven years, Seagate is getting smaller. Revenues have shrunk 30.4 per cent from $14.94bn in fy2012 to $10.4bn in fy2019.

The disk drive business’ revenues have remained more or less flat over the 2016-2019 period.

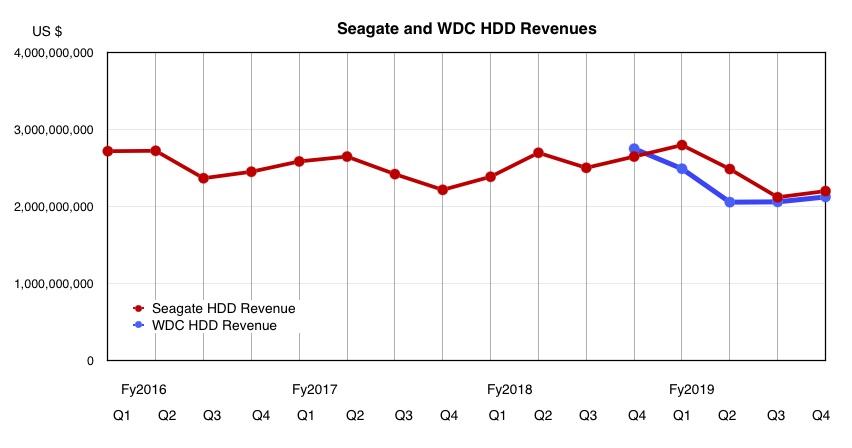

It is now the largest disk drive manufacturer by revenues.

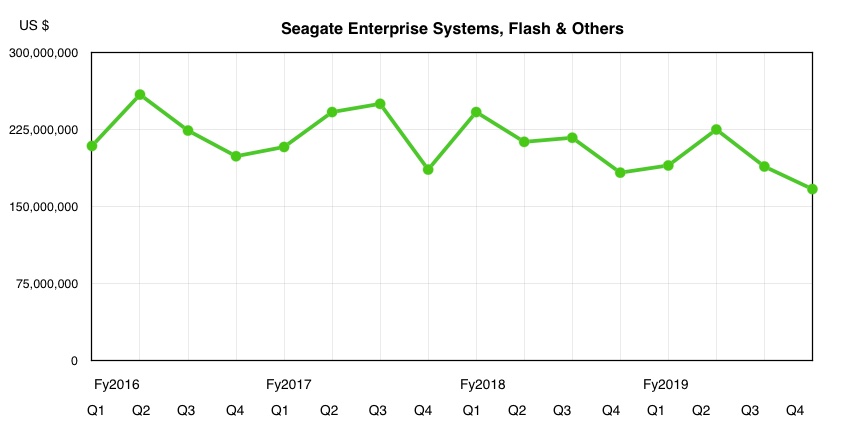

(Figures supplied by Aaron Rakers, a senior analyst at Wells Fargo)

The chart above shows Seagate’s HDD revenues since fy2016 and for comparison includes WD’s five most recent quarters of digital disk revenues. Seagate’s lead in HDD revenues has persisted for four quarters although it is currently slim.

The company’s forays into enterprise arrays and flash memory are not doing so well, with revenues trending down from $209m in the first fy2016 quarter to $167m in the latest quarter.

In comparison Western Digital earned $1.5bn from flash-based products in the quarter.

Seagate focus

Seagate generates tremendous amounts of cash, much used for dividends and share buybacks. The company is content to spin cash from disk drives, believing there is a long-term future in capacity-optimised drives for enterprise data centres, cloud service providers and other hyperscale customers, and the surveillance business.

Disks are pretty much everything for Seagate. The enterprise systems (storage arrays) and flash business represents just seven per cent of revenues.

Western Digital has invested to become a significant integrated NAND and SSD supplier, and is now investing again to build a storage array business. Seagate by contrast is wedded to the hard disk drive business.

Blocks & Files thinks we might even see the company offload its enterprise systems and flash businesses. If it can do better with dollars invested in making disks rather than arrays and SSDs, then it may decide to concentrate everything on disk drives and spin off the array and SSD distractions.

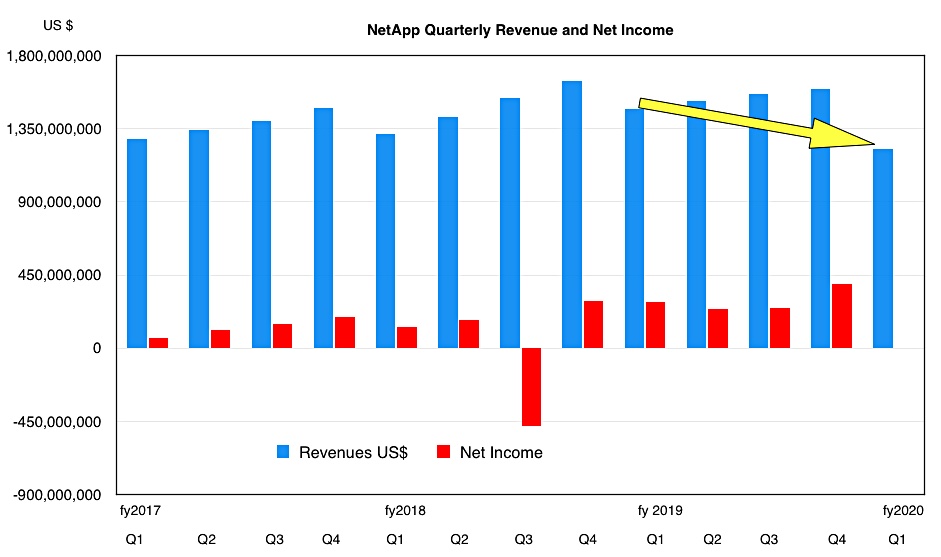

NetApp expects a big revenue miss in the first 2020 quarter due to large global accounts spending less in response to the US-China trade dispute and other macroeconomic uncertainties.

The company has also suffered self-inflicted harm because some of its North America sales teams failed to win enough new accounts to offset dependency on large global accounts.

The preliminary calculation is for revenues between $1.22bn and $1.23bn, down 17 per cent y/y on previous guidance.

Full fy2020 revenues are now expected to fall between 5 and 10 per cent y/y, again below previous guidance. Fy2019 revenues were $6.146bn and the company had expected fy2020 revenues to grow in the low mid-single-digits.

The company had anticipated a revenue range of $1.315bn to $1.465bn in the current quarter. A year ago first fiscal 2019 revenues included $90m from enterprise software license agreements (ELAs) which did not repeat in the current quarter. That accounts for 12 points of the 17 per cent drop.

In a statement, CEO George Kurian said: “We believe we can return to growth over time by prudently reallocating investments to expand sales coverage and accelerate our participation in the growing Private Cloud and Cloud Data Services markets.”

Storage slowdown

NetApp ran a conference call yesterday to discuss the Q1 revenue downgrade.

Kurian said: “In summary, our shortfall was primarily due to lower IT hardware spending related to macro concerns at our largest customers, and to a lesser extent execution issues in the Americas.”

“I think that the macro was about two-thirds of the miss. Factors that we could have controlled is probably one-third of the miss.“

The miss became apparent in the second half of the quarter with deal closures getting pushed out and a small proportion of deals cancelled. However, NetApp public sector revenues in APAC, Europe and US were mostly on track.

Kurian revealed: “This weakness was contained to our storage business. Both Private Cloud and Cloud Data Services grew year over year in Q1, but there’s still a small part of our business and not yet able to offset the slowdown in storage.”

Private cloud refers to object storage and hyperconverged systems. The slowdown in storage spending was part-evidenced by lack of traditional hardware refresh cycles in NetApp’s customer base. NetApp’s mid-range storage will be under further pressure when Dell-EMC releases its MidRange.NEXT refresh later this year.

China woes

The China-US trade dispute was an important factor. Kurian said: “Two of our largest customers that were impacted by the China dispute, shrank their capital spending by 30 per cent year on year and that has meaningful consequences even to IT hardware spending.“

NetApp can’t fix the macro-environment but it can recruit more new account-chasing sales reps. However, “it typically takes three to four quarters for a sales rep to be onboard and fully productive,” Kurian said. “We have been hiring some amount of reps even in Q1, right? So, it’s not like we’ve done nothing over the last quarter, quarter-and-a-half.”

Also NetApp will more aggressively attack Private Cloud and Cloud Data Services opportunities.

Kurian said the fundamental fix would be to remedy the macro uncertainties. “To improve the overall capital spending environment, we need to see certainty, certainty on trade policy, certainty on the economic outlook. That has caused a spending pause in some of the largest global accounts that are most exposed to it.”

He emphasised that NetApp wasn’t losing out to competitors; there was no decline in in rates and product gross margins remained strong.

In that case other storage suppliers to large enterprises should experience the same slowdown effect; meaning Dell-EMC, Hitachi Vantara, HPE, IBM, Nutanix and Pure Storage. Their revenue expectations may get Trumped as well.

In June 2019 the company bought Retrospect, a backup software vendor with half a million customers but skinny revenues, and the following month it bought Vexata, an ailing enterprise NVMe array startup. Prices were undisclosed but it is safe to assume that Vexata shareholders took a big hair cut.

A pattern is emerging here. StorCentric is about buying struggling companies and making them healthy. StorCentric’s investors are in it for the long term, Shah said. “It’s not about squeezing cost, cutting it, and finding a home for it – not churn and burn.”

In a phone interview with Blocks & Files, Shah characterised StorCentric’s acquisitions as “very good technology of high quality that hasn’t been able to liberate itself”. The previous owners had “not listened to the customer”.

He is on a mission to find such technologies and aims to build StorCentric into “the next world-class storage company”, with products for the entire bit lifecycle.

The big vendors focus on $30m-per-year customers and “forget about everyone else,” according to Shah.

He has identified a gap in the market where “customers are frustrated with big vendors” because they push forklift upgrades and jack-up maintenance prices on older products if customers don’t upgrade.

StorCentric will focus on selling affordable products to the everyone elses, said Shah. Things that just work.

The history boys

StorCentric’s roots extend back to Drobo and Nexsan. Drobo set up in 2005 to make consumer storage that wouldn’t lose data. In 2013 it was joined with Connected Data in a transaction process called “merging into” rather than a straightforward acquisition and had never been profitable.

Connected Data set Drobo up as a standalone business in May 2015, with Mihir Shah brought in as a turnaround CEO.

His background included a corporate development position at IBM in 2004-2009 – he was part of the team that handled the XIV all-flash array acquisition in 2008. He joined Drobo from Bluefin, an IT support company, where he was CEO.

Imation bought Connected Data in October 2015.

Over at Nexsan, Gary Watson was its co-founder and one-time CEO. The company made primary data and archival storage arrays and was bought by Imation in January 2013. The idea was that Imation could grow the storage array business while its tape and optical media businesses were declining. Buying Connected Data was part of the overall strategy.

It didn’t pan out, and Nexsan and Connected Data were spun out to private equity in January 2017 as part of Imation’s restructuring under activist investor control.

The private equity people set up the combined Nexsan and Drobo businesses as StorCentric in 2018, headquartered in Sunnyvale, CA. Shah was appointed as its CEO and there was a core team of a dozen or so. He ran Nexsan and Drobo as separate business units. Watson left Nexsan in March 2019, leaving Shah to run the show. The company then bought Retrospect and Vexata.

StorCentric foursome

Today StorCentric’s four storage properties are organised into four independent, wholly-owned business units.

We can characterise the four as hardware or software, and small, medium or large enterprise, using a 6-box diagram:

Vexata is available as storage software. Question marks indicate Blocks & Files notion of technology acquisition areas

Technology development

StorCentric does not intend to have a central and unified engineering team – and the four business units will develop their own technology.

“We will build on the brands and they will go distinctively to their market segments. A Drobo customer is unlikely to buy a Vexata box,” Shah said.

Technologies could be imported from one to another though, such as Vexata taking on board Nexsan replication.

Shah did say Nexsan and Vexata fit together. One impetus for the Vexata purchase was that Nexsan customers were asking for NVMe storage. Another line of thinking is that Nexsan and Retrospect represent tier 2 storage, while Vexata takes StorCentric into tier 1 storage.

What next? Surya Varanasi, co-founder and CTO of Vexata, is developing a technology roadmap for StorCentric. Shah didn’t expand on that, apart from saying two new Drobo products are due in the next six months and a Drobo+Retrospect backup appliance is being considered.

Blocks & Files envisages StorCentric making more acquisitions. We think some kind of cloud storage gateway functionality might be on its radar, but Shah declined to give us any clues.

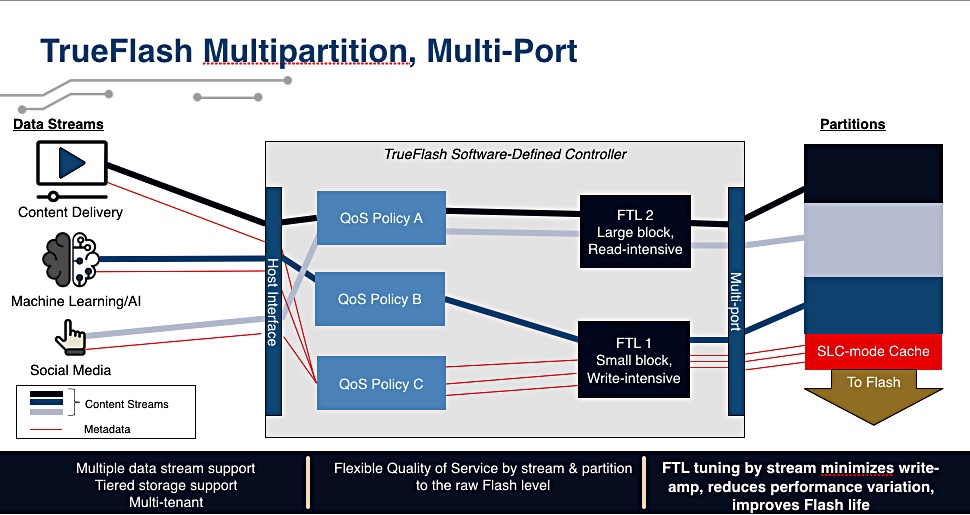

Flash storage software startup Burlywood has introduced an analysis service for SSDs that profiles their production workload in order to tune operations.

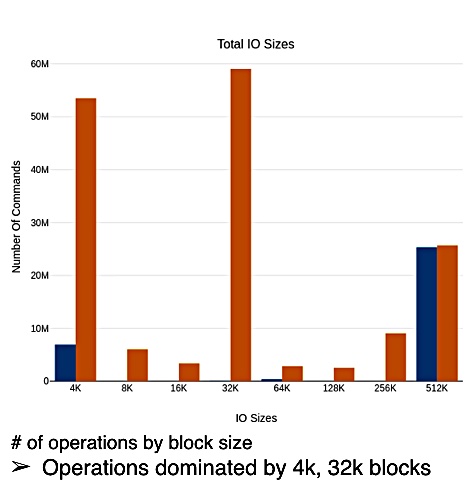

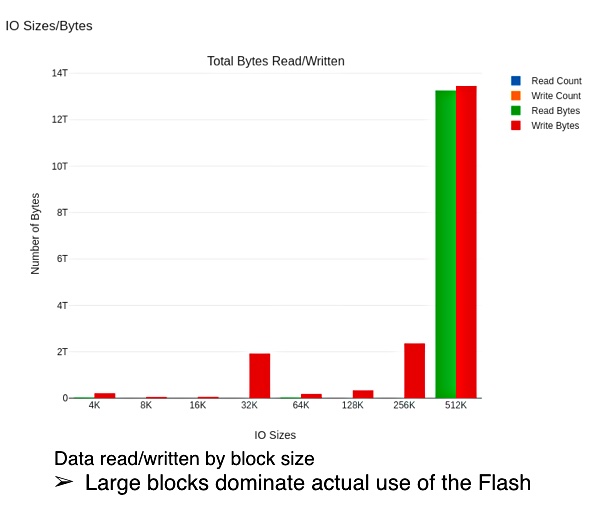

Customer workloads differ by read/write mix, IO sizes, and logical block addresses. Workloads can be viewed as generating data streams for SSDs, and each identifiable data stream type ideally needs its own customised SSD to handle it most efficiently. According to Burleywood, an SSD that matches one workload is less efficient dealing with others.

Burlywood gives an SSD controller multiple flash translation layers (FTL). This software maps incoming datastream data addresses to the data blocks in the SSD. It supports wear-levelling and other SSD performance and endurance-focused processes in the drive.

Different FTLs are used for datastreams with different profiles to enable the SSD to fine-tune performance.

This depends upon Burleywood’s TrueFlash Insight service which installs software in SSDs to record IO telemetry over hours or days. The data is sent to Burlywood and analysed to profile the workload hitting the SSDs. Burlywood service reps can help a customer with the telemetry focus and gathering.

Example Burlywood TrueInsight telemetry capture.

The analysis reveals the characteristics of the incoming datastreams and identifies any different types; read-intensive or write intensive; exhibits a degree of logical block address locality, block size distribution, etc.

Second example of TrueInsight telemetry capture.

Where there are separated datastream types the Burlywood SSD controller is installed with multiple FTLs. A driver recognises incoming IO types and sends them to the right FTL. In effect a single SSD is partitioned or virtualized into several concurrent SSDs matched to the incoming datastream types.

Currently Burlywood supports relatively low capacity SATA and NVMe interface SSDs. It is developing support for two types of NVME SSDs with much higher capacities.

Burlywood said its SSDs are suited for cloud service providers and hyperscale users who need to extract more performance and endurance than commodity drives can provide

At time of publication, we have not seen example data showing drive performance before and after customisation through TrueInsight.

Blocks & Files suggests Burlywood might develop the technology to automatically profile the workload datastream, with data sent to a SaaS-based analysis service, and SSD controller alteration recommendations sent to the customer direct for examination and subsequent installation.

This would enable the SSDs to cope with workloads that change over time.