In-drive SSD compression bumps up over-provisioning capacity, reduces write amplification and extends endurance – how long the SSD lasts under warranty before wearing out.

The utility of data compression is strengthened with QLC (quad level) NAND flash drives which made their market debut in May this year. They have 33 per cent greater capacity than today’s TLC triple cell flash but endurance and performance is worse. This is because reading and writing the extra bit per cell is slower and wears out the drive more quickly.

So says Seagate which notes its Nytro 1551 TLC SSD drive compresses the data it stores.

In a presentation at last month’s 2019 Flash Memory Summit, Seagate managing technologist Erich Haratsch said the Nytro 1551 SSD’s compression algorithm is lossless and runs inline at full data rate in the drive’s flash translation layer (FTL).

The impact on read and write latencies is unquantified but low. However, less data after compression means the SSD writes less and therefore write performance improves.

Write amplification

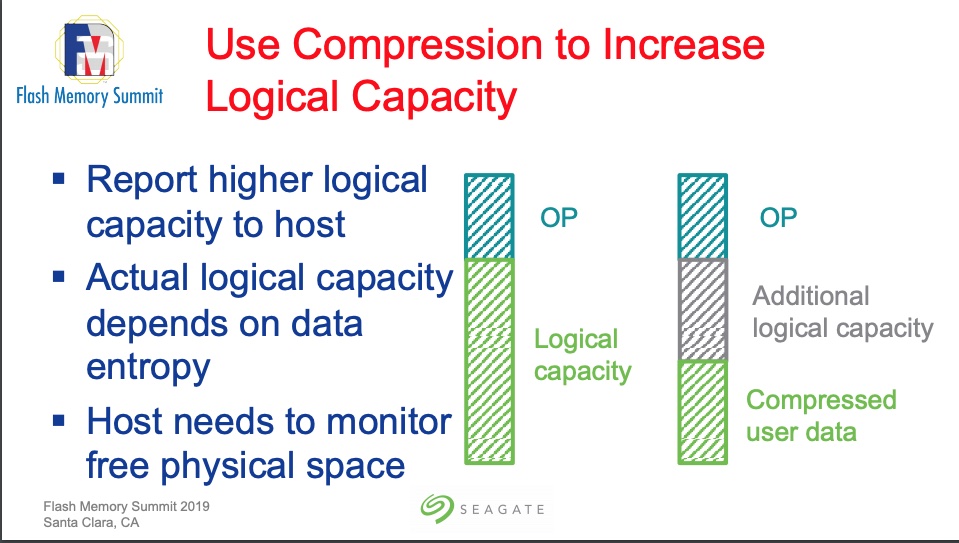

A traditional FTL writes data in chunks with equal physical sizes that fit into a flash page. After compression the data chunks are varying sizes and the FTL has to write these to the media.

With random write workloads, write amplification – an SSD’s extra writes due to its internal processes – increases as over-provisioning decreases.

Slide from Seagate FMS 2019 presentation

For example, take a 12TB SSD, with 1TB over-provisioning – space set aside for use when flash cells wear out – and write 12TB of data to it. This data is compressed by 25 per cent, with only 9TB actually written, leaving 3TB of empty space. In effect the drive’s over-provisioning capacity has risen to 4TB.

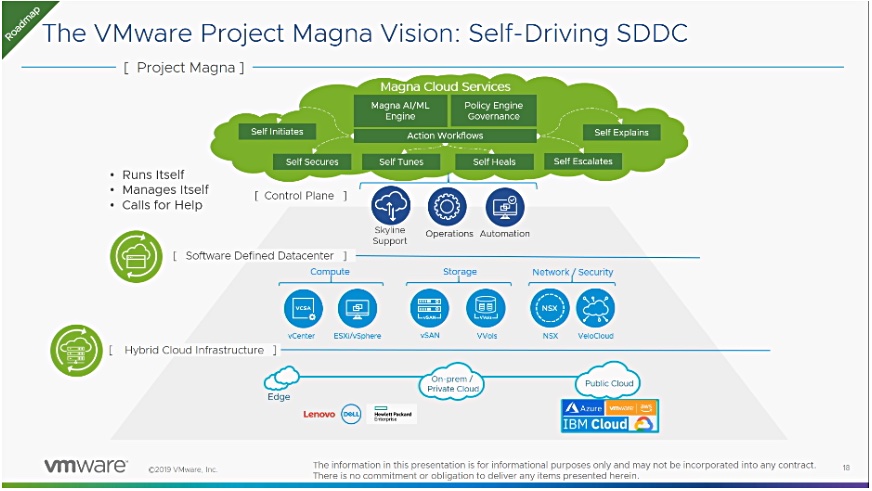

VMware is developing a cloud service to monitor software in customer deployments and tune it automatically to improve performance. This is Project Magna and its first target is vSAN in hyperconverged infrastructure.

It will work like this: customers select their key performance indicator – read or write optimisation or both. Magna examines their vSAN environment and compares it to the KPI average for stored and monitored deployments. If the site is below average, Magna changes it to bring it closer to the average.

When switched on via vRealize Operations (vROps), Magna Cloud Services records data from the deployed vSAN system and uploads it to a VMware data store, where it is analysed. A machine learning engine inside Magna identifies and implements performance tweaks.

vROPs displays the before and after state graphically so customers can see if performance has improved. VMware’s Project Magna people have yet to decide the intervals for system monitoring.

Reinforcement learning

Magna incorporates a reinforcement learning system that seeks so-called rewards. Magna looks at its own performance actions and strengthens those that boost customer vSAN performance

A VMware blog says: “Reinforcement Learning combs through your data and runs thousands of scenarios that searches for the best reward output based on trial and error on the Magna SaaS analytics engine. And this is automatically and continuously done across your vSAN clusters to ensure it’s always using the best settings to maximize throughput and minimize latency of your … hyperconverged infrastructure.”

Magna is also designed so that it does no any harm to systems it monitors, the blog states: “There are guard rails within the ML algorithms that will not decrease performance by any means.”

Project Magna is intended for all VMware’s software-defined data centre components covering compute, storage, network and security. These are vCenter, ESXi/vSphere, vSAN, VVols, NSX and Velo Cloud.

Magna is in tech preview and VMware has not committed to introducing it to a specific version of vSphere.

Cormac Hogan, a senior engineer at VMware, provides a more detailed introduction to VMware’s Project Magna and gives pointers for further reading.

A couple of weeks ago Apeiron and its VC backer trumpeted a global OEM deal with HPE. There is less to this than meets the eye.

Making its debut in August 2017, Apeiron’s ADS1000 system can use Optane SSDs and delivers superfast performance, according to benchmark tests performed by ESG, an IT analyst firm. The Apeiron Data Fabric uses NVMe over Ethernet in a proprietary way and requires Altera FPGA-boosted HBAs and 40Gbit/s Ethernet switches.

President and CEO Chuck Smith came on board in January this year. He is an 18-year HPE veteran and, possibly coincidentally, Apeiron announced the global OEM partner deal with HPE in July. This see the ADS1000 integrated with ProLiant DL360 Gen10 servers. Apeiron gets to take advantage of HPE’s global reach, manufacturing capability and support. It does not mean that HPE sales will sell the integrated HPE/Aperion kit. In effect, HPE will build it and deliver it when Apeiron’s channel sell it.

VC Impact Venture Partners, called Apeiron one of its portfolio companies, when it announced the HPE OEM deal with a tweet;

Apeiron is one of many NVME-oF startups. Will it make the cut? The company appears to be tiny and funding is opaque. Certainly the operation is lean, with no heads of operations, sales, marketing or finance listed on its website or LinkedIn. There’s no PR agency and LinkedIn lists only 14 employees. CFO Rebecca Freeman left in May and sales veep Jim Steed left this month for a sales director role at Nutanix.

We sent questions to Apeiron last week and will update this story if and when it replies.

Toshiba Memory Holdings Corp. is buying LITE-ON’s SSD business for $165m.

Nobuo Hayasaka, acting CEO of Toshiba Memory Holding Corp., released a prepared quote: “LITE-ON’s Solid State Drive business is a natural and strategic fit with Toshiba Memory and expands our focus in the SSD industry. This is an exciting acquisition for us, as it positions us to meet the projected growth in demand for SSDs in PCs and data centres being driven by the increased use of cloud services.”

LITE-ON is a Taiwan-based business supplying optoelectronics, storage, semiconductors and other devices. The company set up its LITE-ON Storage SBG SSD business in 2008 and designs, develops and makes SSDs in-house. The company uses Toshiba 96-layer flash in its EP4 PCIe SSD.

In May this year LITE-ON ranked third worldwide for PCIe SSD revenues as of the first quarter of 2019, as reported by Forward Insights.

Toshiba will own the LITE-ON SSD brands, operations, assets including equipment, workers, intellectual property, technology, client and supplier relationships and inventories, and gets access to its channels. These include LITE-ON’s relationships with PC suppliers such as Dell.

China syndrome

In January 2018 Anandtech reported that LITE-ON had signed a joint-venture deal with Tsinghua Unigroup to develop and build SSDs in Suzhou, China. The JV plant was planned for completion by the end of 2018. It seems reasonable to infer that Toshiba will get ownership of LITE-ON’s 45 per cent interest in this JV.

The JV, which was to start producing chips in the last quarter of 2018, would provide a separate source of NAND wafers for Toshiba, independent from its JV with Western Digital. Toshiba would also be able to bring modern 64-, 96- and 128-layer 3D NAND technology and fabrication expertise to the venture with Tsinghua Unigroup.

The deal would also bring access to the domestic Chinese market to Toshiba.

IPO and closure

Toshiba Memory Holdings’ IPO is now expected to take place in the first half of 2020. Timing has been delayed by Toshiba experiencing low NAND chip demand due to the US-China trade dispute.

Data protector Acronis has introduced a set of cyber services offering a combination of security risk assessments, vulnerability assessments, penetration testing, incident response services and awareness training. They are customised based on an individual’s role.

According to Serguei Beloussov, Acronis CEO, cyber threat assessments, best practices and preparedness training have been too costly and complex for anyone other than large enterprises to implement. But now “with the launch of Acronis Cyber Services, we’re making enterprise-grade cyber protection solutions more accessible so every organisation can have the easy, efficient and secure cyber protection that’s needed today.”

Pay attention to the Buffalo

Buffalo EU has introduced the TeraStation 6000 NAS range for small and medium businesses. This is fitted with 8GB ECC memory and a 1.5GHz Intel Atom C3338 processor for the 6200N 2-bay desktop version and a 2.1GHz Intel Atom C3538 CPU for the 4-bay desktop (6400DN) and rackmount (6400RN) designs. It has storage options from 4TB to 32TB, a 10 GbitE network port and two 1 GbitE ports.

TeraStation 6000 NAS range.

It has Snapshot and iSCSI Volume Backup features. Snapshot takes images of the current data and creates restore points at fixed intervals. Backed up data is stored incrementally and in block units, so that each Snapshot captures the difference from the previous one, instead of backing up full data each time. This results in an efficient use of storage space and allows for a high backup frequency.

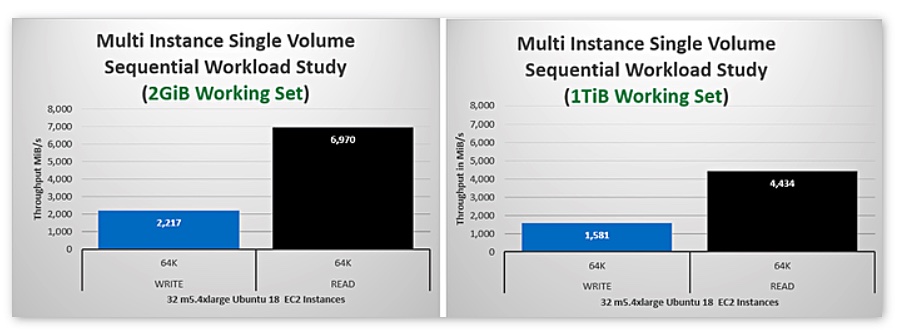

Cloud Volumes ONTAP is the ONTAP storage service running in AWS and Azure. The blog says NetApp, using FIO, saw up to 4,500MiB/s of sequential reads or 470,000 random read IOPS with a single cloud volume. It also reports up to 1,700MiB/s of sequential reads or 220,000 random read IOPS from a single EC2 instance.

The company used two separate sets of data, in its tests. One was a small 2GiB set to demonstrate theoretical maximums. The other was a larger 1TiB working set which caused IOs to traverse the entire storage subsystem, rather than rely upon data resident in storage memory.

Shorts

Secondary storage hyperconverger Cohesity announced its DataProtect and DataPlatform products have gained VMware Partner Ready for VMware Cloud on AWS validation. With Cohesity, customers can back up and recover virtual machines (VMs) running on VMware Cloud on AWS. After completing an initial backup, users can archive VM backups to Amazon S3 and Amazon Glacier for long-term retention.

A 2019 Digital Storage for Media and Entertainment Report, from Coughlin Associates, provides 253 pages of in-depth analysis of the role of digital storage in all aspects of professional media and entertainment. Projections are given out to 2024 for digital storage demand in content capture, post-production, content distribution and content archiving are provided in 63 tables and 128 figures.

Analyst house ESG has a released a Technical Validation report looking at Dell EMC’s VxRail with Xeon Scalable Processors and Optane SSDs. The report states: “ESG testing validated that Dell EMC VxRail with Intel Optane SSDs provides the high performance and low latency that business-critical, virtualized workloads demand. The consistency of performance over time was particularly notable.”

Igneous, an UDMaaS (Unstructured Data Management as a Service) startup, has used some its March $25m VC round to hire Mike O’Brien as chief revenue officer. His resume includes CEO roles and time spent at Dynatrace and Microsoft.

Microsoft wants to bring exFAT file system for SD cards and flash drives to the Linux Kernel. Read more in our sister publication The Register.

Paragon Software has released an updated Microsoft exFAT by Paragon Software driver with transparent read and write access to exFAT volumes from Linux, with additional performance optimisation for modern Linux kernels and lower CPU memory consumption.

Startup StorOnesays TechData will be marketing its Storage-as-a-Service product, which uses Dell PowerEdge servers. It has achieved a total of fifty customers and a OEM partnership with an HCI supplier is likely to happen. StorONE also has a partnership with IBM concerned with small and medium business customers.

Prodigy Universal Processor developer Tachyum has joined the Compute Express Link (CXL) Consortium. CXL is a high-speed CPU-to-Device and CPU-to-Memory interconnect that offers high-bandwidth, low-latency connectivity between host processors, systems and devices, such as FPGAs, intelligent networking and storage accelerators, memory buffers, storage class memory and smart I/O devices. It joins CXL founders Alibaba, Cisco, Dell EMC, Facebook, Google, Hewlett Packard Enterprise, Huawei, Intel Corporation and Microsoft plus processor manufacturers AMD, ARM, and NVIDIA, as joint-CXL consortium members.

Pure Storage could spring a 4-bit flash surprise on the industry next month, and attack nearline disk storage boxes.

This week, Aaron Rakers, a senior analyst for Wells Fargo, hosted investor meetings with Pure Storage’s chief architect Rob Lee and Matt Danziger, head of investor relations.

Pure did not discuss its product roadmap in the meetings but Rakers told subscribers: “We believe Pure could intro’ QLC NAND support for their arrays at the upcoming Pure//Accelerateend user conference in mid-Sept.”

He thinks Pure will use ”QLC to expand its TAM (total addressable market) into workloads that are not currently addressed – e.g. opportunities in second-tier storage applications; deepening encroachment vs. 7200 rpm enterprise HDDs.”

Blocks & Files thinks Pure Storage QLC array will spark mainstream QLC flash adoption by the storage industry.

QLC SSDs are here. QLC arrays should follow

In May 2018 Pure Storage said the Flash Array //X system was ready to support storage-class memory (SCM) and QLC flash.

Pure Storage debuted the FlashBlade in 2016, making it pretty much the first all-flash array vendor to bring out a flash box for unstructured data workloads. Now it could be among the first to bring out a QLC (4bits/cell) flash box and use it for secondary data, attacking nearline 7,200rpm disk drive boxes.

Nearline or secondary data storage is dominated by disk drive arrays using 8TB-16TB hard disk drives spinning at 7,200rpm. Current TLC (3bits/cell) flash SSDs are too expensive for this workload, costing 10X – 20x more per TB than disk.

However, QLC flash changes the price differential . This adds another bit to TLC flash cells, increasing capacity by a third and lowering the $/TB cost.

Storage array costs could go down with the use of QLC flash, opening up the general nearline storage array market to flash boxes.

Startup VAST Data introduced the first QLC flash-based array in February 2019 but they do not feature in mainstream enterprise storage array product lines.

That could soon change.

Blocks & Files believes Western Digital could also introduce a QLC flash tier in its 2-tier IntelliFlash arrays and Toshiba could use QLC NAND in its partner-built KumoScale arrays.

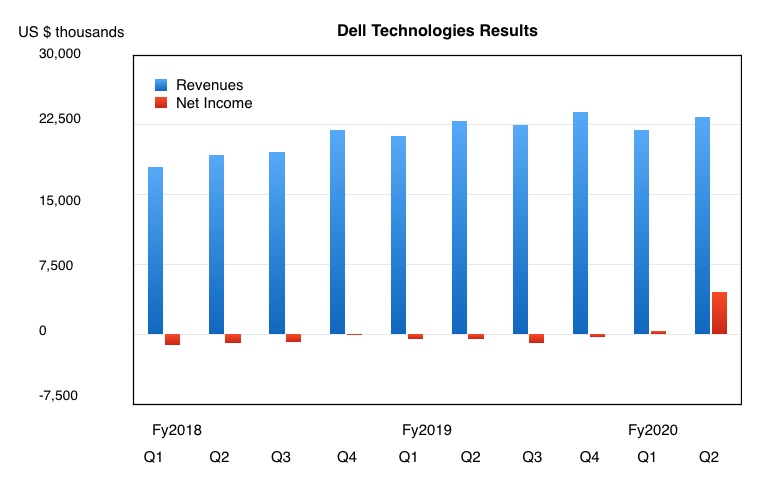

Dell Technologies pulled in £23.4bn revenues in the second fiscal 2020 quarter, up 2 per cent, and eked a massive $4.5bn profit, thanks to an income tax provision.

In a statement Jeff Clarke, Dell Technologies vice chairman, said: “We are in the early stages of a technology-led investment cycle. IT spending remains healthy and our business drivers remain strong.”

No macroeconomic enterprise buying slowdown here – yet, so take that, HPE and NetApp.

Wells Fargo senior analyst Aaron Rakers pointed out Dell experienced “softer enterprise IT demand, though orders, ex-China, grew +4 per cent Y/Y.”

Analyst Patrick Moorhead of Moor Insights and Strategy, said: “Any growth in enterprise spend was good in this environment.” Yes, there was a “12 per cent decrease in servers and networking. [But] competitively, many companies were down so I’m not concerned. Overall storage was flat, but judging by the NetApp train wreck and Dell’s growth in all-flash, the company may have increased overall storage unit market share.”

Some headline numbers:

Cash flow from operations – $3.3bn

Cash and investments balance – $10bn

Diluted EPS – $4.83

$2.0bn of gross debt paid down in Q2 ($2.4bn year to date)

$17.0bn of gross debt paid since the EMC merger – leaving $36.4bn gross coredebt.

CFO Tom Sweet said: “Operating income, gross margin and deferred revenue are up double digits, our PC business produced record results, and we saw record cash flow.” He also mentioned “growing operating income and EPS faster than revenue”.

Turning to that outrageous profit; Dell made a loss before income tax of $111m and then along comes a negative $4.62bn income tax benefit and, hey presto, we have a $4.5bn profit. Without that there would have been a loss.

Segment strengths

The main Dell businesses are:

Infrastructure Solutions Group (ISG) – revenues dipped 7 per cent to $8.6bn

Client Solutions Group (CSG) – PC revenues grew 6 per cent to a record $11.7bn

VMware – revenues rose 12 per cent to $2.5bn

Other businesses (Pivotal, Secureworks, RSA, virtustream, Boomi) saw $619m revenues up 8 per cent.

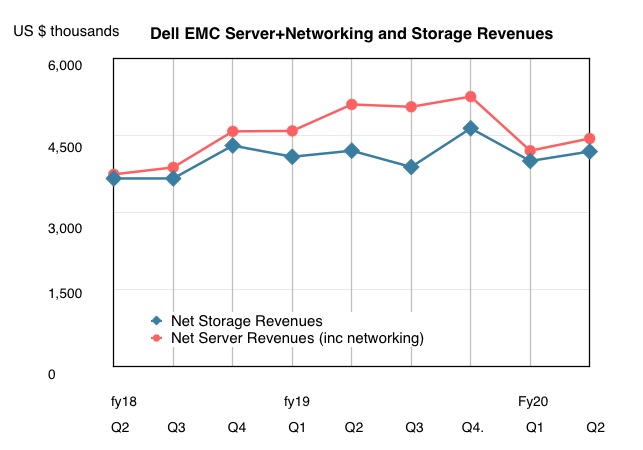

Within ISG, server+networking revenues were $4.4bn, down 12 per cent on the year, while storage was flat at $4.2bn. A chart shows how revenues for the two product lines are tracking each other closely after a gap when storage revenues fell back. But that period of storage weakness is over. In fact Dell is seeing slightly rising storage demand with orders up one per cent.

There was operating income of $1.1bn, up 4 per cent Y/Y to 12.2 per cent driven by better component costs and a higher storage mix. Dell reported strength in Isilon filers and its Unity XT midrange storage array. Hyperconverged VxRail orders grew an outstanding 77 per cent – as Dell basically slaughtered most of its HCI competitors.

It also saw growth in converged infrastructure.

Number one boasts

Dell said it is growing faster than competitors and cites IDC numbers which show it is the leader in external enterprise storage with 34.4 per cent share; leads in storage software (17.5 per cent); ranks first in all-flash arrays (34.2 per cent), and is first in hyperconverged systems (32.2 per cent).

It’s also number 1 in servers in revenues and units terms.

Earnings call

There was enterprise softness but not an enterprise buying slowdown.

In the earnings call Clark said: “We’re seeing a clear split between enterprise infrastructure and PC spending globally. In enterprise infrastructure the market is softer than we and the industry anticipated.”

“We expect to remain soft through the balance of the year, particularly in China. We feel really good about our ISG execution in Q2 given the market context. In the first half, we acquired approximately 21,000 ISG customers, up 11 per cent from the prior year.”

The storage side of ISG looks good: “Our storage business remains healthy in Q2 with orders up 1 per cent and first half orders up 4 per cent. Our sales team remain optimistic about our portfolio and positioning as we head into the second half of the year.”

ISG servers were less good this quarter; “Outside of China, our server orders were up 1 per cent and we expect to gain share this quarter in North America and EMEA, when IDC publish its results next week. Our server ASPs remain strong, up high single digits, as customers are increasingly buying higher end system support for their … high value workloads.”

Enterprise sales softness was more apparent in servers than storage. A revenue weakness in China was due to Dell withdrawing from some hyperscaler business that wouldn’t be profitable.

Dell’s hyperconverged systems performance outstrips the competition by so much that distant competitors, such as Cisco, could walk away from this market.

Overall, Dell dominates the storage industry and is set to dominate it more. Some relative weaknesses include:

All-flash array HW/SW versus Pure Storage and others,

Data protection software vs Acronis, Commvault, Druva, Rubrik, Veeam, etc.

High performance computing, where Qumulo, DDN, HPE (Cray ClusterStor) and WekaIO look stronger

Hybrid cloud – where NetApp’s Data Fabric looks good

Metadata management versus Hammerspace

File lifecycle management and tiering (InfiniteIO, Komprise),

Secondary storage management vs Actifio, Cohesity, Delphix and others

Tape.

But these are largely outliers, as seen from Dell’s mainstream market’s viewpoint. Why bother when it can make bigger returns by extending core products and taking share from everyone else?

NetApp has announced a stripped down, hot-box, EF series all-flash array with double the performance of its predecessor.

Suggested EF600 workloads include Oracle databases, SQL Server, real-time analytics, and hig performance computing applications on top of a BeeGFS parallel file system.

NetApp said the EF600 offers a leading price/performance ratio for these workloads, especially compared to SAS-based all-flash arrays, but has not revealed pricing.

EF block storage arrays sit below NetApp’s ONTAP AFF unified file and block arrays in terms of general power and stripped down software features.

The EF570 was launched in September 2017, two years after the 2015-launched EF560 which it replaced. Now, two years later, we have its replacement.

EF600 bezel.

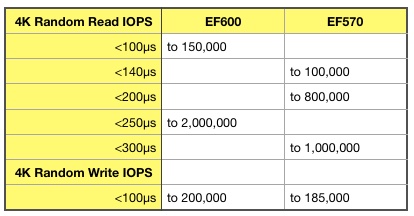

The new top-end EF600 all-flash array, with its end-to-end NVMe storage, is twice as fast as the EF570, at 2 million IOPS. The EF570 supported NVMe-over Fabrics access by host servers but didn’t have an NVMe path to the drives.

That meant the EF570 could output up to 21GB/sec while the EF600 cranks up to 44GB/sec. It can also support lower latencies for more IOPS than the EF570, particularly for random reads:

Oddly, the EF600 only supports up to 360TB of raw capacity from the 24 drives in its 2U chassis, while the EF570 supported up to 1.8PB from its 120 drives, spread across a 2U base chassis and 4 expansion shelves. We have asked NetApp why the EF600 has lower capacity and no expansion capability.

Simplified choices

The EF600 has a greatly simplified set of IO port choices compared to the EF570:

Basically, 16Gbit/s Fibre Channel, SAS and 10 and 25Gbit/s iSCSI are canned, with the EF600 supporting NVMe over Fabrics (using Fibre Channel, InfiniBand or Ethernet) or 32Gbit/s Fibre Channel only. Mellanox provides the 100Gbits network controllers needed for NVMe across InfiniBand or Ethernet (ROCE.)

Another aspect of EF600 simplification over the EF570 is host OS support. The EF600 supports hosts with the SUSE Linux Enterprise Server OS only. In contrast the EF570 supported IBM AIX, Centos, Windows Server, Oracle Enterprise Linux and Solaris, VMware ESX and both Red Hat and Ubuntu Linux as well. All gone now and, again, we have asked why?

The EF600 supports SANtricity Snapshot and volume copy, but not SANtricity thin provisioning, synchronous and asynchronous mirroring or Cloud Connector, which the EF570 did. We have asked NetApp why it has removed these options.

There’s a NetApp blog about the EF600 which points readers to a product webpage and that leads on to a data sheet.

NetApp query answers

Blocks & Files gratefully received answers from NetApp to the questions we asked and here they are;

Blocks & Files; The EF600’s Max raw capacity is 360TB while the EF570’s is 1.8PB. Why is this please?

NetApp; The reason for this is contained in question #2; 24 drives maximum limits the max capacity possible. There is no software architectural limit; as larger SSDs are integrated, the max raw capacity will increase.

Blocks & Files; The EF600 supports 24 drives with no expansion shelves while the EF570 supports 120, via 4 expansion shelves. Why does the EF600 support far fewer drives?

NetApp; The EF600 is focused on extreme low latency and high performance, which are most efficiently accomplished within a single enclosure.

Blocks & Files; According to a data sheet the EF600 supports SANtricity Snapshot and volume copy, but not SANtricity thin provisioning, synchronous and asynchronous mirroring or Cloud Connector. Why not please?

NetApp; The initial release of the EF600 is laser-focused on very low latency and high performance as mentioned. Additional features are planned for future releases.

Blocks & Files; The EF600 supports only one host OS – SUSE Enterprise Linux Server. The EF570 supports IBM AIX, Centos, Windows Server, Oracle Enterprise Linux and Solaris, VMware ESX and both Red Hat and Ubuntu Linux as well. Why the slimmed down host OS choice please?

NetApp; The current narrow OS matrix is solely due to the state of support for NVMe in the operating systems. SLES 12 SP4 is the first enterprise-ready OS for NVMe-oF that supports Asymmetric Namespace Access (ANA) which is required for high availability I/O paths. There are other OSes not far behind that can be certified when they are available.

Blocks & Files; Does the EF600 have different CPUs than the EF570? Is that why it can do 2 million IOPS instead of the EF570’s 1 million IOPS?

NetApp; The EF600 does have newer generation processors, but there are many innovations for performance in the product.

Blocks & Files; If so is that part of the reason why the EF600 can sustain lower latencies for a greater number of IOPS?

NetApp; There are improvements in the NVMe devices’ latency in addition to product latency improvements.

Blocks & Files; Do the Mellanox network controllers also help with the lower latency and more sustained IOPS numbers?

NetApp; We were not sure if this question was about the host adapters or the controller HICs (host interface cards). Mellanox is a great partner, enabling us to deliver a robust RDMA-enabled solution for both EF600 and EF570. For the EF600we are seeing the same latency and IOPS improvements across the interfaces, regardless of whether NVMe/FC vs. NVMe/IB or NVMe/RoCE is in use.

Nutanix delivered poor topline results for its fourth fiscal 2019 quarter and full year, with quarterly revenue down and deeper losses. A good outlook, a smaller loss per share than expected plus internal growth indicators made it all okay and shares rose 19 per cent in post-market trading.

But when will the hyperconvergence vendor stop losing money?

Wells Fargo senior analyst Aaron Rakers said “Nutanix’s F4Q19 results and F1Q20 (Oct ’19) guide should be considered net-positive; albeit it remains difficult to envision Nutanix’s path to profitability.”

Jason Ader, an analyst at William Blair, said: “We believe Nutanix has… a path to cash breakeven within the next few years…. While Nutanix’s subscription transition has been painful, it should yield better visibility/predictability, customer lifetime value, and sales leverage over time.”

Cash breakeven “within the next few years” could mean three to five years time, and that’s breakeven, not a profit.

The Q1 fy2020 outlook is for revenues between $300m and $310m, which compares to $313.3m reported in Q1 fy2019. Shares rose 13.5 per cent after the results were announced.

Background

Nutanix believes customers want and need subscription software that can run on-premises and in the public cloud. Tying software to hardware is the wrong way to go in a hybrid cloud era. Nutanix says it is easier for a hybrid cloud with a Linux-based on-premises offering such as Nutanix to work with the big public cloud players which also use Linus, than non-Linux competitors such as VMware.

Consequently it is shifting from hardware life-bounded license sales to subscription billing. And it is also getting out of selling hardware. The transition has resulted in “revenue compression”. Nutanix says this is necessary pain and it will gain more predictable, consistent and larger revenues as a result of the two switches. It also claims competitors will have to go through the same painful transition.

Additionally the company reported revenue generation issues last quarter, which it attributed to a spending switch from lead generation to engineering and product development at the start of fiscal 2019. There was also a shortfall in sales rep headcount and sales execution issues in the USA.

Lastly, competitors NetApp and HPE have reported a slowdown in large systems sales to enterprises, due to macro-conomic factors such as trade disputes, and this may have affected Nutanix too..

The numbers

In a statement CEO Dheeraj Pandey declared: “We delivered a solid fourth quarter and believe our performance reflects our execution improvements and the meaningful progress we have made transitioning our business to a subscription model.”

The revenue and net income numbers were:

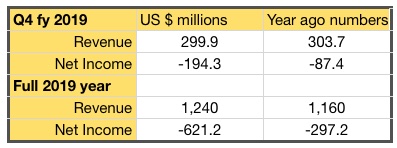

Q4 fy2019 revenues were down 1.3 per cent while the loss more than doubled. Full year revenues increased 6.9 per cent and the loss for the year also more than doubled.

Under the surface of this picture of a high-growth company apparently running towards the buffers, there are encouraging signs.

Q4 revenue came in at the top end of its $290m -$300m guidance.

Nutanix added 990 new customers in the quarter, taking the total to 14,180, and the highest increase for 6 quarters.

Sales and marketing headcount increased by 254, compared to 107 and 207 in the two prior quarters respectively.

Exited quarter with more than 2.5 times the order backlog of the prior quarter.

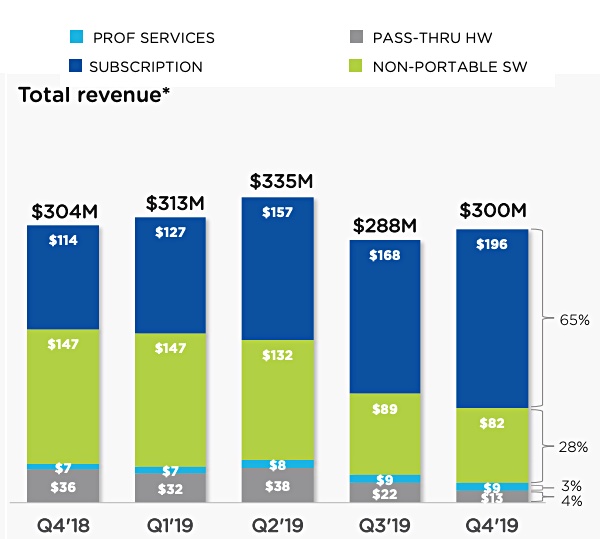

Subscription revenues were $196m, up 72 per cent, representing 65 per cent of revenues. The company is targeting 75 per cent subscription revenues in 12 months.

Software and support revenues rose seven per cent to $286.9m.

Gross margin of 80 per cent rose 2.3 per cent and is a record.

Loss per share of $0.57 vs analyst expectations of $0.64

Free cashflow was -$33.3m though, compared to $6.5m a year ago.

Subscriptions soaring

A look at the revenue mix trends shows the rising subscription revenue trend:

The revenue mix shows the increasing importance of subscription revenues and declining hardware ones. Non-portable SW is Nutanix SW delivered with and licensed to particular hardware. The proportion of this is declining as well. Portable SW can run on-premises or in the public cloud.

Sales of software above the basic hyperconverged hypervisor layer rose, CFO Duston Williams noted: ”26 per cent of our deals included a product outside our core offering.” He’s talking about software such as Files, Era for database workloads, Cam and other multi-cloud workflow software.

Earnings Call

Pandey said in the earnings call: “Q4 was a good quarter for us, as we beat Street expectations on total billings and revenue and by $15 million each for software and support buildings and revenue… our Q4 results demonstrated measurable progress in our subscription transformation, our pipeline funnel, our sales re-enablement, our simpler messaging on the platform versus new apps and our hybrid cloud journey.”

He added: “Our solid quarter-over-quarter billings and revenue growth, as well as our progress in sales hiring are clear indicators that our execution is improving and our market remain strong.”

Wiliams said the subscription transition cost Nutanix $20m to $25m in revenues in the quarter.

Asked about signs of macro-economic weakness, he said: “There’s really been no additional signs or signals that we’ve seen.” The effects of its own subscription transition have masked any indication of the enterprise buying slowdown that has affected NetApp and HPE.

Sales force segmentation

Nutanix plans to split its salesforce between the enterprise and to the commercial mid-market. Pandey said: “We have segmented commercial completely out of our enterprise sales figures and [are] building a focused U.S. commercial sales leadership and an organization under them.”

It wants reduced sales person involvement “so prospects can go without any human touch from digital ads to our clusters in the cloud with a few clicks.”

Comment

Are the glory growth days, with 20 per cent plus revenue growth/quarter, over for Nutanix? The subscription transition will last through its fiscal 2020 and there’s no certainty beyond that. The company believes it will be better positioned than icompetitors for the hybrid multi-clouds oftware subscription era, but that means it predicts pain for them, not growth for itself.

Nutanix’ hardware-centric channel has to get used to selling subscription software deals and that’s uncharted waters. But there are good growth signs, including customer growth and the increased number of large deals.

Nutanix is an enigma. It’s like a hot air balloon that’s stopped rising while it changes its fuel to an untried type, hovering in mid-air waiting for the old fuel to burn off and the new stuff to start working

At some stage it has to turn a profit, and that means either growing revenues by more than $200m/quarter, the current net loss, and/or taking cost more than $200m/quarter costs out of the company. The first seems fanciful at the moment and the second … well, let’s not go there.

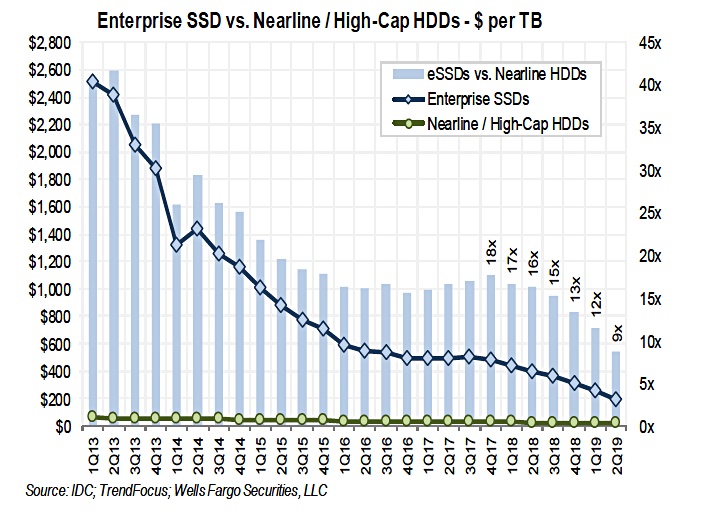

Aaron Rakers, the Wells Fargo analyst, thinks enterprise storage buyers will start to prefer SSDs when prices fall to five times or less that of hard disk drives. They are cheaper to operate than disk drives, needing less power and cooling, and are much faster to access.

So when will the wholesale switch from nearline HDD to SSDs begin? We don’t have a clear picture yet but a chart of $/TB costs for enterprise SSDs and nearline disk drives shows how much closer the two storage mediums have come in the past 18 months.

It is unwise to extrapolate too much but it is clear the general trend direction is that Enterprise SSD cost per terabyte is falling faster than nearline disk drive cost/TB. Our chart below shows the price premium for enterprise SSDs has dropped from 18x in the fourth 2017 quarter to 9x in the second 2019 quarter.

Chart prepared by Wells Fargo senior analyst Aaron Rakers, using IDC and TrendForce data.

Business disk drive sales are mostly dependent on high capacity – 8TB to 14TB, spinning at 7.2K rpm – drives that to store secondary or nearline data. Fast mission-critical disk drives, spinning at 10K to 15K rpm, have largely given way to faster access SSDs.

However, SSD capacities are growing even faster. QLC (4 bits/cell) NAND adds 25 per cent more capacity, compared to current TLC (3bits/cell). And layer counts in 3D NAND are set to rise from the 64-layer mainstream and arriving 96-layer product to 128-layers and beyond.

A 128 layer 3D NAND die will have twice the capacity of a 64-layer die and a third more than a 96-layer die. With our simplistic math that means a 128Gbit 64-layer TLC die will become a 340Gbit 128-layer QLC die and cost substantially less per TB to make than the 64-layer TLC 128Gbit version.

And PLC (5bits/cell) flash is being developed, with 25 per cent more capacity than QLC flash.

This time next year the three disk drive makers -Seagate, Toshiba and Western Digital – could see their nearline business start spinning down.

Toshiba and Western Digital are partners in NAND fabrication and make and sell SSDs. Seagate has no NAND fab interest and is a small player in the SSD market, making it the most vulnerable to SSD cannibalisation of the nearline disk business.

Micron’s against this view

Colm Lysaght, Micron’s Senior Director, Marketing Strategy and Innovation, took issue with this and told Blocks & Files by email: “I don’t argue with the cost trends shown ]above], and clearly SSD price/GB will get closer to HDD price/GB over time.

“I also don’t dispute the lower TCO of an SSD compared to an HDD, nor the faster access.

“However, the raw number of EB needed for a “wholesale switch” from nearline HDD to SSD is far too large for the NAND flash industry to contemplate. The capital investment needed to generate the EB required (which will continue to grow at a rate of about 30 per cent per year) is prohibitively expensive.

“SSDs may nibble (and maybe even munch) at the nearline HDD market, but both will coexist for many years to come.”

Good points, all.

Rakers rebuts

Wells Fargo senior analyst Aron Rakers told subscribers: “While we see most investors already appreciating the SSD replacement of mission-critical HDDs, we have seen little debate at this point over the possible encroachment into nearline HDD workloads.

“However, we think this could evolve as the NAND industry looks to integrate / leverage QLC-based 3D NAND (note: Pure Storage expected to intro new QLC-based all-Flash arrays for lower-performance primary storage applications next week) and we have also seen SSD $/GB fall to sub-10x vs. nearline HDDs.”

Our take is that SSD encroachment of nearline drives could start but will take many years to complete, if it does complete, because vast amounts of new SSD foundry capacity will be needed.

Overall revenues slipped seven per cent to $7.2bn. Within that, server sales dipped 12 per cent to $3.15bn.

In the earnings call yesterday, CEO Antonio Neri talked of an uneven market and disciplined execution, which expanded profitability across the company while revenues fell.

The overall revenue downturn was attributed to portfolio rationalisation (getting out of cheap servers for hyperscalers) and macroeconomic factors. He said: “We continue to see uneven demand due in part to ongoing trade tensions which impact market stability and customer confidence.”

“This is showing up in elongated sale cycles, particularly in larger deals.” In storage Neri said HPE: “overall experienced a modest revenue decline against the tougher market backdrop in year-over-year compare.”

Storage sales

But there was a bright spot. In constant currency terms Nimble array sales grew 21 per cent while the SimpliVity hyperconverged product segment grew at a more modest four per cent, way down from its 25 per cent growth in the previous quarter.

The Synergy composable systems business grew most rapidly, up 28 per cent. This was also a marked reduction on its 78 per cent sales growth in the prior quarter.

The SimpiVity and Synergy growth slowdowns could be attributed to enterprise buyers slowing purchases.

It’s clear that the enterprise 3PAR array business did nor grow, and the newly announced Primera arrays were too recent to affect sresults.

Wells Fargo senior analyst Aaron Rakers told subscribers the: “Primera(3PAR) high-end cycle will materialize through 2H2019.”

SMB and US sales

Neri noted: “The SMB mid-market continues to be strong, and this is where we are putting a lot of emphasis on what we call the no touch low touch model for the transaction of high velocity business.”

As with NetApp, HPE acknowledged a US sales execution problem, which it is tying to fix: “We are actively addressing the sales coverage model in the United States. I am pleased with the actions taken to date that have resulted in positive [growth] with our US product business, which was up over 40 per cent sequentially.”

But the fundamentals are strong: “Explosion of data will continue to fuel underlying demand for solutions to help protect, store, manage and analyze their data. And this is where we are laser focused. We have a strong portfolio solutions and services that span the Intelligent Edge and hybrid cloud.”

Looking for growth

HPE’s strategic areas of product investment are high-performance computing, hyperconverged infrastructure, hybrid cloud (meaning servers and storage) and the PointNext/GreenLake subscriptions business.

Neri pointed out underlying signs of health with improving gross and operating margins and a record level of year-to-date free cash flow ($860m). HPE is shift its product mix towards higher-margin, higher value, software-defined products delivered as a service.

This will help it maintain margins as commodity prices, such as DRAM and NAND, fall. CFO Tarek Robbiati pointed out: “Fiscal year ’19 was not a year where we wanted to dial-up to growth. Fiscal year ’19 is a year, where we had to deliver on EPS commitment, drive free cash flow. These are the two most important metrics, prepare ourselves to dial-up to growth in the subsequent quarters.”

HPE’s fiscal 2020 then is being signalled as a revenue growth year, with Robbiati confirming that: “notwithstanding the consolidation of Cray, we will grow our business overall.” The Cray acquisition is expected to close in October.

The company has raised its non-GAAP earnings per share (EPS) outlook for the year, the seventh quarter in succession it has done this. There’s confidence and disciplined execution in action.

But when will the enterprise buying slowdown end? The China-US trade tensions could well affect the next quarter and the one after that. Trumponomics are unpredictable.

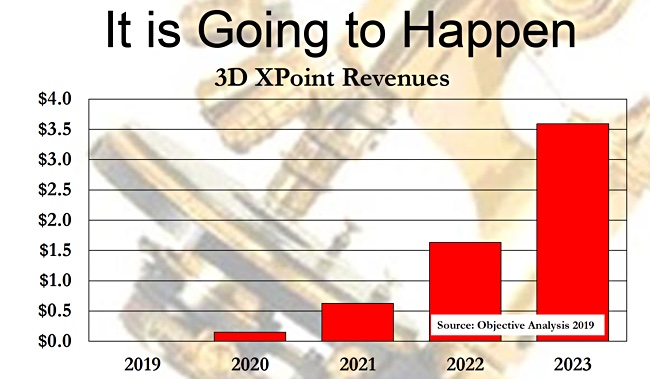

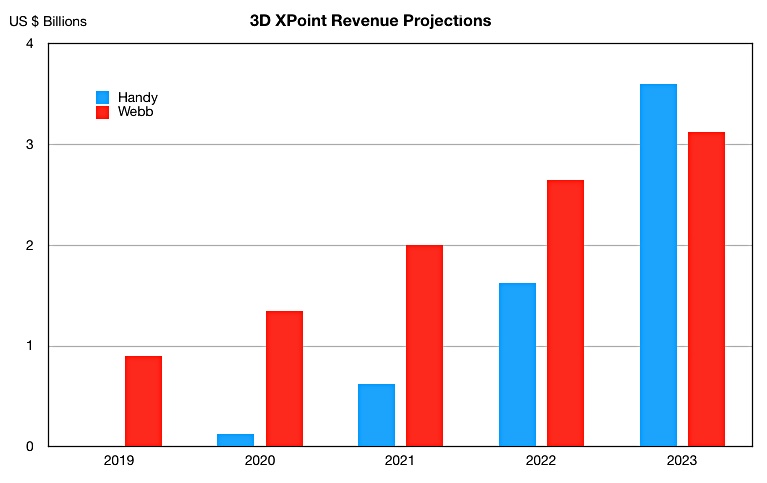

3D XPoint media revenues will grow to more than $3bn in 2023, propelled by system software support and lowered manufacturing costs.

XPoint expert analyst presentations at the Flash Memory Summit 2019 in San Jose this month were based on a belief that XPoint is now a viable storage-class memory (also called persistent memory) and sales will take off in 2019 or 2020.

Jim Handy, the memory guy at Objective Analysis, showed a chart of predicted XPoint revenues in his FMS 2019 presentation:

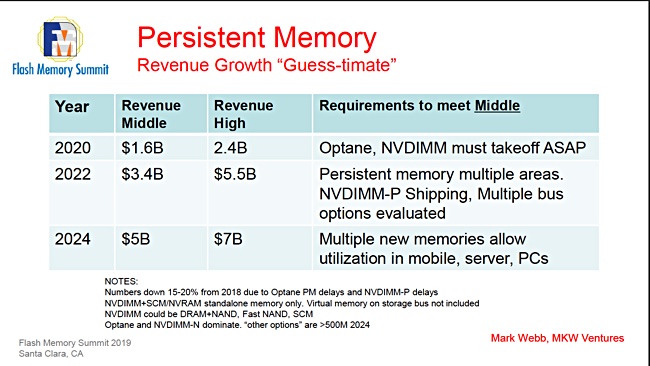

Mark Webb of MKW Ventures Consulting, also showed an XPoint projected revenue table.

Webb looks out a year further than Handy, and includes non-Optane media in 2024. Blocks & Files thought a direct comparison between the Handy and Webb projections would be a good idea. We guesstimated numbers from Handy’s chart and put them into a spreadsheet model.

Webb skipped 2020 and 2022 in his slide but Blocks & Files interpolated numbers in these years by splitting the difference between the previous and following years to arrive at this table;

That enabled us to chart and compare both sets of numbers:

Handy thinks XPoint revenues start quite slowly in 2020 but then accelerates out to 2023. Webb differs with a near-$1bn number this year and then a linear rise out to 2023. At this point, Handy’s projected revenues surpass Webb’s.

Webb and Handy are making best-estimate assumptions about Optane DIMM and XPoint SSD sales; their relationship to Intel Cascade Lake server sales; the ratio of DRAM to XPoint DIMMs in servers; and the entry of Micron into the XPoint market.

They both arrive at $3bn- $3.6bn revenue range in 2023.

Gen 2 XPoint

Intel and Micron are planning for its generation 2 of Optane in 2020, according to Webb. He estimates it will have 4 stacks, instead of Gen 1’s 2, but similar lithography. It will still be SLC (1 bit/cell) but have a 35 per cent lower bit cost with its 256Gbit die than Gen 1’s 128Gbit die.

He said there should be measurable Gen 2 XPoint volume in late 2020.

In Webb’s view Micron will not ramp its own Gen 1 XPoint sales. Its plan is to wait for Gen 2 and then develop its own markets. Blocks & Files thinks that Micron may make its XPoint media usable as memory by AMD processors, also perhaps ARM systems, IBM POWER processors and GPUs.

Webb points out that Micron’s Lehi, Utah plant is the only XPoint fab and will be able to support Intel’s needs and Micron’s initial ramp. It will output 45m GB/month of Gen 1 XPoint in the fourth quarter and 5m GB/month of Gen 2 XPoint. A year later the Gen 1 output will be the same but Gen 2 will have risen to 25m GB/month.

Under the terms of the Intel-Micron joint venture, now being dissolved, Micron is required to provide XPoint capacity to Intel for another year from October 2019. It could agree to provide capacity for longer still, thus saving Intel the cost of developing its own XPoint fab.

With an XPoint fab likely costing north of $10bn to develop from scratch and the Lehi fab capable of of doubling or tripling output Intel could defer building its own fab for some time.

Note. the Handy and Webb presentations scan be found in the presentation set downloadable from the FMS 2019 website.

SK hynix's 128-Layer 1Tb TLC NAND Flash")