Infinidat today boasted it makes the fastest SAN array with the lowest latency and can prove it – albeit with its own test results.

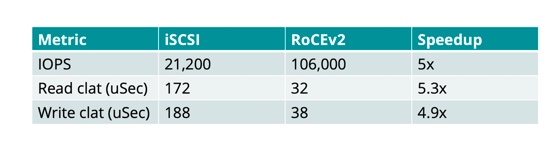

The high-end array vendor used the flexible IO testing tool Fio to compare iSCSI access to its array and NVMe-over-Fabrics access.

The round trip latency to an Infinibox array using iSCSI was 172 μs for reads and 188 μs for writes. Latency was reduced to 32 μs for reads and 38 μs for writes when using NVMe-oF with Remote Direct Memory Access over converged Ethernet (RoCE).

New Infiniboxs are ‘NVMe-oF ready’ and the company plans to make the technology generally available via a “non-disruptive software update within a year”.

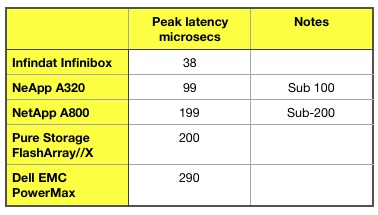

In a blog titled ‘Dell, Please Stop Calling PowerMax The World’s Fastest Storage Array’, Indinidat CTO Brian Carmody compared the Infinbox Fio benchmarks with published numbers for Dell EMC’s PowerMax array, NetApp’s AFF A800 and Pure Storage’s FlashArray//X.

His sources include NetApp figures for the A800 and a Pure Storage FlashArray///X data sheet (pre-NVMe-oF, claiming 250 uSec) and Pure’s statement that NVMe-oF would give a 20 per cent speed-up.

Blocks & Files has added latency figures for NetApp’s latest A320 all-Flash FAS array as these became available today:

We have given the A320 and A800 notional numbers as they are listed as sub-100 and sub-200 respectively by NetApp.

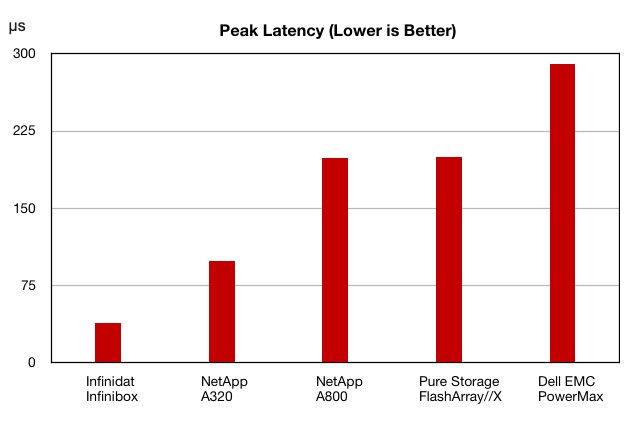

Graphing these numbers shows us how they compare:

Infinibox uses memory caching and is faster than rival all-flash arrays which retrieve data from flash, according to Carmody. He claimed Infinidat will retain its lead so long as no-one else moves to memory caching.

Secondary data converger Cohesity has bought its first company, a NoSQL backup supplier called Imanis Data, for an undisclosed sum.

Blocks & Files thinks the Imanis acquisition strengthens the similarities between Cohesity and its rival, Rubrik.

Cohesity founder and CEO Mohit Aron said in a prepared quote: “Cohesity’s acquisition of Imanis Data advances our mission to transform the way that enterprises back up, store, manage, and derive insights from their secondary data, no matter its type or where it resides.

“NoSQL databases will likely experience double-digit growth over the next five years, and as enterprises continue to embrace these modern workloads, Cohesity can help ensure the data is protected.”

Yet another single pane of glass

By combining Imanis software with Cohesity, customers can manage their non-distributed and distributed NoSQL and Hadoop workloads from a single pane of glass.

Cohesity said Imanis software is data-aware, petabyte-scale, and uses machine learning to reduce cost. It is already available as an application in the Cohesity MarketPlace. The two companies are said to share many customers.

Imanis Data was founded as Talena Software in 2013. Talena’s mission was to back up distributed databases in a way analogous to that of DatosIO, a company that Rubrik acquired in February 2018. Talena raised $25.5m in two funding rounds and changed its name to Imanis Data in 2017.

In September 2018 Imanis introduced automated backup for Hadoop and NoSQL apps, supporting Apache Cassandra, Apache HBASE, Cloudera, Couchbase, DataStax, Hadoop, HDInsight, HortonWorks, Microsoft ADLS, MongoDB, and Vertica platforms.

The Imanis team is joining Cohesity, with co-CEO Nitin Donde at the helm.

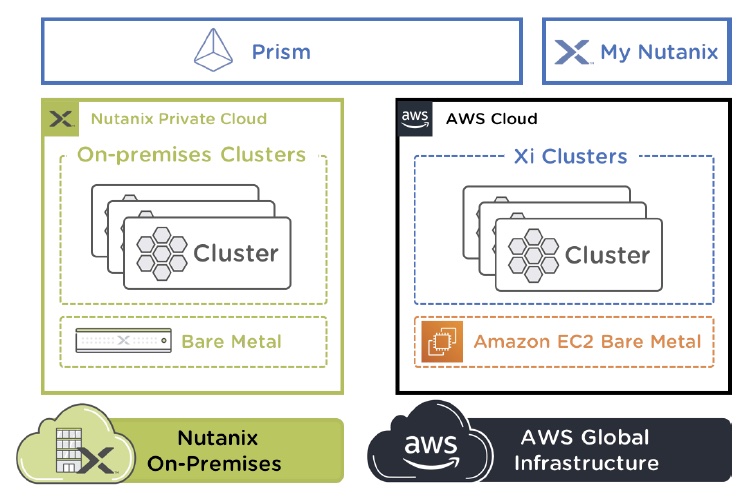

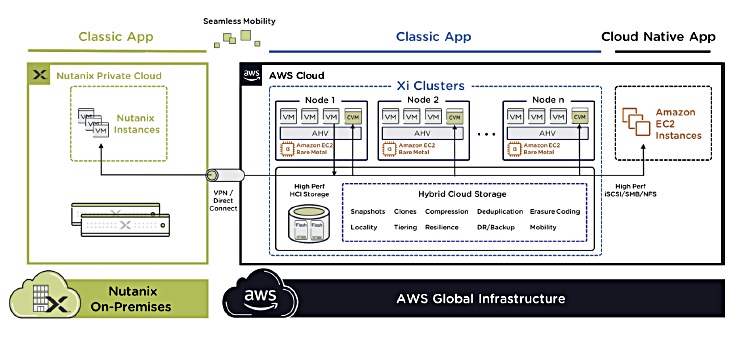

.NEXT 2019 Nutanix is moving into the hybrid cloud world in a big way by making its software available on AWS.

Customers can launch Nutanix’s Enterprise Cloud OS within their AWS environment via Xi Clusters. They do not need to create a new AWS account, VPCs or WAN networking scheme, Nutanix announced today.

Xi Clusters brings up AOS nodes in AWS bare metal servers. These are managed using Nutanix’s Prism Central console.

With Xi Clusters, the complete Nutanix HCI stack runs directly on AWS EC2 bare metal instances. The bare metal runs the AHV hypervisor and, like an on-premises deployment, runs a Controller Virtual Machine (CVM) with direct access to NVMe instance storage hardware.

Xi Clusters allows customers to spin up clusters on bare metal in EC2 on demand and in minutes. The cloud infrastructure is available from AWS at an hourly rate, and this AWS facility can be used for bursting.

AWS bills customers directly for infrastructure spend and Nutanix charges for the cost of Nutanix software when Xi Clusters are used.

With Xi Clusters, classic apps can be on the same subnets as cloud-native services and apps, Nutanix said. Apps can move between the Xi Clusters to AWS EC2 native without IP address changes or network reconfiguration. The company claims the result is native network performance with minimal overheads.

Xi Clusters AWS architecture diagram.

Nutanix has modified its AHV virtualization software to add AWS networking integrations that lower latency and improve performance. When virtual machines (VMs) talk to each other they are directly switched by AWS within the Xi Clusters or to native EC2 VMs.

AWS Xi Clusters can be hibernated in S3 and spun up again when EC2 compute resources are needed. This aids repeated bursting of EOS to AWS instances.

Read a Xi Clusters blog by Nutanix Cloud Services CTO Binny Gill to find out more.

.NEXT 2019 Nutanix today announced Nutanix Mine, a way of converging the management of secondary backup data with ordinary data management operations.

By converging primary and secondary data storage, Nutanix will compete directly with Cohesity’s hyperconverged secondary storage business.

The company is supplying a bunch of native integration with backup products made by Veeam, HYCU, Commvault, Veritas and Unitrends via the Nutanix Enterprise Cloud Platform.

Cohesity was founded by Mohit Aron, the ex-CTO of Nutanix, and provides backup and supplies secondary data to other operations. By bringing backup data into its orbit Nutanix can do the same without competing with backup software vendors.

Subbiah Sundaram, HYCU VP products, said: “That is what Nutanix Mine with HYCU is fundamentally all about. Backup becomes an invisible service of the Nutanix platform.”

How many single panes of glass does a company need?

Customers can use the Nutanix Prism console as a single point of management for primary and secondary storage within their private clouds.

Nutanix said Mine will simplify overall deployment, on-going management, scaling and troubleshooting of the backup process. Mine scales primary and secondary storage as business growth dictates, Nutanix said.

Secondary storage silo

The company seems to be saying that dealing with primary and secondary data in the same silo is the real hyperconverged approach.

Sunil Potti, chief product and development officer, Nutanix, provided a canned quote: “Even as customers embraced HCI, the secondary storage silo persisted. With Nutanix Mine, customers will get all the benefits of collapsing this silo into a single platform – reduced management complexity, simplified operations and reduced TCO – without the requirement that they forgo the backup solution best suited for their business needs.”

It can say to customers that secondary data should not be stored and managed in a separate silo – that is not hyperconvergence. Deal with primary and secondary data in the same silo – that is hyperconvergence.

The delivered kit

Nutanix’ channel takes the Nutanix SW, adds in the customer’s backup engine of choice and supplies an X86 server, such as a Supermicro, running the resulting SW concoction. For the backup software the target storage device is the Nutanix storage hardware, not a separate deduplicating backup target appliance.

This is the equivalent a Nutanix insider said, of a combined Nutanix and Data Domain system.

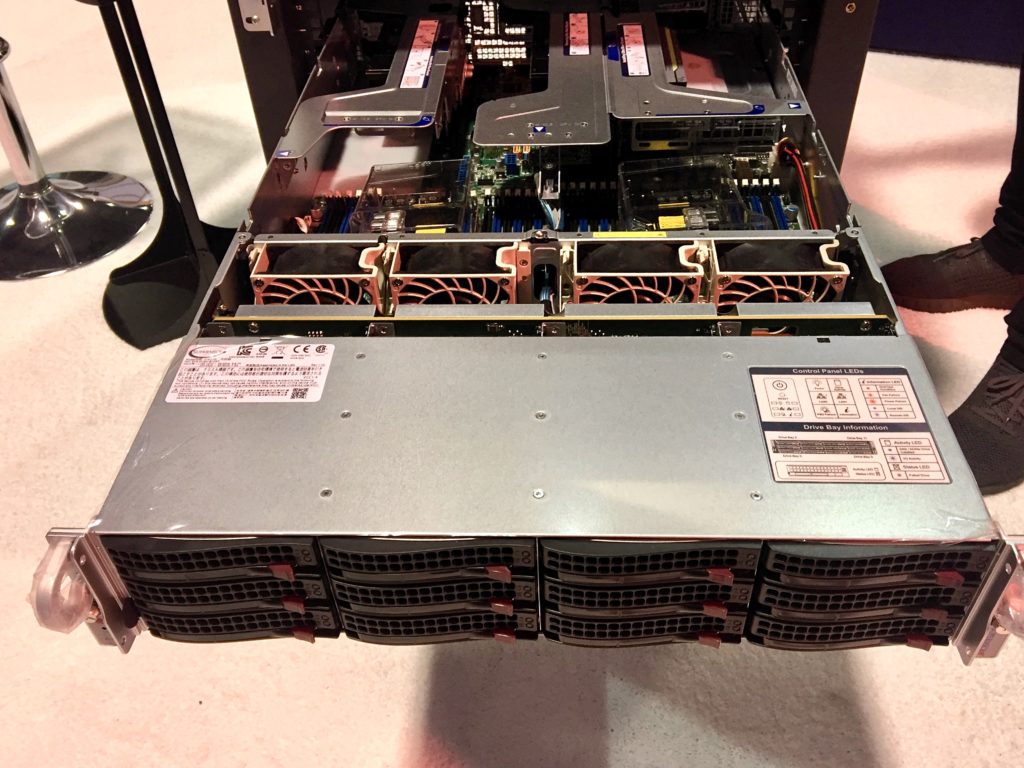

Supermicro exhibited a 2U, GPU-accelerated storage server at the .NEXT event in Anaheim, a SYS-6029U-E1CRT product, which supports dual Gen 2 Xeon SP (Cascade Lake) or Xeon SP (gen 1) processors.

Supermicro SYS-6029U-E1CRT server exhibited at .NEXT.

It can have 12 hot-swap front-mounted, 3.5-inch drive bays, either NVMe SSDs or SAS hard disk drives storing up to 144TB raw capacity (12 x 12TB). The chassis can hold up to 6TB of DDR4 memory, up to 6TB of Optane memory in memory mode, not App Direct mode. There is space for GPU cards – Tesla M0, T4 or V100s – in either side of the chassis at its rear.

This is a high-powered server/storage chassis, designed to for GPU-enhanced analysis of data.

Blocks & Files thinks Mine gives Nutanix a starting position to analyse stored secondary data – data mining, in other words. Otherwise, why call it Mine?

Availability

Nutanix Mine with Veeam and Nutanix Mine with HYCU, both with Nutanix SKUs and sold through Nutanix resellers, are expected to be available in Q3 2019. Nutanix Mine with Commvault, Veritas and Unitrends will be available in a future release.

In a blog discussing the announcement yesterday, IBM WW cloud storage portfolio marketing manager David Wolhford revealed the rationale for the reseller deal.

The combination of Panzura Freedom Cloud NAS with IBM Cloud Object Storage overcomes the limitations of network-attached storage (NAS), according to Wohlford.

“Traditional NAS has seen better days,” he wrote. “IDC estimates that scale-up file storage is shrinking and expected to decline 5.0 per cent CAGR for 2017-2022.”

Panzura CEO Patrick Harr said enterprise businesses ”require the scale and durability of a modern object store with the performance and features of a traditional NAS solution.”

“Our partnership with IBM enables enterprise customers to easily migrate their file-based applications without rewrite, converge their primary and secondary storage and collaborate globally from a single, scalable platform.”

Panzura and IBM Cloud Object Storage

In this tie-up, IBM’s COS is the central repository and Panzura makes file-based apps cloud-capable and available on COS. File storage can be migrated to COS without interruption to workflows or applications.

Users get local access to files from cloud-attached storage, based on Panzura’s cloud storage gateway and file sharing technology.

Freedom Cloud NAS uses Panzura’s CloudFS filesystem and supports file and object access.

IBM diagram showing Panzura and COS. PCFS is Panzura Cloud File System.

DDN dipped its toe into the general enterprise storage market in September 2018 with the purchase of Tintri assets from bankruptcy. This acquisition cements the company’s move into the enterprise.

Post-acquisition,DDN supplies storage software to enterprises in the AI, 5G and IOT markets, taking advantage of Nexenta’s deals with hardware suppliers such as Lenovo.

Nexenta develops ZFS-based file storage and block storage in NexentaStor and also object storage with a separate object storage system.

Post-acquisition, DDN can offer general file, block and object storage with Nexenta and virtualized server storage with Tintri.

As with Tintri, Nexenta will run as a separate operation within DDN. Nevertheless there is scope for cross-selling and technology cross-pollination between the three operations.

Exagrid has a Veeam in its eye

Exagrid has launched ExaGrid Backup withVeeam [Exagrid italics]. This end-to-end system integrates the companies’ products in the following ways:

ExaGrid runs Veeam Data Mover in its appliance and supports the Veeam end-to-end protocol for fast backups. The company claims a 30 per cent increase in backup performance versus other products on the market.

ExaGrid’s architecture uses Veeam’s Scale-out Backup Repository which allows automated job management and linear scalability.

Veeam Backup & Replication’s built-in source-side data deduplication is integrated with ExaGrid’s zone-level deduplication. This reduces storage and bandwidth consumption.

ExaGrid Backup with Veeam comes in three scalable models: a 13TB, 21TB and 32TB backup systems, scalable up to 90TB full backup.

ExaGrid Backup with Veeam is available today in the USA and Canada. The company will consider expansion to other countries in due course.

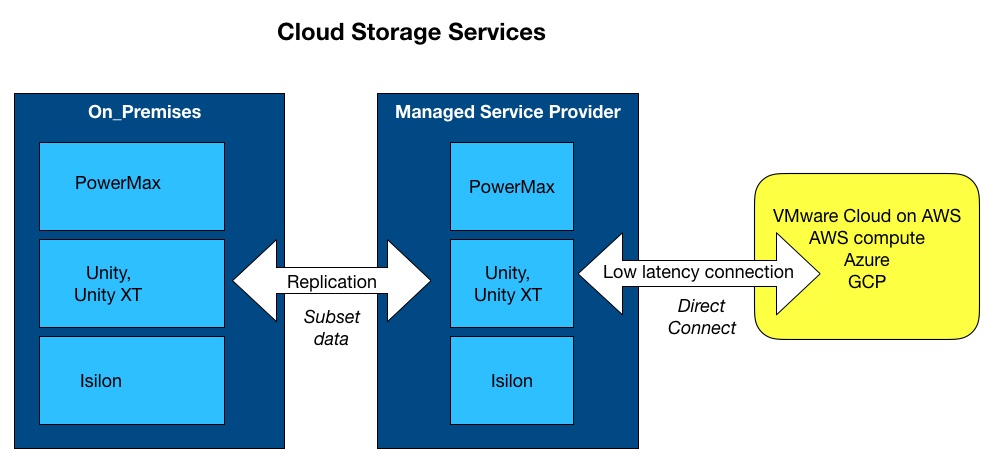

Faction is the Dell EMC Cloud Storage Services MSP

Dell EMC announced Cloud Storage Services last week Dell Technologies World in Las Vegas.

The service Hybrid Disaster Recovery-as-a-Service (HDRaaS) and Cloud Control Volumes for Unity, Isilon, and PowerMax arrays. These require an MSP to house the arrays in a data centre with a Direct Connection to the supported public clouds.

That MSP is Faction, a startup which counts Dell Technologies Capital as an investor. At time of writing it is the sole MSP supporting Dell EMC Cloud Storage Service.

Faction supports AWS, Azure and Google Cloud Platform. It is a member of the Dell EMC Select Partner Program and its products and services are now part of the Dell EMC Select catalogue.

Kaseya gets $500m kash

Kaseya, the acquisitive IT infrastructure management vendor, has nabbed $500m in fresh funding, giving it a $1.75bn valuation. TPG and existing investor Insight Partners are the backers in this round.

The company has promptly bought another supplier, ID Agent, the owner of Dark Web ID, a dark web monitoring platform, and BullPhish ID, a phishing simulator and security awareness training platform. Kasey will integrate the software into its own suite of infrastructure management security products. ID Agent will also run as a separate entity.

Kaseya made four acquisitions in 2018: Unitrends, Spanning Cloud Apps, RapidFire Tools, and IT Glue.

The company claims 40,000 customers worldwide and sells its products to MSPs and small/medium business on-premises IT departments.

Mimecast provides supervision

Mail message provider and archiver Mimecast has announced Mimecast Supervision as part of its Cloud Archive offering.

The software is designed for financial services organisations and addresses compliance requirements. Supervision can be coupled with Mimecast Compliance Protect, which helps firms meet SEC retention requirements.

Supervision includes intelligent selection, enabling customers to focus on specific messages that warrant review and avoid false positives. An optimised workflow helps the review process.

Mimecast Cloud Archive and Supervision are listed on the FINRA Compliance Vendor Directory, joining the list of approved solutions recognised by this financial services regulatory agency.

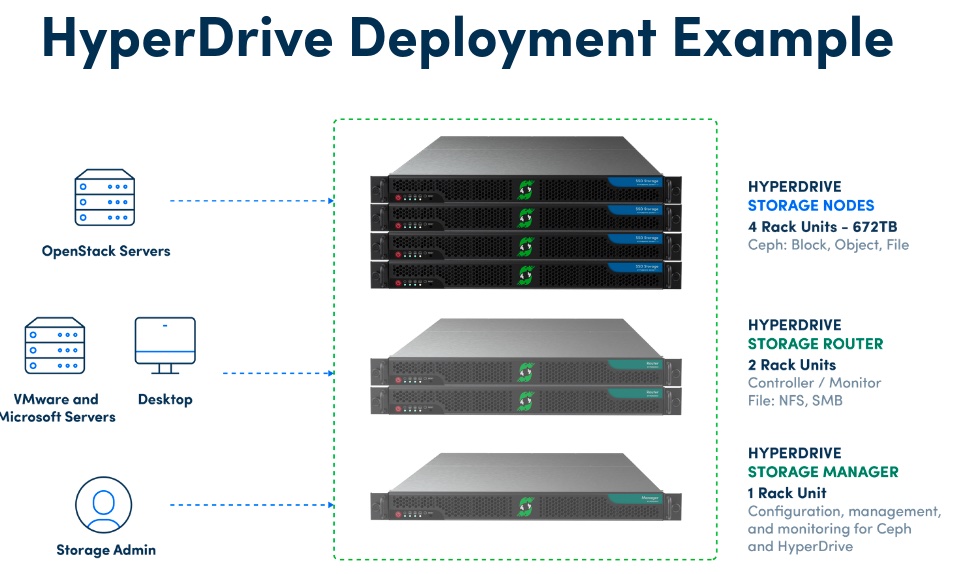

Softiron soups up Ceph-based Hyperdrive

Storage startup Softiron has launched a system that combines performance and internal flash tiering into a single, 1U Ceph appliance.

Called HyperDrive Density+, the system differs from older members of the Hyperdrive family, which need separate management servers and a storage router.

HyperDrive Density+ is available in two versions, a 78TB with 72TB of disk and 6TB of flash, and a 168TB version with 120TB of disk and 48TB of flash.

HyperDrive Density has 120TB of raw capacity using a dozen 10TB disk drives and 960GB of SSD cache.

A table shows the characteristics of the three system.

The 78TB and 168TB model have faster networking via two 100GbitE interfaces instead of the Density model’s 10GbitE pair.

Softiron Density and Density Plus HyperDrive variants

Softiron CEO Tim Massey said: “Currently if you have a situation where you need high-performance drives for one data set and cost-effective storage for another set of data, you’re pretty restricted and really only have two available options.

“You either deploy two different Ceph clusters, one for each data set or, you deploy one Ceph cluster with enough of each drive type to be able to handle redundancy, which is typically triple replicated. As you can imagine, these are very complicated and expensive solutions that are not serving the enterprise in the least. HyperDrive Density+ solves this problem by combining performance and internal flash tiering into a single, 1U Ceph appliance.”

Shorts

Formulus Black won an award for Best Overall Solution for its ForsaOS at the Advanced Scale Forum 2019, April 15-17 in Ponte Vedra, Florida. .

FileShadow has announced FileShadow for Windows Virtual Desktop. This thin provisioned storage separates user data from the operating system, local applications and user settings in the data centre. The company said this reduces costs for any company using virtual desktops.

Liqid Composable Infrastructure is now part of the Dell Technologies OEM & IoT Solutions Portfolio. This is separate from Dell EMC’s own MX7000 composable system as the Liqid system composes virtual systems from pools of disaggregated GPUs, FPGAs, PowerEdge CPUs, NVMe storage and Intel Optane extension technologies, using a low-latency, intelligent fabric.

Customers

InstaDeep, a London-based AI company, has deployed Excelero NVMesh (NVMe-over fabrics storage) for its AI as a Service offering. It said Excelero feeds unlimited streams of data to GPU-based systems with local performance for AI and ML customers. InstaDeep’s Excelero system includes a 2U Boston Flash-IO Talyn server with an Nvidia DGX-1 GPU system, Mellanox 100Gbit/s InfiniBand, Micron NVMe flash and Excelero NVMesh software that provides access to up to 100TB external high-performance storage.

Early tests indicated that external NVMe storage with Excelero gives equal or better performance than local cache in the Nvidia DGX.

Infinidat, the high-end array maker, today launched subscription programs, software with enhanced performance, extended array connectivity, and cloud-delivered array monitoring and analysis.

The company also signalled its intention to enable workloads to move between on-premises and cloud storage in a single fabric.

Infinidat develops hybrid InfiniBox arrays with disk-based capacity storage and SSD and memory caching. The systems deliver performance equivalent to or better than all-flash arrays.

Infinibox and beyond

Let’s run through today’s announcements:

Elastic Data Fabric: the aim is to deliver a fabric supporting seamless workload mobility between systems, data centres, and cloud storage. Infiinidat proclaimed its goal to relegate data migrations to the IT list of extinct technologies and services.

InfiniBox Software v5.0 features:

Network Lock Manager (NLMv4) for NFSv3 filesystems

Active/active replication for 100 per cent data availability

Non-disruptive data mobility for workload relocation between any two InfiniBox systems

Reduction of its sub-millisecond latency, enabling upwards of 2m IOPs

Increased throughput up to 25GB/sec

2. InfiniBox networking and memory extensions:

16Gbit/s and 32Gbit/s Fibre Channel support

25GbitE support

Groundwork laid for NVMe-over-fabrics and faster cache expansion with Storage Class Memory support

3. InfiniVerse cloud-based, AI-driven advanced monitoring, predictive analytics and support system. This includes customisable dashboards for all InfiniBox systems, wherever they reside, as a single system in a SaaS-based offering.

4. InfiniBox FLX subscriptions for on-premises storage and InfiniGuard FLX subscriptions for backup.

Both FLX offerings allow customers to pay for what they use, when they need it, scaling capacity up, or down, as workloads grow, retire, or relocate to other systems. Both provide 100 per cent data availability guarantees, and a full hardware refresh every three years is included in the subscription cost.

Discussion

NVMe-oF support, previewed in March 2019, could be delivered via RoCE or NVMe/TCP over Ethernet, or NVMe/FC. No word yet from the company on what it will plump for.

Together with upcoming SCM support, this will allow Infinidat to deliver the same class of low-latency access as other NVMe-oF and SCM-supporting all-flash arrays and offer multiple petabyte capacity using cheaper-than flash disk storage. Monster 16TB and 20TB disk drives are coming this year and they should enable a capacity jump over the current 10, 12 and 14TB drives.

Subs drive

Infinidat aims to deliver all-flash array levels of performance at hybrid array costs, and to mix and match new technologies such as NVMe-oF and SCM.

It is also taking on board best practices from other suppliers for a public cloud-influenced storage world, with SaaS-based array management, subscription-based array use, and the data fabric idea. We expect Infinidat to establish InfiniBox software beachheads in the main public clouds.

Blocks & Files sees echoes here of Infinidat extending its offering to take on board SaaS-based array management. This concept was pioneered by Nimble and is seen in elements of Pure’s Evergreen service and NetApp’s Data Fabric.

Availability

InfiniVerse will be available this quarter at no charge to supported customers.

InfiniBox Software v5 delivery starts in the third quarter, 2019. The 16/32Gbits FC and 25GbitE options for InfiniBox arrays are available this quarter. New InfiniBox systems shipping in the quarter will be NVMe-oF and SCM-ready. Certain elements of the Elastic Data Fabric are here now and others will be delivered in mid-2020.

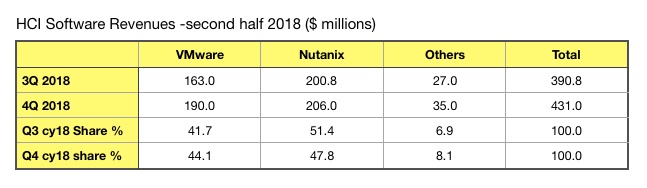

Nutanix leads the hyperconverged infrastructure software market, according to Gartner research seen by Blocks & Files.

This contrasts with IDC numbers, released last month, which showed VMware and its VSAN product, topping the HCI software market, with Nutanix in second place.

However, a Gartner report by analyst Naveen Mishra, titled ‘Market Share Analysis: Data Center Hardware Integrated Systems, Worldwide, 3Q18 and 4Q18 – 19-Apr-2019‘ shows Nutanix in pole position. HCI software market. The report is listed in Mishra’s recent Gartner output.

Clicking on the bottom report gets a “File Not Found We apologize for the inconvenience The page you were trying to reach cannot be found on gartner.com” response.

The report was not available on Gartner’s media site when Blocks & Files looked but kind customer sources supplied some basic numbers.

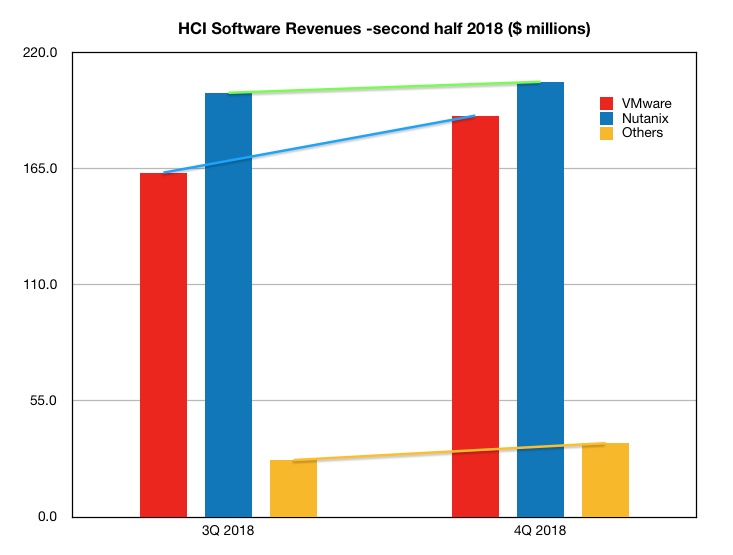

We’ve tabulated these figures.

Nutanix leads in Q3 and Q4 2018 although its lead over VMware fell in Q4 . The two companies collectively accounted for 91.9 per cent of the HCI software market in the fourth 2018 quarter, with ‘others’ such as NetApp, Pivot3, Scale Computing mopping up the rest.

The lines in the chart above show VMware had a great catch-up quarter with Nutanix – and also that the “others” are not in imminent danger of any market break-outs.

Also maybe noteworthy is that the Gartner 4Q 2018 figures cover two months of Nutanix’s anaemic Q2 FY2019 earnings. Nutanix blamed a lack of attention to lead generation for lower than anticipated revenues in the quarter. Was it just a blip? It will be fascinating to see how things change over the next couple of quarters.

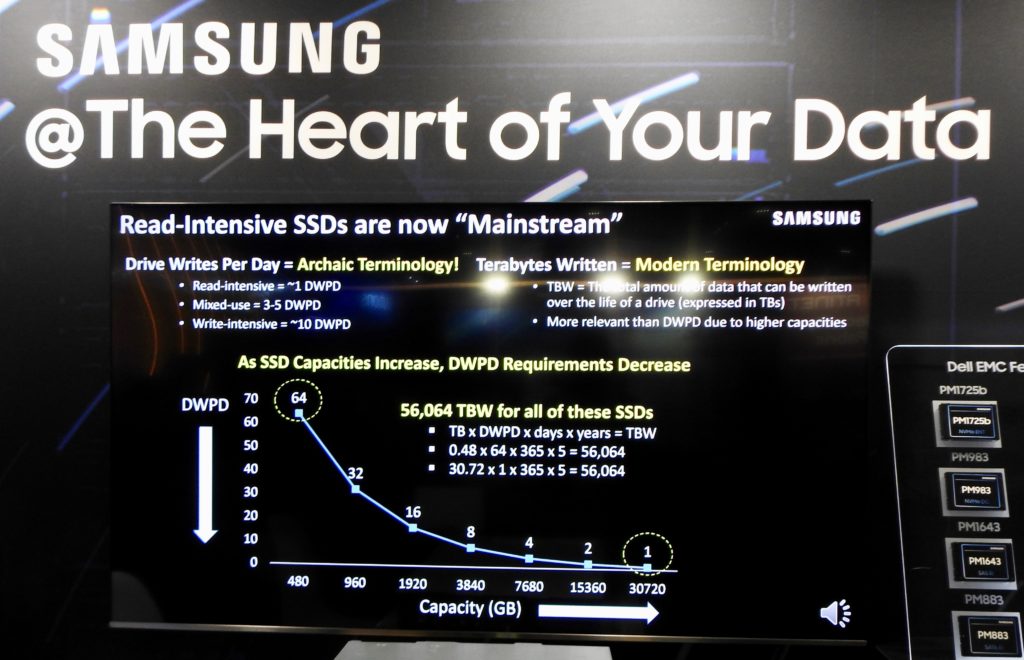

Samsung thinks drive writes per day (DWPD) is no longer fit for purpose as a useful measure of SSD endurance – in other words how long the SSD lasts before wearing out.

DWPD is widely accepted as an endurance measure but as SSD capacities increase, DWPD requirements decrease, Samsung said.

The company recommends terabytes written (TBW) as a more appropriate way to measure endurance and illustrated its ideas this week at Dell Technologies World in Las Vegas.

Check out the slide below.

TBW is calculated by using a formula: TBW = TB capacity x DWPD x days x years. Samsung uses the example of a 480GB SSD with a 64 DWPD rating and a 56,064 TBW rating:

0.48 x 64 x 365 x 5 = 56,064 TBW

The company cites a 30.72TB SSD rated at 1 DWPD, which has the same TBW rating:

30.72 x 1 x 365 x 5 = 56,064 TBW

Over-provisioning

Blocks & Files thinks something different is going on. SSD manufacturers over-provision SSDs above their nominal capacity because the flash cells wear out as data is written and rewritten to them. The manufacturer adds spare replacement cells to the drive in order to retain full capacity over the drive’s warranted life time. This ensures the quoted capacity is not reduced over time due to cell wear-out.

Endurance is measured in how many full drive writes a day an SSD can handle before wearing out.

For the sake of this argument, let’s say that 20 per cent over-provisioning is required to achieve a rating of 64 DWPD. With the 480GB drive in Samsung’s example an extra 96GB of flash is needed.

To achieve the same 64DWPD rating for a 30.72TB drive, the manufacturer needs to over-provision by 6.24TB – 65 times more than with the 480GB drive. That 6.24TB takes up physical space and costs money to produce.

So, by saying the 30.72TB drive has a 56,064TBW rating the endurance sounds good, whereas saying the drive has a 1DWPD rating sounds bad.

DWPD and TBW represent the same thing in different ways. Blocks & Files thinks DWPD is what we are used to and gives an instantly more insightful measure of a drive’s endurance. Stick with it.

Dell EMC is unifying its mid-range storage product around a single new platform, potentially called PowerStorage, based on XtremIO, with the internal codename Trident.

Dell EMC has revealed a little about its thinking on Midrange.next – through some Linkedin profiles and a job ad for the company’s Trident subsidiary.

1. Mark Weare’s LinkedIn profile says he is: “Sr Consultant Services Product Lead for XtremIO & Next Gen Mid-Range Products [and] Providing leadership to teams responsible for service planning, readiness and serviceability product management for Dell EMC’s Storage Division (XtremIO and Trident product lines).“

Trident develops a new class of storage solution based on groundbreaking innovation in primary storage design. Leveraging Solid State Drive (SSD) technology, we re-architect storage to deliver unprecedented value in performance, economics, operations, and data management efficiencies, addressing major pain points in high growth Enterprise IT markets.

“Trident is a Dell EMC company, led by a team of experienced professionals and entrepreneurs with a highly successful industry track record. The company’s R&D is headquartered in Herzlia, Israel, and Hopkinton MA.

We are looking for candidates capable of leading and specifying system design and specifications to address the system’s complex management, control and data aspects, coping with a distributed scalable highly available storage system.

Our understanding is that the contributing storage arrays, XtremIO, Unity, and SC, will co-exist with the new mid-range system, possibly for many years. There will be no speedy end-of-life moves.

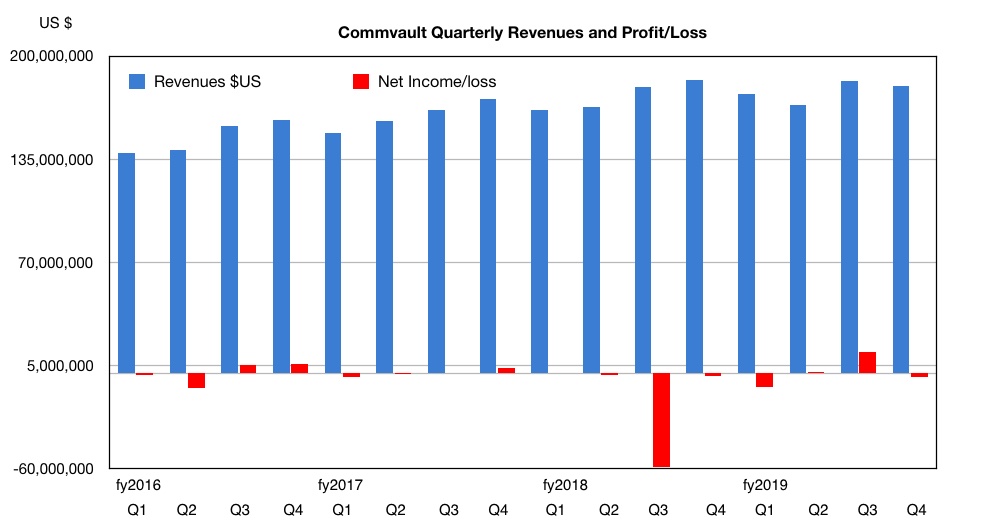

Revenues in Commvault’s latest quarter dipped slightly, just enough to remind incoming CEO Sanjay Mirchandani, that he has a job on his hands after three months in the post.

Revenues of $181.4m in the fourth fiscal 2019 quarter fell two per cent year-on-year ($184.9m). There was a loss of $2.2m (-$1.7m).

The earnings call revealed two reasons for the revenue dip, according to CFO Brian Carolan, who cited “lower than expected revenues from large enterprise transactions and poor execution with the channel, particularly in the mid market.”

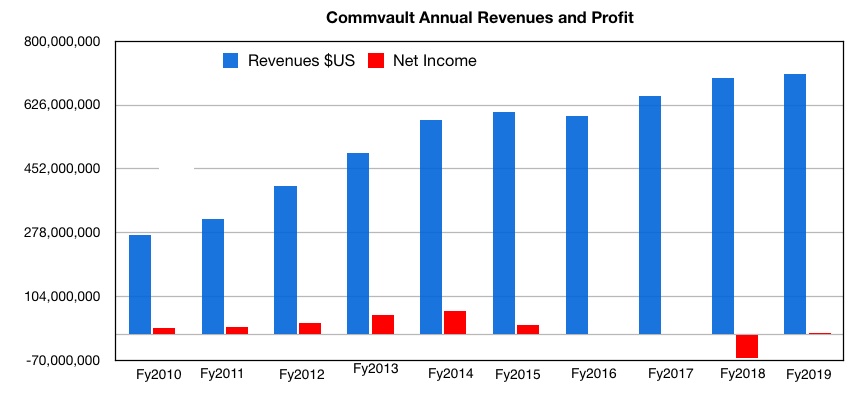

Full fy2019 revenues were up two per cent to $710.9m ($699.4m) and net income improved to $3.6m (-$61.9m).

Commvault quarterly revenues and profits/losses.

Commvault annual revenues and net income

Mirchandani said Commvault is making good progress with “significant increases in annual contract value, repeatable revenue and earnings per share.”

In the earnings announcement, he said the company had “implemented extensive operational and organisational changes over the past twelve months, which have enabled us to reduce costs, increase repeatable revenues, and deliver significant year-over-year earnings growth. However, we have more work to do to ensure that Commvault reaches its full potential.”

The company is “focused on simplifying our business and improving execution. Actions are underway in each of these areas, and our employees are energised about where Commvault is heading.”

All change at Commvault

With regard to simplifying operations, Mirchandani said: “In the last few weeks, we’ve made several changes to further improve our performance and ensure we have the right people in place to deliver on our strategy. We work to ensure the leadership team and I are much closer to our customers by realigning our field and partner teams globally, flattening our organisation by eliminating the Chief Operating Officer role and recalibrating our partner organisation.”

He said: “I asked a Commvault veteran, Gary Merrill, to lead our global operations and simplification initiatives as Vice President of Business Operations, a new executive position and priority for fiscal year 2020…As a result of our changes, our field teams can now focus on our strategic initiatives like landing new customers and selling subscriptions.”

He mentioned “improving our run rates through better channel engagement, enablement and my putting resources closer to the field. This includes increasing our large deal predictability by strengthening our funnel to better demand generation capabilities and more aggressive digital marketing.”

There’s more: “To drive our strategy and dramatically improve our go-to-market processes, I brought in Tom Broderick, our VP of Strategy and Business Readiness. He is responsible for ensuring that’d we have a clear end to end path to effectively and efficiently bring our products to market and drive satisfaction throughout our ecosystem.”

The channel partner angle is receiving attention too: “We elevated our strategic alliances, cloud and managed services teams higher in the organisation and aligned our field partner leads closely with our field sales leadership, so they’re in lockstep with their regions.”

Finally: “I’m finalising new elements of our strategy that I believe will land new customers, broaden the reach of our partners and clearly deliver more value. I look forward to sharing these finalise initiatives in the coming months.”

Channel flannel

William Blair analyst Jason Ader said: “VAR checks indicate that Commvault has lost substantial competitive ground to Veeam, Rubrik, and Cohesity.”

Ader is cautious but positive in his outlook for Commvault: “While some investors might argue that these proposed changes are too little too late, especially as execution has almost become a perennial challenge at Commvault, we are giving the new CEO the benefit of the doubt here, especially given our belief that the underlying drivers of Commvault’s business remain intact.

“Specifically, multi-cloud adoption is driving enterprises to reevaluate and ultimately modernise their data protection capabilities, enabling substantial opportunities for Commvault and its peers.”

We note that Ron Miller, SVP worldwide sales, resigned last month. Carolan said the company aims to hire a chief revenue officer by the end of the current quarter.

Dell Technologies World Dell EMC has announced Cloud Storage Services, a disaster recovery option that removes the need for a separate storage DR site and so cuts costs. The service uses the public cloud and an MSP intermediary instead.

The service is a two-stage affair where customers replicate data to an MSP (managed service provider) facility, which has a Direct Connect link to a public cloud.

When disaster strikes at the on-premises site the compute switches to the public cloud and the stored compute instances access data on the arrays using a Direct Connect link. Claimed speed is 3msec or faster.

Cloud Storage Services supports PowerMax, Unity and Isilon on-premises arrays. The SC arrays are not supported.

Arrays without a Direct Connect link could take up to a second or more to replicate data to the public cloud, depending on network bandwidth.

Dell envisages customers will typically replicate a subset of data to the MSP site, so the arrays there would be smaller than their on-premises relatives.

This is similar to NetApp’s 2012 vintage NetApp Private Storage which “allows one to place a NetApp FAS appliance in a data centre – specifically one where Amazon’s Direct Connect is operating – from where it will be available for “immediate use via iSCSI to and from their EC2 environment.”

Cloud Storage Services supports four public cloud targets: VMware Cloud on AWS, AWS, Azure and GCP. Dell EMC said the multi-cloud approach enables compute instances in each cloud to access the MSP arrays. There is no need to move data to these clouds or to pay for storage. Users pay only for the compute in the cloud when it has to be used.

Customers running VMware environments can implement a DR system using VMware Cloud on AWS as the secondary site. VMware Site Recovery Manager, along with native replication of the Dell EMC storage arrays, enables automation of DR operations.