Nutanix latest results show it adding new customers and growing subscription revenues in the face of the Covid19 pandemic.

Sister publication The Register covered Nutanix’ third quarter fiscal 2020 earnings this moring but we have taken a look at some of the details to give you a B&F’s perspective, and they show a business that is weathering the storm.

William Blair financial analyst Jason Ader told his subscribers: “In the midst of a global pandemic, the company delivered strong billings and revenue growth, achieved record pipeline growth, and significantly reduced its operating expense run-rate. While balance sheet concerns may have not disappeared, they have certainly been alleviated as Nutanix management focuses on sales productivity and cash efficiency in this new world order, and as the company gets one step closer to reaping much of what it has sown on its subscription model transition.”

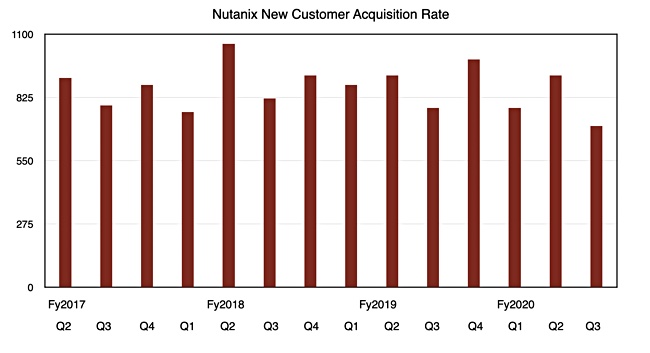

Looking at the detail, customer acquisition numbers grew by 700 in the quarter, which ran from February 1 to April 30, and now total 16,580. This is a slowdown from Q2 when 920 new customers were added and from Q1 which saw 780 new customers logged. Nutanix has a target of passing the 23,600 customer mark by fiscal 2021.

Charting 14 quarters of customer acquisition numbers shows that Q3’s 700 was the lowest total for all these quarters.

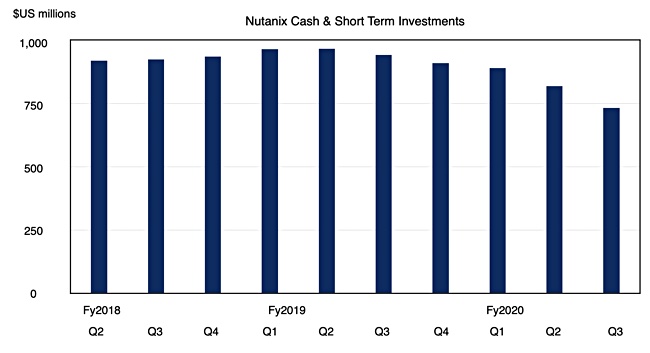

Cash and short term investments have also taken a hit, amounting to $732.1mn at the end of Q3, down from $940.8m a year ago. There has been a steady quarterly drop since the high point of $965.9m in Q2 fiscal ’19 as Nutanix’ growth cost it money. That’s also shown by the quarterly losses Nutanix is making;

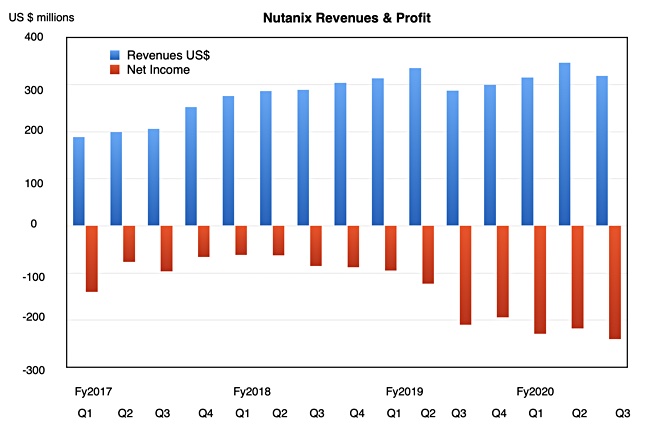

Revenues grew 11 per cent year-on-year in Q3 ($287.6m to $318.3m), despite the pandemic.

Nutanix growth strategy has been based on two major pillars: To broaden the product portfolio beyond core hyperconverged infrastructure appliances; and to adopt cloud-style subscription billing.

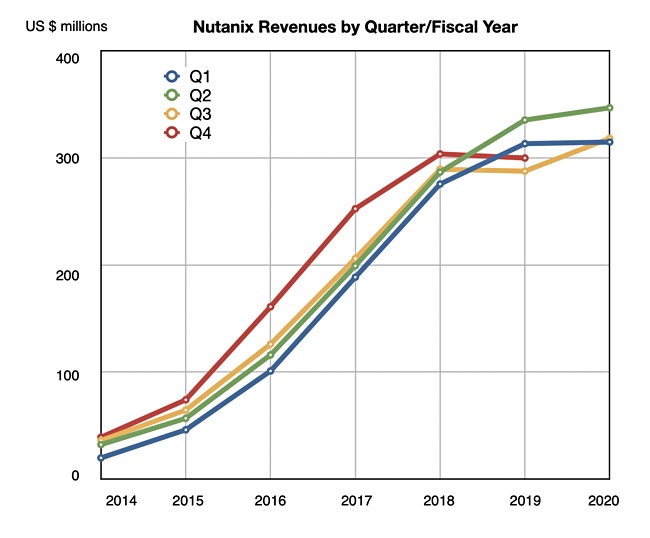

It been converting business from perpetual license sales to subscriptions for several quarters and has been affected, to a small degree, by the loss of up-front license revenue. Our fourth and final chart looks at Nutanix’s quarterly revenues by fiscal year and shows a revenue growth reverse in Q3 and Q4 of fiscal ’19 and again in Q1 of fiscal 2020, but since then growth has resumed.

Nutanix has been showing revenue growth resilience in the face of the pandemic with increases in customer spend as well as having more customers. Wells Fargo senior analyst Aaron Rakers told subscribers: “Nutanix continues to highlight strong large customer traction; 910 Global 2K customers w/ cumulative spend growing 37 per cent y/y and accounts for ~30 per cent of revenue.”

Rakers noted that “32 per cent of Nutanix’s F3Q20 deals include at least one product beyond core; company notably highlighting End User Compute/Desktop-as-a-Service strength given work-from-home demand.”

That’s a net positive benefit from the pandemic.

He also said subscription renewals are becoming more and more important to Nutanix which “reported that the renewal base of business stood at $5m in F3Q20; expected to expand to $10m. While we are in the early innings of Nutanix becoming a subscription renewal story, we think Nutanix’s commentary and incremental disclosures will begin to drive this as an increasing narrative / future positive driver of top-line revenue and, more importantly, operating leverage.”

Ader explained this reasoning: “[Nutanix] management noted that more than 90 per cent of quarterly bookings today are composed of new and up-sell business, which dampens visibility and carries high sales and marketing costs.

“Once the company begins to see a meaningful renewal pool (expected to be only $10 million in the fourth quarter) and aligns sales incentives properly, it should not only achieve better visibility but also see significant operating leverage (as renewal deals are transacted at much lower cost than new or up-sell deals). This to us is the essence of the bull case on Nutanix going forward.”

He added: “Our field checks point to hyperconverged infrastructure emerging as a clear winner in the post-COVID-19 world as customers rethink their long-term infrastructure architectures with a focus on cloud-like simplicity, automated operations, easy setup, built-in burstability, and disaster recovery. Last but not least, we view Nutanix as a highly strategic asset with the potential for takeout interest from larger players that desire a best-of-breed private cloud/HCI platform.”

Comment

What is the big story here, the main thrust?

There are just two dominant hyperconverged infrastructure appliance vendors in the market; Dell Technologies and Nutanix. Nutanix’ growth is simply not being stopped by Dell Technologies’ VSAN and VxRail products. This billion dollar run rate SW-defined server application platform hybrid cloud company is set for the long-term.